A Digital Currency to Fight Data Overlords

The ECB’s privacy-first approach to digital cash may offer a global template for authorities to negotiate with Big Tech.

(Bloomberg Opinion) -- From e-commerce firms and payment processors to governments, everyone with half a server and an algorithm wants our data. So it’s a pleasant surprise to see at least one central bank expressly rejecting the idea of sweeping up personal information in designing its electronic cash.

The European Central Bank “has no interest in monetizing or even collecting users’ payment data,” executive board member Fabio Panetta told the European Parliament last week. A digital euro would let people “make payments without sharing their data with third parties, other than what is required by regulation.”

This restraint is refreshing in what’s developing into another area of superpower contention. Digital currencies are in the news less for what they’ll mean to users and more for how they would help issuers. Whether China could use a fully online version of taxpayer-backed cash to challenge the dollar’s hegemony gets the most attention. The electronic yuan, e-CNY, will be available for international visitors during next year’s Beijing Winter Olympics, People’s Bank of China Deputy Governor Li Bo said at the Boao Forum on Sunday. We may know more about preparations for a FedCoin as early as July, when the Federal Reserve Bank of Boston and the Massachusetts Institute of Technology, which have been developing prototypes for a digital dollar, unveil their research.

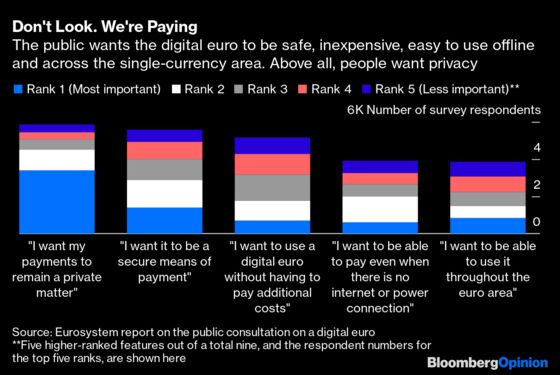

The eurozone is still some years away from deciding whether to offer an electronic version of physical cash. If it does go ahead, the overriding goal may be less about joining the U.S.-China race and more about taking back some of the data-mining power of private payment apps — and handing it back to citizens. That’s what people also want: 43% of the record 8,000-plus replies the ECB received in its recently concluded public consultation on the digital euro identified privacy as the most important feature.

In societies where the state has already appointed itself Big Brother in exchange for supplying trust in economic transactions (and in human interactions, after Covid-19), individuals can do very little to reclaim ownership of their data. Beijing may not want to surrender the surveillance capabilities of the digital yuan, whatever its unease with the dominance of private payment services in the domestic economy, such as Ant Group Co.’s Alipay and Tencent Holdings Ltd.’s WeChat Pay.

But Europe, which cares more than most of the world’s major economic powers about personal data protection, will be different.

Beyond checking money-laundering and terror financing, the ECB doesn’t want digital currencies to turn everyday lives into an open book for private payment giants to read and profit from. It’s investigating three different approaches to the privacy challenge.

In theory, it’s possible that electronic cash will be made available as blockchain tokens. In that case, there’s no privacy concern. The user will need to produce the correct cryptographic key to spend the balance in her smartphone wallet. That will make digital currencies similar to physical cash or Bitcoin: Individuals will be responsible for the safety of their money.

But in all likelihood, digital currencies will follow a different path. Starting their life as IOUs in the central bank’s ledger, they’ll resemble deposits more closely than cash. Except that a monetary authority won’t have the bandwidth to verify if all of us are who we say we are, or if we’re double-pending our resources. That job will be outsourced to banks, which will be able to see who’s paying whom — even though we’ll no longer be using their money. Instead, customers will settle claims with the sovereign’s liabilities.

This is where people risk losing the anonymity of cash forever.

One way to counter this could be to separate identities from transactions. Let the operator of the infrastructure see only cryptographic public keys while recording payments, and not the identity of customers. The banking intermediaries used by the payer and the payee will know the link between identities and public keys, but they won’t see the rest.

Another mechanism could be an off-ledger system where the payment details won’t be known to any third party, not even the central bank. This can presumably be done for small-value transactions. Finally, electronic cash could come very close to the real thing if purchasing power could be made to reside on a piece of hardware that their users have to safeguard.

Cash pays zero interest, and that’s the minimum a digital currency will also have to offer to gain popular acceptance. Whether it’s a hit or a flop will depend on third-party value-added services. International payments, for instance, could get a lot cheaper once money moves across borders without requiring elaborate networks of correspondent banks.

It’s important to refocus the discussion on users. All financial and commodity assets are underpinned by a formal system of state-enforced property rights. But not consumer data, which the tech industry has simply captured as if they were “res nullius,” or wild animals, says Columbia Law School Professor Katharina Pistor. One way to force data harvesters to share their supersize profits from analyzing traces of our financial lives could be to give users a bargaining chip — an alternative means of payment that provides instantaneity without commercial exploitation.

The ECB’s privacy-first approach to digital cash may offer a global template for authorities to negotiate with Big Tech on our behalf.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2021 Bloomberg L.P.