DBS Hitches a Ride With Go-Jek to Create a Super-App

(Bloomberg Opinion) -- Southeast Asia’s largest bank is teaming up with a unicorn. The prize they may have in mind: a super-app like China’s Alipay and WeChat Pay.

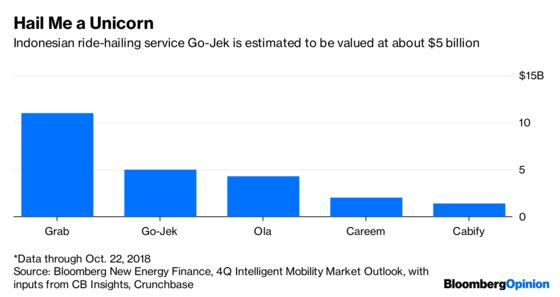

Go-Jek Indonesia PT, which started out as a ride-hailing app, has since gone on to capture a much bigger slice of commerce, including food delivery, courier and hairdresser services, and bill payment. As my colleague Shuli Ren wrote recently, Go-Jek has the advantage of a central bank e-money license in Indonesia, Southeast Asia’s most-populous nation and biggest economy.

So it’s only natural that Go-Jek’s impending expansion into Singapore has made DBS Group Holdings Ltd. sit up and take notice. The lender, which is aggressively embracing technology in its core operations, wants to hail its own ride with Go-Jek if consumers across Southeast Asia use the startup platform to do more than book transportation.

For that’s when DBS can have a rich harvest of user and merchant data to make quick, cash flow-based e-loans to both consumers and small businesses. It is in that context of algorithmic online lending that the regional strategic partnership between DBS and Go-Jek, announced to coincide with the annual Singapore fintech jamboree, assumes importance.

Lending by fintech firms is currently in the throes of a shakeup in China, as smaller players fall prey to tightening regulations and state-mandated caps on interest rates. The consolidation would see an online consumer-loans market, which is expected to be in shouting distance of $1 trillion by 2022, get carved up between the likes of Alibaba Group Holding Ltd.’s Ant Financial and Lufax, backed by Ping An Insurance Group Co.

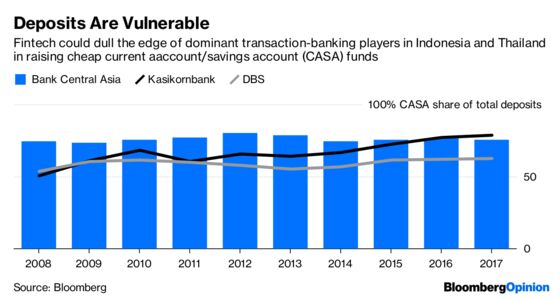

Southeast Asia, meanwhile, would witness another kind of disruption, with banks like Indonesia’s PT Bank Central Asia and Thailand’s Kasikornbank Pcl forced to defend their moats from an assault by nimble technology players.

Their supremacy in transaction banking has rewarded these traditional lenders by making sure around three-quarters of their deposits come from cheap current and savings accounts.

If they lose transactions to the likes of GoJek, which is backed by WeChat parent Tencent Holdings Ltd., then profitability could fade away. In some ways, the process may have already begun. At 26 percent, Kasikornbank’s return on equity in 2004 was double that of DBS. Now the Singaporean bank has almost caught up.

So why’s DBS doing better? The company runs the world’s largest open application programming interface for developers in the banking industry. Open APIs may be the “fastest way for banks to collaborate” with technology firms to cut costs and boost speed, notes Bloomberg Intelligence analyst Diksha Gera, adding that Thailand, Malaysia and Indonesia still need clearer regulatory frameworks.

The payoffs won’t be immediate, and not all of the handshakes will click. But DBS investors should still be watching deals, such as the one with Go-Jek, closely.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2018 Bloomberg L.P.