(Bloomberg Opinion) -- Shares of CVS Health Inc. have been battered in recent months along with other health-care companies amid stepped-up scrutiny of the industry’s pricing practices and calls from lawmakers and the Trump administration to overhaul the current complicated and costly U.S. health system. CVS also has had the added task of integrating Aetna Inc., the insurer it bought for $69 billion in November as part of an ambitious plan to transform itself from a pharmacy giant into a more complete provider of health-care services.

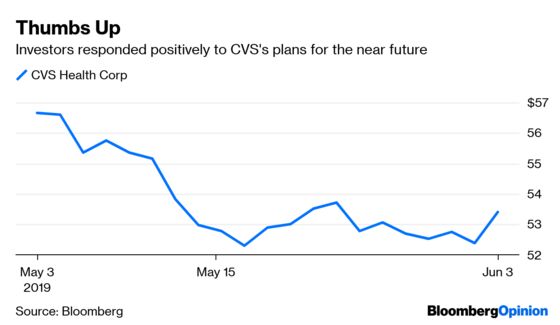

It was against this backdrop, and with CVS’s shares down 31% since completing the Aetna deal, that the company held its much-anticipated investor day Tuesday. It marked the first comprehensive update of CVS post-merger, and was a chance for management to convince shareholders that the combined company was up to the challenges ahead and moving in the right direction. Based on the stock’s initial positive reaction, investors seem to have liked what they heard. That upbeat vibe isn’t misplaced.

CVS’s most promising initiative is the rapid expansion of its new “HealthHub” store model, which includes substantially more health-care services and expanded clinics. At these locations, CVS says it can offer about 80% of the services your average primary-care practice provides, as well as some things that they don’t. This includes everything from traditional urgent care to sleep-apnea screenings.

The company started the year by opening three HealthHub locations in Houston. It plans to open 1,500 locations by the end of 2021, with the rollout focused on the Philadelphia area, Atlanta and Tampa, Florida, in addition to its initial target market of Houston. It’s a lofty goal and may make hitting its financial targets that much more difficult, but it’s a worthwhile long-term investment.

Transforming standard pharmacies into something more is key to making the Aetna purchase pay off. The company’s massive physical reach differentiates it from large rivals like Cigna Inc. and UnitedHealth Group Inc., which also manage both health-insurance and prescription-drug plans.

The new services focus in large part on patients with high-cost chronic conditions like diabetes. CVS argues that it has an advantage in reaching what’s historically been a tricky and expensive population. Because it’s an insurer, it knows when someone is overdue for a diabetes checkup and it can can remind them when they arrive at the pharmacy counter. CVS can schedule and provide that appointment, and also can arrange follow-up interventions like a consultation with a dietician, helping patients better adhere to their care plans so they stay healthier and avert the need for costly measures in the future.

Success would pay off handsomely. Keeping spending in check for patients with chronic conditions could make Aetna significantly more profitable and competitive, while revenue from services would keep more health spending profitably in-house and boost the financial performance of its stores. That would come in handy amid pricing pressures and Amazon.com Inc’s entry into the mail-order drug business. The new model also diversifies CVS away from its prescription-drug plan management business, which has lost business recently and is exposed to significant regulatory pressure.

That isn’t to say it will be easy. CVS plans to transform 1,500 stores; it currently only has 1,100 locations that even have clinics, some of which will be expanded. Executives pointed to positive early anecdotes and data, but the combined company is still young and the cost savings are theoretical. This expansion won’t be cheap, and it will have to be balanced with debt reduction and a target of double-digit earnings growth by 2022.

Regulatory risk, heightened bipartisan scrutiny and ambitious health-reform plans put forth by Democrats have given investors reason to be antsy; the negative reaction to any failure on CVS’s part to meet expectations will be swift and substantial. Still, the company is right to keep pushing forward with its plans. In the end, mild tweaks to the status quo won’t be enough to bring down costs or stand out in a competitive and unstable market.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.