(Bloomberg Opinion) -- DWS Group GmbH is describing 2018 as “an inflection year.” The question for investors is whether that means the firm’s business curve will change from concave downward to concave upward. But for now, the German asset manager remains in a downward tailspin.

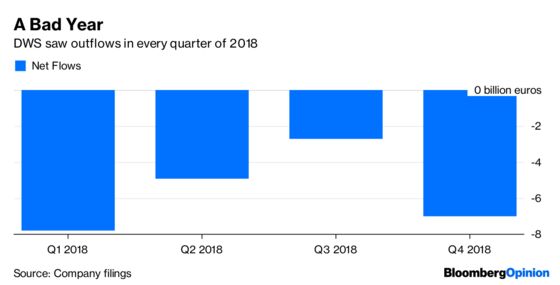

Figures released Friday showed DWS continues to hemorrhage funds. Outflows of 7 billion euros ($8 billion) in the fourth quarter were triple what analysts were forecasting; the 22 billion euros of full-year outflows took assets under management down to 662 billion euros, their lowest in at least two years.

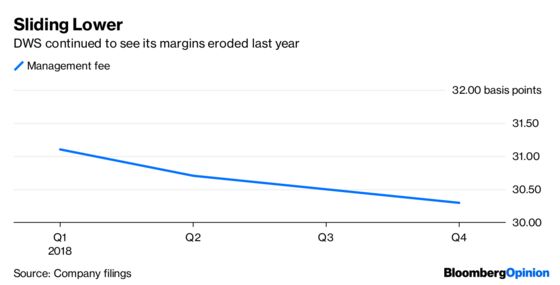

As a result, the management fee the firm is able to charge its customers also declined, barely holding above the 30 basis-point level DWS says is its medium-term target.

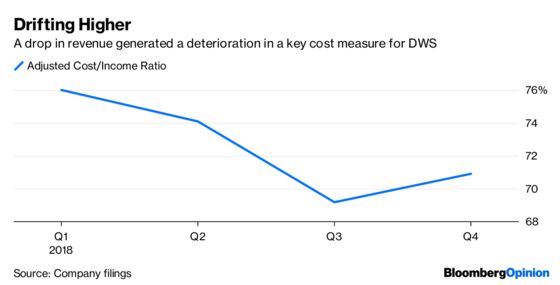

And on its internal business performance, a decline in revenue more than offset improved efficiencies to allow the firm’s cost-income ratio to drift higher in the fourth quarter.

DWS isn’t out of line with its competitors on this measure; Standard Life Aberdeen Plc, for example, has a cost-income ratio of 69.4 percent. But the best-in-class is Amundi SA, Europe’s biggest fund manager with 1.5 trillion euros of assets, which has achieved a ratio of 53 percent. Given the asset management industry’s current straitened circumstances, every company should be aiming to replicate Amundi’s number.

So what needs to go right? DWS says two of the key drivers of last year’s outflows, namely the loss of 10 billion euros from insurance mandates and 11 billion euros of tax-related redemptions by U.S. customers, won’t repeat this year. U.S. tax reform prompted American clients to repatriate billions of dollars, with network equipment maker Cisco Systems Inc. taking home about $5.7 billion it had parked with DWS last year, Bloomberg News reported in August.

In December, the firm added two exchange-traded funds to its range of passive products designed to invest in companies with high environmental, social and governance scores. The combination of increased customer demand for socially responsible products and DWS’s extensive passive-strategy franchise could be a winner for the firm.

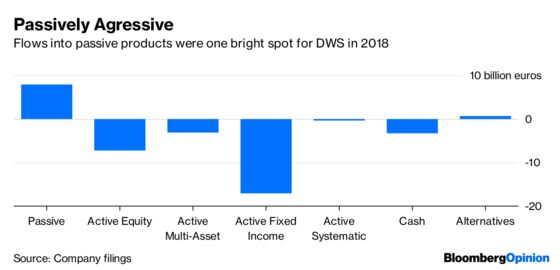

DWS says its share of the European market for exchange-traded products is more than 27 percent. As investors continue to favor low-cost passive strategies, DWS is optimistic it can build on its fourth-quarter success, when inflows of 3.9 billion euros were the best period of last year.

And an improvement in market performance could ride to the rescue of asset managers generally. According to analysts at Deutsche Bank AG, January marked the first month when every one of the 38 asset classes they’ve tracked since 2007 generated a positive total return. Last year, almost every asset class delivered losses. Better market performance typically lures inflows.

In October, DWS ditched its CEO the day after announcing its third-quarter results. Asoka Woehrmann, the former head of retail banking at Deutsche Bank, replaced Nicolas Moreau, who had shepherded the firm through its March listing.

For now, the firm remains at the mercy of the same forces that have trashed its peers. Deutsche Bank, which still owns 78 percent, will need to show more patience with Woehrmann than it did with Moreau if he’s to reverse the 30 percent decline in the company’s shares since its flotation.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.