Bad Week for Energy Stocks? Wait Till Next Year

(Bloomberg Opinion) -- One word to describe this week in energy stocks is “painful.” Another is prologue.

Energy stocks were not particularly popular coming into this week anyway. To one degree or another, they were losing the confidence of investors that they will manage their capital responsibly and profitably.

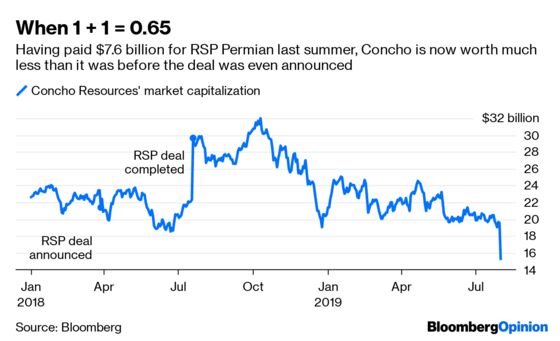

Now their deserved reputation for squeezing ever more oil and gas out of shale has also taken a big knock. Concho Resources Inc. plunged 22% on Thursday, to its lowest level since the panic of early 2016, after it cut guidance and revealed weak results from an experimental project of drilling wells much closer together than usual. Other Permian producers, such as Diamondback Energy Inc., also took a hit on fears this reflects a shale-productivity issue, rather than just a Concho issue. It’s sobering to think that Concho, valued at more than $23 billion in the spring of 2018 and having since absorbed the $7.6 billion purchase of RSP Permian Inc., now sports a market cap of less than $16 billion.

Meanwhile, the industry also has a problem with a man who is nominally its champion: President Donald Trump. His offhand tweet-threat of more tariffs on Chinese goods on Thursday afternoon took what was already a flaming dumpster fire, hitched it to a truck and took it straight over a precipice (the Federal Reserve’s quarter-point rate cut fading quickly in the rear-view).

Trust, trip-ups, Trump. They seem like separate problems for the sector, but they actually add up to the same problem: cost of capital.

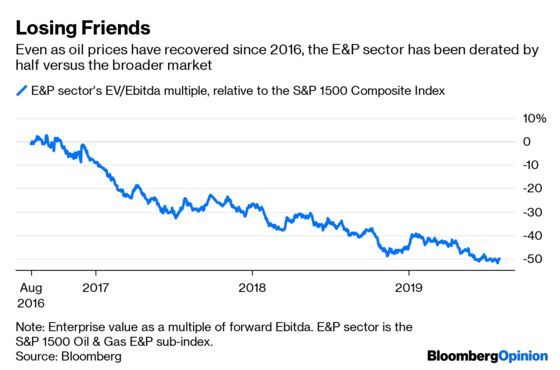

Equity and bond issuance has faltered across the energy sector. Services giant Schlumberger Ltd., which has talked consistently of a recovery for several years, just changed its CEO, and its stock languishes around levels plumbed during the financial crisis. The pipeline sector, meanwhile, is undergoing a painful transformation away from the once-dominant (and so hot) master limited partnership structure. Missed expectations there are punished swiftly, while good behavior is rewarded with a stable, rather than surging, stock price.

Concho’s problems with its “Dominator” project affected only a small minority of the wells it has drilled so far this year. But investor tolerance for wasted capital – as well as sharp revisions to guidance given only a few months ago – has evaporated. When Pioneer Natural Resources Co. surprised in mid-2017 with a snafu of its own, its stock was trading at parity with the market and a one-third premium to the sector in terms of Ebitda multiple. It never recovered that poise. Today, it trades below both.

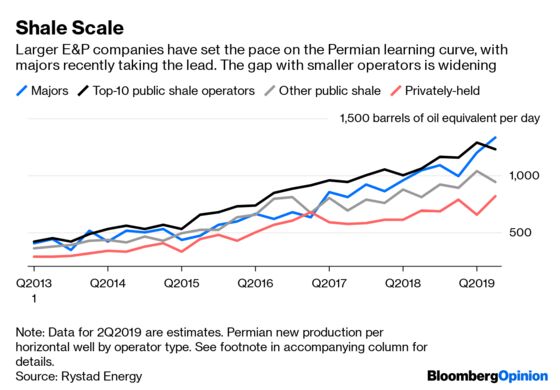

Many companies in an industry predicated on growth are struggling to make the pivot to prioritizing return on capital and shareholder payouts. It has traditionally been a sector that took in capital rather than spat it out. This is a particular problem for smaller and mid-cap companies, which tend to carry higher unit costs and struggle to attract attention and investors (though not, of late, activists). And a new report from Rystad Energy, a research and analytics firm, suggests smaller is worse when it comes to productivity too :

The basic equation here – rising cost of capital and flat-but-volatile oil prices – demands radical change. There’s really no reason why dozens and dozens of companies should be cheek-by-jowl in the Permian basin, other than a steady flow of external capital that has dried up.

If, as seems likely, 2020 hosts a confluence of weaker economic growth – with added Twitter trade-war frisson – and high non-OPEC production growth, this week’s wash-out will have been a mere prologue to what’s coming. The cure is consolidation, which would cut costs and rein in the barrels pushing into an already oversupplied market. However, it appears we still aren’t quite there yet.

One obvious potential acquirer, ConocoPhillips, was asked on this week’s earnings call whether falling E&P valuations had piqued its interest. In response, the COO said:

We still believe that there is a mismatch between what people expect for their assets and what we compete as a use of capital for our capital, and that may change over time.

Translation: Stuff isn’t cheap enough yet.

One obstacle to deals is, paradoxically, something that also lies behind the sector’s chronic de-rating: misaligned incentives for management vis-a-vis shareholders. In a new report, Evercore ISI analyst Doug Terreson calculates that, for a sample of nine large E&P companies, the average value of the pool of stock and option awards held by their CEOs at the end of 2016 was $26 million. By the end of 2018, that had risen by $21 million – of which just $1 million reflected higher share prices; the rest was new awards. The total return of the E&P sector in that time was negative 35%.

As long as the corner office enjoys a more positive outcome than shareholders do, it suppresses any willingness to negotiate a deal that could change the occupant of that corner office. As this week demonstrates, though, pressure for change is building inexorably. The cost of capital is getting just too damn high.

In the accompanying chart, 'Majors' refers to BP, Chevron, Exxon Mobil, Occidental Petroleum and Royal Dutch Shell. The 'Top-10' public companies are Anadarko Petroleum, Apache, Cimarex Energy, Concho Resources, Devon Energy, Diamondback Energy, Encana, EOG Resources, Parsley Energy, and Pioneer Natural Resources. These are the top 10 operators bynumber of horizontal unconventional well-completions in the Permian shale basin, according to Rystad Energy's figures.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.