(Bloomberg Opinion) -- CVS Health Corp. shares took a beating in February after the pharmacy and health-insurance giant delivered a disappointing full-year earnings forecast. So it was a relief of sorts for investors on Wednesday when the company reported first-quarter results that beat Wall Street’s sales and profit estimates. CVS even adjusted its full-year guidance a little higher.

The first quarter marked CVS’s first full reporting period since closing its $70 billion acquisition of insurer Aetna Inc., and one might be tempted to interpret the upbeat results as validation of the company’s transformational M&A strategy. But reshaping its business is a multiyear project, and a few months of results can only tell investors so much.

The first quarter went better than expected, in part due to positive drug-pricing trends. Aetna’s integration is going as planned — CVS is on track to hit the high end of its synergy estimates for the year — and its new insurance business performed well.

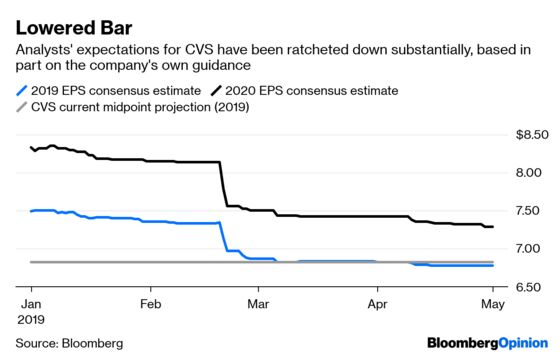

Investors certainly don’t mind the nice start to the year, but they’re really looking towards the company’s forecasts for 2020 and beyond which will be delivered at its investor day on June 4. CVS’s longer-term predictions will tell us how confident it is in its new and bulked-form, and after this quarter’s positives. The company has taken care not to raise expectations too high.

CVS’s commentary on drug-pricing trends during its earnings call suggested that they are more likely to be a headwind than a boost going forward, this quarter notwithstanding. The company’s pharmacy benefit management unit — which negotiates drug costs for health plans — isn’t retaining business as well as it usually does, and the company didn’t have a satisfying explanation for why that’s happening. And while CVS’s synergy targets might be attainable, it has a lot of work to do to prove that paying $70 billion to integrate an insurer and a retail pharmacy was a profitable decision.

All of this takes place against a difficult political backdrop. There are growing bipartisan discussions on drug-pricing legislation that would be a mixed bag for CVS. The Trump administration also still plans to change the way PBMs operate in Medicare, and not to the company’s benefit. More ambitious health-care reform is a more distant concern, but it’s not going to be out of the news or investors’ minds any time soon. The first-ever congressional hearing on “Medicare for All” — a plan that would end much of the company’s business outside of its retail pharmacies — took place on Tuesday and the non-partisan Congressional Budget Office will release a report on the plan Wednesday.

Policy and pricing uncertainty makes it extremely difficult to invest in or forecast the future performance of health insurers and PBMs. That’s compounded for CVS, which is pioneering a brand new business model. The combined company is off to a good start, but its recent guidance and share-price whipsaw suggest the road ahead will be anything but smooth.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.