Elliott Has a Point When It Comes to EBay

Marketplaces are critical to e-commerce, and the company could do more to compete with Amazon and Walmart.

(Bloomberg Opinion) -- One of the internet’s earliest and most lasting successes, eBay Inc., is under pressure again to remodel itself to fix a persistently cheap share price. The latest initiative from a prominent investor lacks crucial details but also highlights eBay’s missed opportunities.

Elliott Management Corp. disclosed Tuesday that it owns more than 4 percent of eBay’s stock, and it unveiled a blueprint for changes that the firm said could as much as double eBay’s stock price. In a statement, eBay said it would review and evaluate Elliott’s proposals. In addition, the Wall Street Journal reported that another activist known for pushing companies for changes, Starboard Value LP, had also purchased a significant stake in eBay and has a similar fix-it plan.

In many ways, Elliott’s analysis of eBay is a classic activist argument. The firm suggests eBay’s ticket-selling business, StubHub, would be more valuable on its own, as would eBay’s constellation of online classifieds websites in countries such as Germany and Australia.

It’s tough to assess the validity of Elliott’s views on eBay’s asset structure. Suggestions of asset breakups plus cost-cutting and funneling more cash back to shareholders are classics of the activist playbook. And it’s worth remembering that eBay has previously been pushed to separate or sell other assets — notably PayPal. That breakup less than four year ago worked out great for PayPal, which has thrived as a solo company, while eBay’s strengths and weaknesses are largely unchanged from the point of the split.

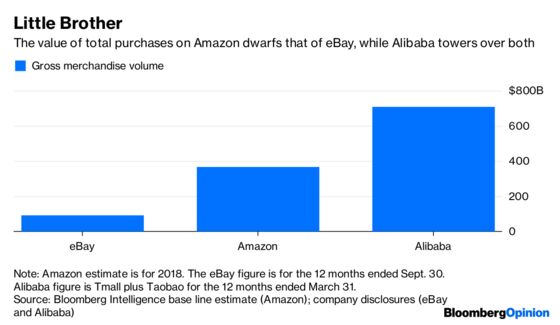

Two points in Elliott’s argument are difficult to refute: Marketplaces are the most promising corner of the e-commerce industry, and investors don’t put much value on eBay’s marketplace business. It has been tough for eBay in Amazon.com Inc.’s shadow, but there are areas for improvement in its marketplace operations.

Marketplace is the industry’s term for middlemen — companies that connect willing buyers and sellers and collect fees for their trouble — and it’s a growing area of focus for some of the world’s dominant online retailers. China’s e-commerce titan Alibaba Group Holding Ltd. is largely a marketplace that allows an army of independent businesses to list, promote and sell products to Chinese shoppers.

Amazon is both a conventional retailer that buys products and resells them and increasingly a marketplace. Just more than half of the individual items sold on Amazon come from independent merchants that sell their goods on the e-commerce site. Their fees tend to be highly profitable for Amazon and are a big reason for the company’s recent increase in profit margins from nearly invisible to tiny. Amazon’s revenue from marketplace merchants amounted to about $40 billion in the 12 months ended Sept. 30 — about one-fifth of Amazon’s total revenue in the period and more than half of Target’s annual sales.

Walmart Inc., too, has drawn digital strength from the marketplace model. In particular, it has allowed the big-box giant to drastically expand its online selection, a powerful change when dueling with a competitor that is known as “The Everything Store.” Walmart executives have said the marketplace expanded too fast, resulting in some lower-quality items and sellers. Walmart has been on a clean-up mission, but it’s clear that third-party sellers are an important component of Walmart’s digital future.

Compared with other internet middlemen including Walmart and Amazon, eBay takes a relatively small cut of revenue from transactions on its marketplace, on average about 8 percent of the total value of purchases. Similar internet middlemen such as Booking Holdings Inc.’s Priceline or Grubhub Inc. take on average 10 to 15 percent or more of the money from each transaction. StubHub’s average cut is about 23 percent. Elliott’s letter doesn’t address the share of transactions that goes to eBay, but that is a potential area for improvement.

The investor does say eBay has been plagued by technical problems, management missteps and misplaced spending that have hurt marketplace sales growth and profits. And Elliott says eBay missed opportunities to enter valuable corners of e-commerce that left openings for handmade-goods seller Etsy Inc., online furniture retailer Wayfair Inc. and the online classifieds sites LetGo and OfferUp, among other categories. Elliott is right about missed opportunities for eBay, but it’s worth noting that Amazon and Walmart also whiffed in letting those niche players gain traction.

It’s clear that investors don’t have high hopes for eBay, as reflected in the low prices they’re willing to pay for eBay stock. Before Tuesday’s Elliott-related stock jump, shares of eBay traded at about 9.2 times the company’s estimated earnings before interest, taxes, depreciation and amortization for the next 12 months, according to Bloomberg data. That’s less than half of what people are paying for Amazon’s shares, and it’s cheaper even than Walmart and Booking Holdings.

Like previous eBay critics such as the investor Carl Icahn, Elliott is putting its finger on persistent weak spots for the company. There are no easy answers for eBay, and the company could do without the distraction of yet another long investor fight or public negotiations over the right strategy for the company. What Elliott gets right, however, is investors don’t believe in eBay’s direction for its marketplace business, which in principle should be one of the havens of the internet.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

Sarah Halzack is a Bloomberg Opinion columnist covering the consumer and retail industries. She was previously a national retail reporter for the Washington Post.

©2019 Bloomberg L.P.