(Bloomberg Opinion) -- Germany’s Deutsche Bank AG and its British rival Barclays Plc kicked off the earnings season for Europe’s investment banks on Wednesday. The results weren’t great.

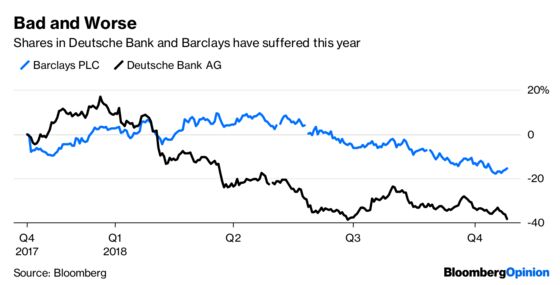

Deutsche’s third-quarter trading revenues were dismal and its net income sank by two-thirds. Barclays’ investment bank fared better but still posted its lowest quarterly revenue in two years. Of the two, it’s Deutsche whose problems run deepest. Its shares sank 4 percent, while those of Barclays rose slightly. But investors in either bank have little cause for excitement.

Growth is proving elusive, with revenue falling at both Barclays and Deutsche. Plus there’s persistent evidence of subdued financial-market volatility (bad for traders), low interest rates and the banks’ own retrenchment plans.

Still, Deutsche matches up particularly badly with the Wall Street giants. Germany’s No. 1 lender suffered 15 percent declines in both equities and fixed-income trading, compared to gains of about 8 percent in equities and falls of about 10 percent in fixed income at Goldman Sachs Group Inc. and Morgan Stanley. Barclays, by contrast, managed to do better than its U.S. peers in both these businesses, which was offset only by disappointing advisory fees.

Christian Sewing, Deutsche’s new CEO, is still trying to hit upon the right size and strategy for its beleaguered investment bank, a decade on from the banking crisis and after three straight years of losses. While he’s indicating a retreat from the U.S. and Asia toward Germany and Europe, his scalpel is being wielded tentatively. Deutsche wants to cut headcount to below 90,000 in 2019 – from about 94,700 today, but it’s holding back from any big exit from a business line.

Even if the bank returns to profit in 2018, investors know the scars will be visible for years. The investment bank’s post-tax return on tangible equity was a measly 1 percent in the third quarter.

Barclays can certainly lay claim to be in a better position, having doubled down on a “transatlantic” investment bank model under CEO Jes Staley, a JPMorgan Chase & Co. alumnus. The unit reported a 7 percent return on tangible equity.

But Staley doesn’t have all the answers either. Shifting more resources to the investment bank has improved returns, but they’re still well below other parts of the Barclays business such as retail banking and credit cards. They’re running at closer to 20 percent. Staley appeared confident when talking about his activist investor Edward Bramson on Bloomberg TV on Wednesday – referring to him as Ed. But if there’s a weak spot for the hedge fund to target, it’s the performance and profitability of the Barclays investment bank.

The roller-coaster world of financial markets aside, the health of these banks still relies heavily on their home turf. While Deutsche’s retail arm Postbank is pumping out loans, it’s feeling the heat from local competitors and low interest rates. Barclays is wary of taking on too much U.K. consumer-credit risk ahead of Brexit, but it’s a big player in the mortgage market there. The broader absence of too many bad loans in Britain has been a big help for Staley. Credit impairments were 254 million pounds in the third quarter, the lowest in at least two years. A combination of a market correction and rising consumer defaults would have a damaging impact on both lenders.

Deutsche Bank is clearly in dire straits, and is valued accordingly at a 70 percent discount to its book value. The Barclays discount is less steep, though it’s still 45 percent. The gap will probably persist. But given the better returns and outlook elsewhere in European finance, Staley and Sewing will both struggle to win around investors.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering finance and markets. He previously worked at Reuters and Forbes.

©2018 Bloomberg L.P.