(Bloomberg Opinion) -- Selling Tesla Inc.’s stock short is the Escher’s “Waterfall” of trading. On the heels of an Axios interview of CEO Elon Musk broadcast this weekend, here is a brief summary of some things that happened over the past year or so:

- Short sellers claimed Tesla was heading for bankruptcy and/or needed to raise a lot of capital, and placed bets accordingly;

- Tesla said it did not need to raise capital;

- Musk just did the aforementioned Axios interview and admitted Tesla was “bleeding money like crazy” and within “single-digit weeks” of death at some point in the past year or so;

- Despite thereby validating short-sellers’ earlier suspicions, the stock was up in early trading on Monday.

I mean, are you not entertained?

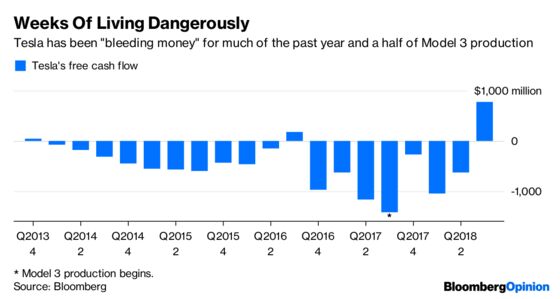

Recall, back on April Fool’s Day, Musk tweeted a series of jokes about the supposed risk of Tesla going “bankwupt.” Was this during the actual “single-digit weeks” period in question? Tesla demurred when I asked about timing, but it is quite possible. Tesla burned through almost $1.7 billion in the first half of 2018. Just a couple of days after Musk’s tweets, the company disclosed it had missed its reduced first-quarter production target for the Model 3 car — the accelerant for all that cash.

In that same release, however, Tesla went out of its way to say it “does not require an equity or debt raise this year, apart from standard credit lines.” So, surely that can’t have been the period in question, because how could Tesla proclaim financial robustness even as the edge of the waterfall hoved into view? If not then, though, when was it? Tesla has had boilerplate risk-factor stuff in quarterly and annual filings about having enough cash to service debt and has also admitted problems with the Model 3’s production schedule. But I don’t recall any public disclosure of potentially imminent demise in the past year or so.

You might think the CEO would shy away from making public statements seemingly at odds with earlier public statements. Especially when he just had to settle a lawsuit with the SEC due to problematic public statements about a potential takeover that suffered from an unfortunately tenuous attachment to reality. Even more so when said settlement forced him to give up his position as chairman and submit future public statements to vetting.

The interview comes soon after surprisingly positive third-quarter results, albeit with lingering questions about how sustainable they are. Perversely, in revealing Tesla’s apparent near-death experience, Musk’s interview not only offers some vindication to short-sellers but also provides a narrative for bulls that the worst is truly behind the company. The latter also chimes with the perception held by committed fans of Tesla being an underdog able to engineer its way out of even the most dire circumstances like a $59 billion MacGyver.

In that sense, Musk co-opts one of the very arguments put forth by those betting against him — even as he revives chronic concerns about liquidity and governance. Fascinating stuff. Still, like so much else with Tesla and its CEO this year, I find myself asking: Why do this?

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.