Axis of Evil, Axis of Joy. Emerging Asia Splits Apart

The fast and furious stock rallies in Indonesia and Philippines are good reminders of what emerging-markets investing is all about

(Bloomberg Opinion) -- They were down but never out. The fast and furious stock rallies in Indonesia and the Philippines are a good reminder of what emerging-markets investing is all about.

As the U.S.’s record bull run falters, developing nations are finally becoming a haven. We’ve been making the argument for the asset class since late September.

But not all developing markets are created equal; in fact, there’s a wide divide. Over the past month, the Philippines and Indonesia were by far the world’s best performers. Meanwhile, Taiwan and South Korea are struggling to break out, and mainland China continues to choke in its bear pit. Mean reversion, one of the key reasons behind Morgan Stanley’s bullish call on emerging markets for 2019, hasn’t quite worked out yet.

What’s driving this north-south Asian divide?

Two broad factors shape emerging-markets investing. Strong global economic growth tends to lift export-oriented North Asia, while the Federal Reserve’s interest-rate policy moves younger markets such as Indonesia and India. Countries such as China and Korea, which have current account surpluses thanks to their exports, are less vulnerable to international portfolio flows. Meanwhile, South Asia is all about domestic demand.

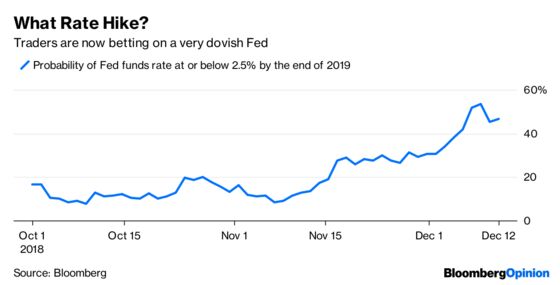

This year has been especially bruising for emerging markets because both factors were at play. In October, the International Monetary Fund lowered its global growth outlook set only six months earlier, citing trade tensions. Meanwhile, the Fed is poised to raise rates for a fourth time this year, the most in more than a decade. Increasing U.S. borrowing costs have sent countries such as Indonesia, where foreigners own close to 40 percent of government bonds, scrambling to raise rates.

But traders have been recalibrating lately, paring back expectations for further tightening next year. The odds on the Fed hiking only once more by the end of 2019 are now close to 50 percent, a prospect that appeared improbable just two months ago.

Viewing emerging markets along these two axes, it’s not surprising that Southeast Asian markets are beating their northern neighbors.

This is a good time to reflect on why global investors want to put their money in this asset class. Many are attracted to the demographics — young, eager consumers using smartphones or opening bank accounts for the first time. But in reality, only some nations fit the bill. China’s demographics, for instance, don’t look any better than those of the U.S.

Earlier this year, foreigners shunned the Philippines, fretting over soaring inflation and the threat of central bank tightening. Now, with growth slowing and oil prices down, the world has a deflation problem. In that light, is inflation in the Philippines such a bad thing?

Indonesia’s biggest problem is its reliance on foreign money. But the central bank has been a mature kid on the emerging block, preemptively raising rates to buffer against the risk of another taper tantrum. The rupiah is now offering a juicy real yield of 2.8 percent, among the highest in emerging markets.

Voices are growing louder that emerging markets are the place to be in 2019. As investors place their positions though, it’s good to remember that this asset class includes a wide cross-section of nations, each responding to different factors. May the right forces be with you.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2018 Bloomberg L.P.