Don’t Bet on Buybacks to Bail Out the Stock Market

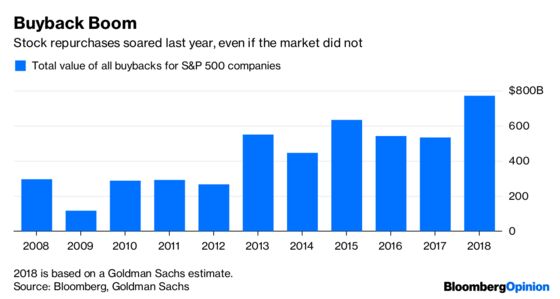

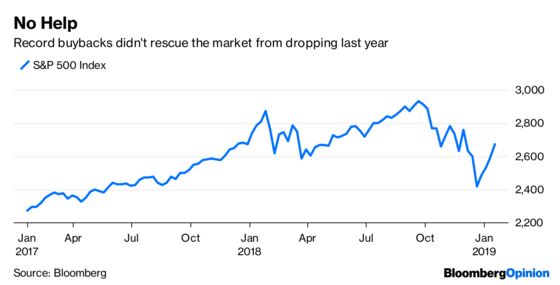

(Bloomberg Opinion) -- Last year’s disappointing market amid record stock repurchases should have taught investors and executives that corporate buybacks are not a panacea. But they appear to have missed the lesson.

Brian Reynolds, a strategist at Canaccord Genuity, wrote in a report last week that the equity bull market will continue in large part because of “debt-fueled buybacks.” And at least some of those buybacks seem to be on their way. Fox Corp. and Charter Communications both did did bond deals, of $6.8 billion and $2 billion, respectively, and said the purpose was to raise cash for dividends and buybacks, though there is nothing forcing them use the proceeds that way.

Even with the existing dry powder, if interest rates rise this year, as many still expect, it seems unlikely buyback activity will be able to match last year’s. If they drop, or stay low, as Canaccord Genuity’s Reynolds envisions in a Goldilocks buyback scenario, that will most likely be the result of a slowing economy, something that repurchases are unlikely to overcome. Moreover, buybacks appear to be making the market less stable, as dips during share repurchase blackout periods have coincided with surges in volatility.

But the greater problem is that buybacks aren’t living up to their promise. They are supposed to boost the value of a company’s stock by lowering its shares outstanding and raising its earnings per share, which in theory should make its remaining shares worth more. Plus, as companies come into the market with cash, they can push up stock prices, like any other buyer. The investors they buy out, the theory goes, can then turn around and invest that money elsewhere, increasing the value of other stocks or making capital available for private companies. Somehow this virtuous cycle didn’t work out last year. Corporate stock repurchases should have boosted the value of the companies in the S&P 500 by 3 percent. Instead, their prices fell 6 percent. Yes, an argument could be made that stocks would have been down even more without buybacks, but the forces arrayed against them still exist, and if a record year for repurchases can’t deliver for investors, they shouldn’t count on buybacks to bail them out this year.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.