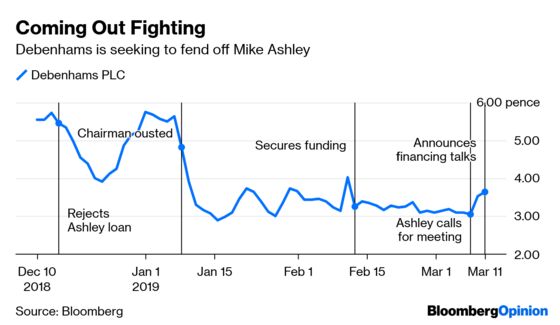

(Bloomberg Opinion) -- As the battle between Mike Ashley and Debenhams Plc becomes ever more acrimonious, the department store chain is stepping up its efforts to see off the retail billionaire.

On Monday, it said it was close to securing about 150 million pounds ($194.9 million) of extra financing. This announcement follows last week’s severe profit warning.

When you are fending off an activist investor or a potential predator – and Ashley is both, given that his Sports Direct International Plc has a 30 percent stake – it’s important to have some good news. And to show that you have a viable standalone strategy.

So the extra funding is welcome. Credit insurers are cutting cover as the store builds up stock for the summer season, so this will help working capital.

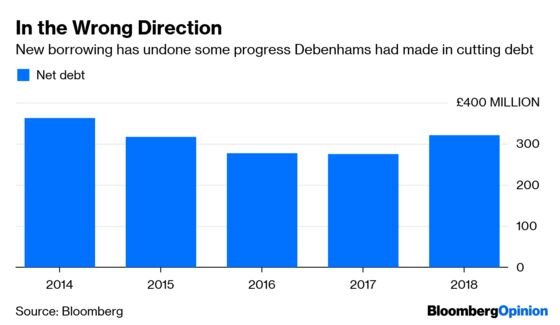

But Debenhams already has heavy borrowings. Even before the extra facilities, analysts at Jefferies estimate net debt to Ebitda at just over three times, the level at which investors start to become nervous.

This is clearly unsustainable given its shrinking profits and lengthy store leases. All the new facilities do is kick these issues further down the road. They will still need to be tackled.

The problems are about to come to a head. Debenhams must hold a general meeting after Ashley called one last week to remove most of the company’s board and install himself as chief executive. I’ve argued he has a good chance of succeeding.

Either way, Debenhams faces an unpalatable choice. If Ashley seizes control at the meeting, he will surely try to prevent any debt for equity swap as this would heavily dilute his shareholding. He wants to put the chain together with his House of Fraser division, and will be working towards this conclusion.

If Debenhams does defeat him, and proceeds to exchange debt for equity, it stands to be taken over by its lenders, including hedge funds that own the debt.

They may take a long-term view of the company and seek to nurture it, in order to achieve a better return on their investments at a later date. But they would also have the leverage to try to extract an attractive price for the business from Ashley.

His mistake was buying Debenhams’ equity, rather than its debt. If he had gone down the latter route he would be in pole position in any restructuring.

Even so, he could end up getting the department store anyway. House of Ashley still looks like the most likely outcome.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.