(Bloomberg Opinion) -- Wall Street analysts have been lowering the bar for 2019 earnings for the past few months. But their expectations may not have fallen far enough.

Fourth-quarter reports are offering early evidence of that. The latest big example was JPMorgan Chase & Co., which on Tuesday reported results that missed expectations for the last three months of 2018. It was the first time the bank had not exceeded quarterly expectations in two years and its biggest miss in nearly five. More disappointments are probably on the way. A number of companies, including and most notably Apple Inc., have already said profits and sales will be lower than previously expected this year.

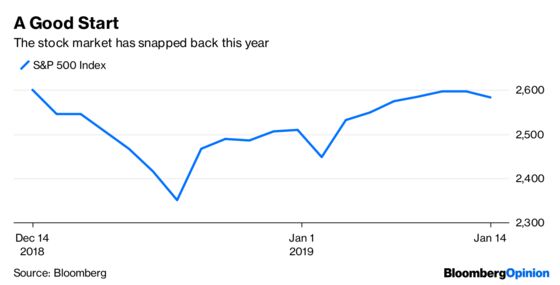

In October, analysts were predicting that the companies in the S&P 500 Index would boost their earnings by 11.5 percent in 2019. Since then, projections for earnings growth have slumped to just more than 7 percent. Worries about growth intensified as those estimates dropped, and markets sold off. Investors appear to have come to grips with those lower estimates, though, perhaps because of comments from the Federal Reserve or perhaps because prices adjusted. The stock market has been rallying recently and was up again on Wednesday, with the S&P 500 now registering a gain of more than 4 percent for 2019.

That 7 percent income growth would appear attainable, given that the S&P 500’s earnings rose 24 percent last year. Analysts expect that, including the tax cut, 107 companies in the S&P 500 will grow as fast or faster in 2019 than they did last year. Earnings growth will slow or even drop for the rest, which seems appropriate given the impact of a trade war, government shutdown, slowing global economy and comparison with a tax-cut-turbocharged year. Moreover, corporate profits and the U.S. economy have been expanding for a while and are most likely due for a breather.

The main problem is that last year’s growth was largely a mirage. I recently calculated that Donald Trump and the Republicans’ 2017 tax cut boosted profits for the S&P 500 companies by $144 billion last year, about half of overall earnings growth when analysts had been expecting it to account for about a third.

But analysts are still predicting that, excluding the tax cut, as many as 219 companies will be able to increase their operating earnings more in 2019 than they did last year. That seems less realistic. Some of the companies did have a disappointing 2018, with earnings dropping or slowing. So a rebound, even with a slower economy, may not be out of the question. But others had solid earnings increases, even without the tax gains, and analysts are still expecting better numbers this year. That looks like a recipe for disappointment.

Those higher numbers may not be out of reach for Cigna or Southwest, but they seem like a stretch, not just for them but the other companies that analysts are expecting to deliver big. Investors should be cautious about the tax-cut tailwind reversing course.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.