Deutsche Bank and GAM Cause a Ripple of Excitement

(Bloomberg Opinion) -- After years of false dawns, the European asset management industry may finally be about to embark on a bout of large-scale consolidation. Moreover, there’s the exciting prospect of sales processes developing into auctions as potential acquirers jostle for position in the race to bulk up.

DWS Group GmbH, which is 78 percent-owned by Deutsche Bank AG, is scheduled to report on Friday how its funds fared in the first three months of 2019, after suffering outflows in every quarter of last year. Investors, though, will be more interested in what the management has to say about the persistent speculation that it’s up for sale. Meantime, the troubled Swiss fund manager GAM Holding AG has asked potential buyers to put forward proposals by early May, Bloomberg News reported last week.

The news that GAM was seeking a buyer as the best way out of its self-inflicted mess prompted a spike in the share price, which is now 35 percent higher than this year’s low.

The question facing any potential buyer of the firm and its 137 billion Swiss francs ($137 billion) of assets – which include Switzerland’s Union Bancaire Privee and the French bank Natixis SA, according to Bloomberg News – is whether GAM’s reputation is tarnished beyond repair, or whether a new owner could convince clients to entrust the firm with more of their capital.

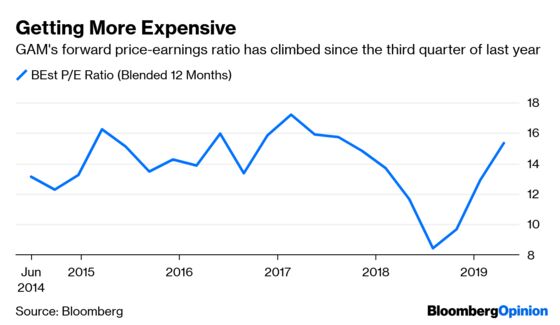

The July suspension of star portfolio manager Tim Haywood prompted customers to accelerate the withdrawal of billions of francs from the firm’s funds and investors to dump the shares. With a market capitalization of about 670 million Swiss francs, GAM is much cheaper than the 2.5 billion francs it was worth a year ago. Given the slump in its business, though, it’s becoming a more expensive target on a price-earnings basis.

Europe’s second mooted asset management candidate for a takeover is a far bigger deal. But if Deutsche Bank is truly willing to contemplate selling more of DWS – and that remains a big if – there seems to be a growing list of suitors. After Bloomberg News reported this month that UBS Group AG might seek to combine its asset management unit with DWS, the Financial Times on Tuesday described the talks as “serious.” Other mooted buyers include German insurer Allianz SE and Paris-based Amundi SA.

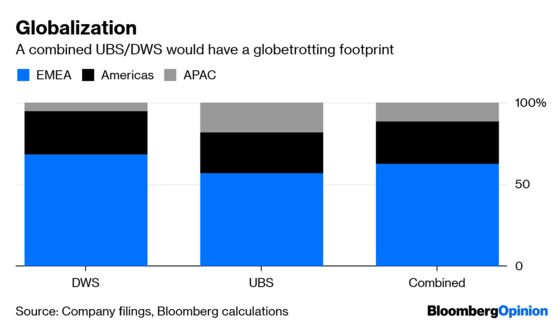

A combined UBS/DWS would have a healthy geographic split, albeit one with more assets concentrated in Europe and fewer in Asia than is currently the case at UBS.

On Wednesday, DWS’s shares finally topped the 32.50 euros that they fetched when Deutsche sold slightly less than a quarter of the firm in an IPO in March last year. They’re up by almost 40 percent this year, more than double the gains seen in the benchmark Stoxx Europe 600 index. The Frankfurt-based fund manager now has a market value of more than 6.5 billion euros.

If a deal with UBS could be structured in such a way that Deutsche Bank retains control of the combined group, it might work. But Amundi has reasons to not let that happen. A UBS-DWS deal would create a European money manager with about 1.4 trillion euros of assets – and that would threaten the French fund’s current status as Europe’s champion, a challenge it is unlikely to back away from.

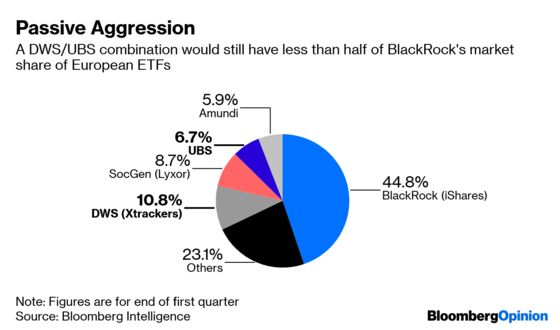

As I argued earlier this month, Amundi would benefit from buying DWS by leapfrogging up the global league tables to about fifth place; it currently scrapes into the top 10. And given its aim of doubling its passive management and smart beta products business by 2023, DWS’s hefty share of the exchange-traded funds market in Europe would be a prize worth fighting for.

All this speculation might come to nothing. GAM may find its brand is too sullied to attract a buyer. Deutsche Bank may not need to raise capital by selling more of DWS – especially if its own merger with Commerzbank AG doesn’t happen. But the challenges facing the asset management industry are piling up, and Amundi has shown that scale can be a valuable defense. Fear of missing out could be a strong motivation for potential acquirers to start a bidding war.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.