Oil Bosses Aren’t Hiring, But They’re Glad You Are

(Bloomberg Opinion) -- Friday’s blowout jobs numbers provided a welcome shot in the arm for oil prices. Up 4 percent as of writing this, West Texas Intermediate topped … $49 a barrel — only a fifth lower than where it was a year ago.

It’s an apt backdrop to the oil and gas payrolls data, much of which comes with a one-month lag to the headline figures. While the past few months have felt like dog years in the oil market, November was when October’s decline turned to a rout, with WTI dropping from $65 to about $50 a barrel. On cue, sector headcount dropped by 2,300 that month, only the second decline in more than two years and the biggest since August 2016 (when oil averaged $45). Yet November also saw record U.S. oil production, if weekly estimates hold.

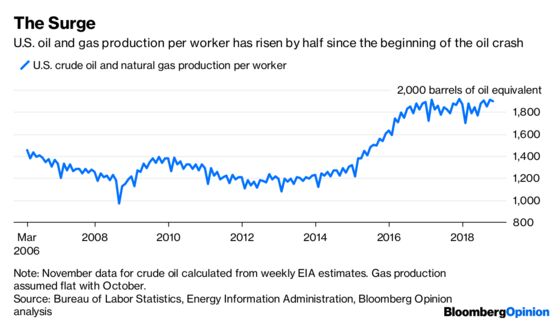

Those layoffs portend a wobbly end to an otherwise solid year. The industry’s ranks swelled by almost 50,000, or about 13 percent, in the 12 months ending November; they’re now back to where they were in late 2015. Production of crude oil and natural gas, however, is up by a quarter over the same time. This has been a productivity story.

The peak, however, was December 2017, and worker productivity seems to have plateaued (although I expect a new peak once December 2018’s data are in). Still, that wasn’t a problem for much of 2018 given the jump in oil prices, with WTI hitting a peak of more than $76 a barrel in early October.

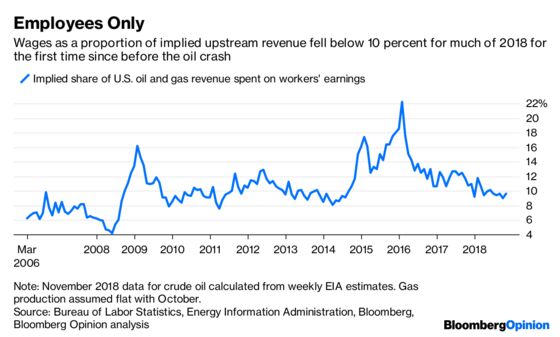

I use monthly production data and payrolls figures to construct a very rough estimate of industry revenue and the proportion of it going to wages (this ignores regional price differences and hedging effects, among other things, so bear that in mind). On this basis, wages dropped below 10 percent of revenue last year for the first time since the summer of 2014, when crude oil still traded north of $100 a barrel:

With productivity gains having topped out, though, prices rule. Plug in current oil and gas spot prices, and November’s implied wage bill would have been 12.4 percent of revenue — summer 2017 levels — rather than 9.6 percent. (It’s worth noting that natural gas prices were exceptionally strong in November, averaging more than $4 per million BTU for the first time in more than four years.)

This helps explain November’s slowdown in hiring and also wage inflation, which fell toward 2 percent, roughly half the rate of a year before. The payrolls data provide another marker indicating the late-2018 drop in oil prices will force exploration and production companies to make good on pledges of spending discipline sprinkled throughout the latest set of earnings calls. WTI at less than $50 a barrel — closer to $40 in the Permian shale heartland — is priced for supply constraint, especially as production per worker suggests productivity gains, impressive as they have been, are slowing.

Yet it’s also worth noting that a $10 swing in the oil price makes a big difference to the wage burden on revenues. The wildcards affecting them this year range from OPEC discipline to White House indiscipline, pulling either way. Demand, especially, is more of a worry than in recent years. On that score, while oil-sector employers didn’t do much for payrolls at the end of 2018, they can only be glad that so many others did.

The sector added an estimated 300 oil and gas extraction workers in December. Extraction workers account for just over a third of the industry workforce, according to Bureau of Labor Statistics classifications. Data for the more numerous support workers lag by one month, hence the focus on November's data.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.