Deutsche Bank’s Failure Is Another Bank’s Opportunity

(Bloomberg Opinion) -- The failure of Deutsche Bank AG’s attempted takeover of Commerzbank AG creates the possibility of something more exciting: a cross-border European banking deal involving the smaller German lender. Logic rightly trumped politics in nixing the Deutsche tie-up. The risk is that politics gets its revenge in hampering the future course of Commerzbank.

A Deutsche-Commerzbank deal would have created the appearance of a German national champion. Regulators and shareholders had valid concerns about the systemic risk of such a combination, though, as well as the difficulty of integrating the businesses. Common sense prevailed in killing the idea.

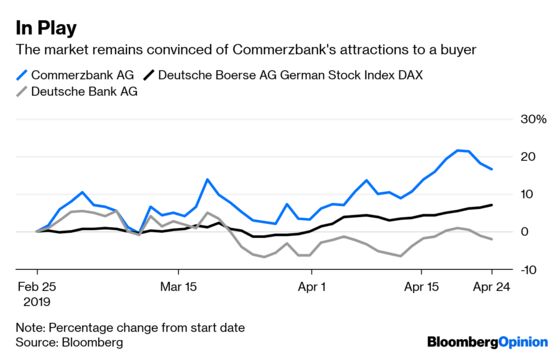

Commerzbank still sounds open to M&A. Its cheap valuation — just 34 percent of book value — belies its strategic attraction, notably a strong position in German banking for small and medium-size companies (the country’s famous Mittelstand).

For regulators and Commerzbank shareholders, a clean bid at a premium by a well-capitalized and well-run European peer would surely be welcome. BNP Paribas SA, with a market value of 58 billion euros ($65 billion), could place equity in support of a cash offer. The French bank has a limited presence in Germany. A takeover would see its culture dominate and its management probably has the capacity to take on the integration.

There are two snags. The first is whether there’s enough upside in the deal for BNP. Limited overlap reduces the scope for synergies to cover any premium offered. Then there’s the political awkwardness of a German entity being acquired by a French bidder at a price that, even baking in a 30 percent premium, would crystallize a loss for German taxpayers. Berlin still owns 15 percent of Commerzbank.

ING Groep NV of the Netherlands would possibly be a more palatable owner, but it’s smaller than BNP and a deal would be a big shift in its strategy.

That leaves a share-based deal with HypoVereinsbank, the German subsidiary of Italy’s UniCredit SpA, looking the most realistic option. UniCredit would potentially receive a controlling stake in the enlarged Commerzbank, depending on how the deal was structured. Politically, that’s probably just about acceptable to both Berlin and Rome.

There are still questions about whether such a deal would replicate too much of the risk of the failed Deutsche Bank tie-up. The merger integration wouldn’t be as painful, but nor would it be clean. It remains to be seen whether a management team could be assembled from the two sides that had the confidence of regulators in taking on such a complicated task.

Cross-border banking M&A will happen one day in Europe, and a deal for Commerzbank might be where it starts. It might even provide an impetus for the completion of Europe’s banking union. But marrying sound business rationale and political buy-in applies to cross-border deals as well as domestic ones.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.