Emerging-Market Malaise Won’t Be Going Away Anytime Soon

(Bloomberg Opinion) -- By my count, emerging-market currencies are in the midst of their fifth major weakening trend since 2011. The origins of the current downturn are broadly similar to the earlier four episodes, which is to say that a combination of rising U.S. Treasury yields, sluggish equity markets and risk aversion are to blame. What’s different now is that these factors may not dissipate as quickly.

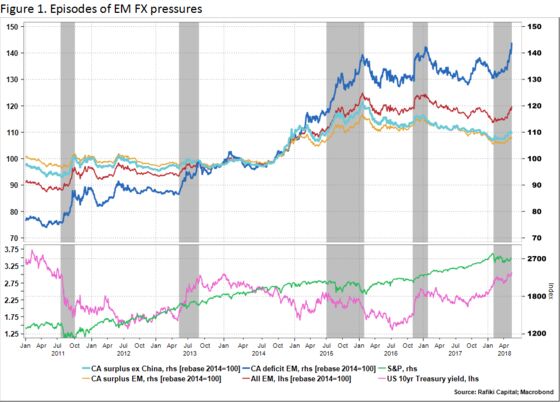

The sensitivity of emerging-market currencies to higher rates is striking. Every major upward move in yields since 2011 has triggered currency weakness among countries with large current-account deficits. So unless there’s a recession or a serious slump that would reverse the rise in U.S. yields, the pressure is likely to continue. In the chart below, the shaded areas represent recent episodes of emerging-market currency weakness. The red line is an index of overall emerging-market currency valuations and the dark blue line is emerging-market currencies with current-account deficits. The light blue line denotes currencies of current-account surplus countries excluding China.

The 2011 and 2015 episodes were largely confidence events, as they came first with the U.S. government shutdown and then with China’s surprise decision to devalue the renminbi. Both were accompanied by weakness in equities (green line). The drop in bond yields (purple line) reflected pessimism. The 2013 and 2016 episodes were driven purely by higher bond yields. It didn’t matter what equities were doing. The current episode is one of sharply rising yields and, at best, a sideways equity market.

What are the takeaways?

- The 2000s-era of EM market leadership are gone, even if the sequence of profound 1990s emerging-market currency crises is not quite back. It is not just the frequency of these episodes, but the drivers. The two big EM currency sell-offs of the 2000s were driven by global downturns, and emerging markets led the charge back once recovery began. The emerging-market downturns of the last couple of years were driven by the normal ups and downs and random shocks. These come more frequently than global downturns, and the recoveries among current-account deficit EM currencies are shallow.

- There are two sets of emerging-market currencies. The high current-account deficit countries lose ground when there’s stress and rarely recover when stability is restored. They fall versus the euro as well as the dollar. On a carry-adjusted basis, these currencies have weakened since 2011. Currencies of current-account surplus countries have typically declined modestly against the dollar, and often recover those losses when conditions stabilize. The currencies are very stable over time versus the euro. When we talk of crisis, we are dealing with an important but limited set of countries.

- It’s hard to find an emerging-market reform story. There were rays of optimism a few years ago, with incoming governments in Argentina, Peru, Brazil, Mexico and India somewhat committed to economic reform. There were hopes that the Arab Spring would prompt economic as well as political reform. Those efforts have faltered. If anything, the attraction of authoritarian governments is growing and the impetus to political and economic reform is faltering. My respect for age and experience increases every year, but it’s hard to see the new Malaysian government as growth- and reform-focused.

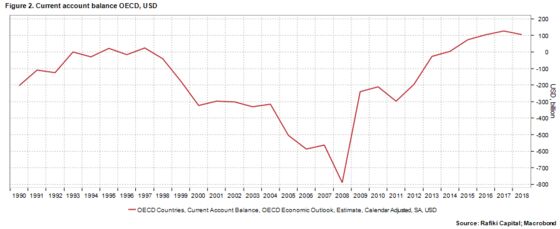

- G-10 macro conditions are not supportive. From the late 1990s on, OECD countries collectively ran large and increasing current-account deficits (see the chart below). The flip side was improving current-account surpluses in emerging markets. This has reversed since 2008, with OECD countries now running surpluses. It’s unlikely that the pace of OECD expansion will be so strong in coming years to restore emerging-market economies to a significant collective surplus.

- Structural factors are working against emerging markets. The most positive scenario for EM is if developed economies grow fast and the growth is intensive in low- and middle-tech goods and commodities. However, both production and sales are shifting to service-oriented industries. For emerging-market countries, it is much better if marginal demand is for shoes, shirts and televisions, but marginal demand in developed economies looks to be shifting to services such as leisure, health and education.

I started this column far more optimistic than when I finished. There’s a scenario in which tax reform and other structural factors drive strong, low-inflation U.S. economic growth, China opens its economy to a greater degree, and the euro-zone economy keeps expanding. But that’s nothing more than hope. There’s another scenario in which emerging-market economic and political reform generates endogenous growth, but this may be even more hopeful. Absent good luck, and especially in an environment of rising bond yields, pressures could end up being chronic.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

©2018 Bloomberg L.P.