(Bloomberg Opinion) -- Deutsche Bank AG’s decision to abandon an attempted takeover of Commerzbank AG makes sense, but it still leaves both sides scrambling for alternative solutions to the same problem of pathetic returns.

After weeks of deliberations, the German behemoth concluded the benefits would not have offset the “additional execution risks, restructuring costs and capital requirements.”

The rationale is hardly a surprise. As we’ve argued from the outset, the costly and risky combination wouldn’t have addressed the broader structural inefficiencies in German banking, while leaving the enlarged group still exposed to Deutsche’s trading activities and sub-par profitability.

After multiple attempts at a reboot in recent years, Deutsche Bank will probably need to do the next stage of the restructuring on its own. For the smaller Commerzbank, the option of a deal with another European lender may become more likely. A few have already been knocking.

The logic of the transaction was also its main obstacle: The fusion of two domestic firms offered the prospect of considerable savings, and the deal would have effectively created capital by crystallizing a Commerzbank valuation at a considerable discount to its book value.

But while this promised to improve the merged company’s earnings power five years hence, the operation might well have killed the patient in the meantime. The challenge of integrating the two complex financial institutions would have been a huge test for the newish Deutsche chief executive Christian Sewing. The combined balance sheet would have been worth almost 2 trillion euros ($2.3 trillion). That will have made its chief regulator, the European Central Bank, nervous.

The hefty job cuts involved – estimated as high as 30,000 – added to the risk. While Germany may have full employment, and job losses in finance may attract less sympathy than other industries. the deal couldn’t work without unions on board and they were vigorously opposed at both banks.

Deutsche must now revert to its standalone strategy. It will be a long slog. The bank has an enduring cost problem. Cutting back its equities operation and its U.S. activities to create a business more focused on Europe may be a start. But that will be expensive and might require yet more capital from investors.

For Commerzbank, the question is who’s the best parent strategically and politically. Rumored interest from foreign buyers was probably a factor in pushing Deutsche, egged on by Berlin, into talks in the first place. BNP Paribas SA, UniCredit SpA and ING Groep NV are the obvious candidates. Commerzbank CEO Martin Zielke has said doing nothing isn’t an option, which leaves open the option of more domestic consolidation too. The best he can do for his shareholders is to get a clean auction going to flush out the most determined buyer.

UniCredit’s ownership of Germany’s HypoVereinsbank should give it an advantage. That offers scope for domestic synergies and creative structuring. A deal could be structured as a share swap with the Italian bank receiving stock in a combined HVB-Commerzbank, leaving the German state, which owns 15 percent of Commerzbank, invested in an enhanced Frankfurt-listed, Germany-focused lender.

But it would be wrong to rule out other foreign buyers, whose limited geographical overlap would make the path to trade union assent easier.

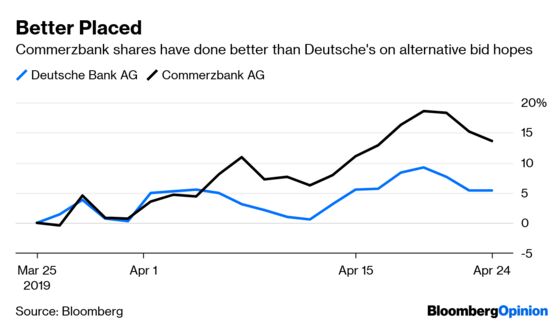

This explains why Commerzbank stock is doing so well. It’s 16 percent above its level on Feb. 6, before speculation of a Deutsche tie-up kicked off in earnest. The DAX has risen since then, but Commerzbank is up twice as much.

Now look at Deutsche. Its shares are back where they were in early February, and have sharply under-performed the DAX and the Bloomberg 500 Index – even after a small bounce on Thursday. The stock trades at 25 percent of estimated book value. Deutsche is more likely to be issuing equity than getting a bid.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

Elisa Martinuzzi is a Bloomberg Opinion columnist covering finance. She is a former managing editor for European finance at Bloomberg News.

©2019 Bloomberg L.P.