Hot Emerging Markets May Be in for a Shock

The global economic slowdown flagged by lower interest rates and bond yields will ultimately be a net negative.

(Bloomberg Opinion) -- The U.S. Federal Reserve’s pivot to easier monetary policy has had a positive impact on emerging markets. Both the MSCI EM Index of equities and the Bloomberg Barclays Emerging Markets Local Currency Government Debt Index are poised for their best quarters since the start of 2017. Also, several key currencies have risen against the dollar.

Recent bond market developments in the U.S. and Europe, however, suggest that policy easing is no longer an unalloyed positive. Negative-yielding debt globally has just risen to $10 trillion, suggesting economic weakness. Lower interest rates in developed countries are likely to have different impacts on emerging markets in the short run relative to the fallout that may come in 2020 and 2021.

While lower rates for borrowers in hard currencies would reduce debt service expenses and alleviate pressure on their balance of payments, the economic slowdown that lower rates and yields portend would ultimately be negative. Emerging markets feasting on cheaper credit in the short-term may be in for a rude shock as importing nations cut purchases in response to their economic weakness.

To perform well over the short- and medium-term, investors should divide emerging-market investments into two components. The first would consist of countries such as Turkey dependent principally on speculative capital inflows that policy easing in the U.S. and Europe may benefit. This would be the “high-risk” portion of the portfolio.

The second component would include countries such as Brazil dependent on direct investment flows to finance the bulk of their development needs. Foreign direct investment flows tend to be “sticky” and provide more stability to the economies of recipient countries, reducing downside risk to foreign portfolio investors. This component would be a “low-risk” manner of investing.

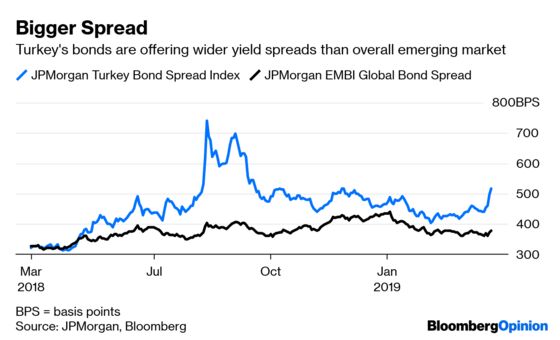

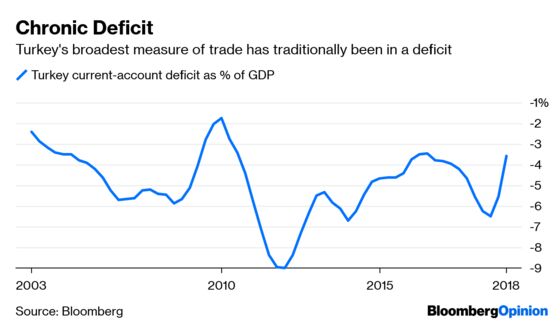

Turkey has historically run large current-account deficits that have increased over time. The shortfalls have been financed largely by short-term capital inflows that could easily reverse direction and leave the country. That is what happened Friday when the lira fell by 5.8 percent after news that official international reserves had fallen following authorities’ failed attempt to support the currency.

Turkey’s prospects of attracting capital during coming months, however, should improve as foreign investors reach for higher yields. Turkish bonds yield about 5 percentage points more than U.S. Treasuries, significantly more than the 3.73 percentage-point spread of the JPMorgan Global Emerging Market debt index.

Looking beyond the immediate future, Turkey’s external accounts suffer from a serious problem. Imports of goods and services significantly exceed exports, and foreign direct investment flows constitute a smaller and smaller portion of the funding. For investors, this structural weakness means that the lira will experience bouts of volatility as capital flows change direction. It also implies that government policies are not conducive to attract long-term investors.

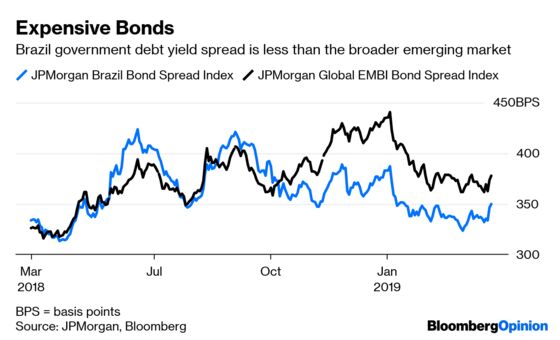

At the other end of the emerging-market risk spectrum, Brazilian sovereign debt yields only 3.46 percentage points more than Treasuries, seeming to diminish its attractiveness to yield seekers in a dovish central bank environment.

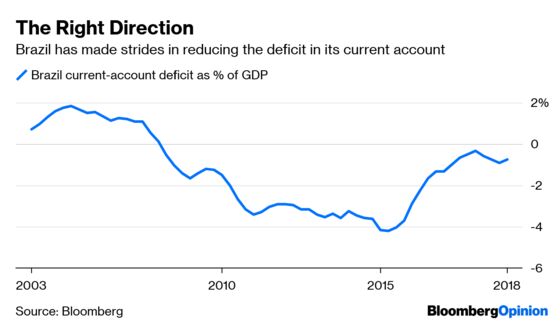

On the other hand, Brazil’s fundamentals are on a sounder footing. Its external balance has steadily improved since 2015, and it has almost eliminated the deficit. Foreign direct investment flows have been more than enough to finance the deficit, contributing to an increase in international reserves held by the central bank. That should provide greater currency stability and reassure investors.

The widely held view that lower global interest rates are positive for emerging markets applies only in the short term. Beyond that, the impact of easier monetary conditions will be offset by a slower global economy. Countries making themselves attractive to long-term investors are likely to offer higher, as well as more stable, returns.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Komal Sri-Kumar is the president and founder of Sri-Kumar Global Strategies, and the former chief global strategist of Trust Company of the West.

©2019 Bloomberg L.P.