(Bloomberg Opinion) -- Chief executive officers are going out of their way to brace investors for what could be the worst first quarter in years. As of the end of last week, more than 20 percent of the companies in the S&P 500 had pre-announced details of how they did in the first three months, and nearly 80 percent of them told investors to lower their expectations. But top executives can breathe a sign of relief. It appears investors aren’t all that bothered by potentially lousy earnings.

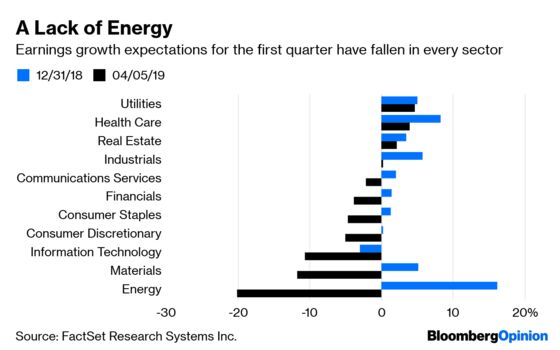

Consider energy stocks. The sector has recorded the largest decrease in expected earnings growth of any sector in the S&P 500, according to FactSet Research. At the start of the year, analysts had expected energy companies’ quarterly profits to increase an average of 16.2 percent compared with a year earlier. Not anymore. They now expect the bottom lines of those same companies to tumble 20 percent. That huge swing in expectations, though, doesn’t seem to have put off investors. Energy stocks are up almost 19 percent since the beginning of the year, making them the third-best-performing sector in the S&P 500.

The best-performing sector of the market this year is the information technology sector, which is made up of Microsoft Corp., Apple Inc. and some other established tech players. Shares there are up 23 percent, including dividends. But just like with energy, those shares have risen as the outlook for those companies’ earnings has withered. Analysts now predict the bottom lines of Microsoft and the others will, on average, drop by double digits, nearly 11 percent. That’s 8 percentage points worse than what analysts had expected at the start of the year.

Earnings estimates for health-care companies have also been cut, but only by 4 percentage points. On average, the companies’ bottom lines are expected to rise 4 percent in the first quarter. That’s the second-highest predicted rise of any sector in the S&P 500. Yet health-care shares are up just 7 percent this year, the worst performance of any sector in the S&P 500.

And it’s not just individual sectors behaving strangely; it’s the entire market. At the beginning of the year, analysts had expected the average earnings of all the companies in the S&P 500 to rise 3.4 percent in the first quarter. The profit picture is now a near-mirror image, with analysts estimating that overall earnings will drop 3.9 percent. Yet the market is up sharply. The S&P 500 returned 13.6 percent in the first quarter, one of the best quarters in years. And it was the first quarter in four years in which the stock market rose while earnings expectations fell.

That’s not how it is supposed to work. The general theory of the stock market is that higher earnings make shares more valuable. By extension, high growth stocks tend to trade at higher price-to-earnings multiples. The price those shares are trading at, whether it is too high or too low relative to earnings — the P/E ratio — also matters. So do interest rates, and some companies are more sensitive to them than others. But new information is supposed to move stocks, and if the fresh information is that a company will earn less, those shares would presumably be worth less and, consequently, their prices could be expected to decline.

The fact that is not happening says something about investors and the current bull market, which has lasted a decade. Investors could be writing off the first quarter as an anomaly, but earnings expectations are starting to slide for the rest of the year as well, though not as severely. Another explanation is the dreaded B-word.

There are a number of ways to tell whether stocks are in a bubble, or at least whether investors’ expectations have become unrealistic. One of them is the P/E ratio, which isn’t a real problem yet. It’s 16.8 based on forward earnings for the S&P 500, which is high by historical standards but considerably lower than where it was at the end of 2017. Another sign is when stocks start trading away from their fundamentals, like earnings. That’s a growing problem, and something that investors should care a lot about.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.