This Stock Market Can Be Awfully Deceiving

(Bloomberg Opinion) -- When the S&P 500 Index surged on Tuesday to its highest in five weeks, bringing its rally since bottoming on March 23 to 27%, the sense was that the market was signaling that the worst from the coronavirus pandemic would soon be over. On Wednesday, though, the benchmark took a hit, falling by more than 2% as data on U.S. retail sales and factory output for March posted historic declines. Other figures measuring economic activity for April also suggested a very deep recession is in play.

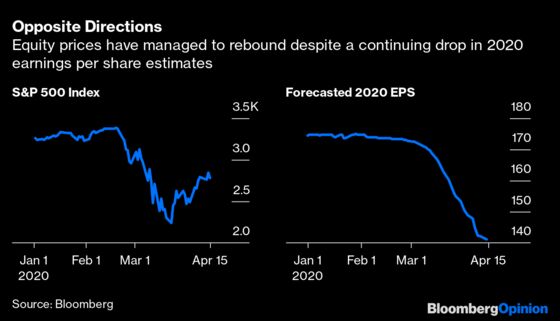

The recent rebound in equities had made stocks as expensive as they have been at any point during the past two decades based on one key measure: The S&P 500 was trading at about 20 times this year’s estimated earnings. Problem is, analysts have only started cutting their 2020 profit forecasts, dropping them to $141 a share on average for the index from $175 in early January, according to data compiled by Bloomberg. Those forecasts are likely to go far lower as companies report first-quarter results over the coming weeks and executives update their outlooks. It’s not hard to imagine investors questioning why they are paying so much for earnings that are likely to keep shrinking. During the 2008-2009 financial crisis, profit estimates came down by just over 30%. If we see the same thing happening now, which is a conservative estimate, then projections will drop to around $120 a share, implying a price-to-earnings ratio for the S&P 500 of about 23. “Even with $4 trillion of direct and indirect stimulus” from the Treasury Department and Federal Reserve, “the current level of the S&P — over 2,800 — is completely unjustifiable,” the strategists at Cantor Fitzgerald wrote in a Tuesday research note.

If economic optimism wasn’t responsible for the recent rise in stocks, then what was it? Medley Global Macro Managing Director Ben Emons figures it was nothing more than cheap money. The Fed’s efforts at cutting interest rates and getting capital flowing into the credit markets reduced the weighted average cost of capital for members of the S&P 500 by 3.5 percentage points on average since March 23. So based on traditional relationships between stocks and the cost of capital, the Fed’s efforts account for almost 95% of the S&P 500’s rebound, with only 5% due to any of notion that the worst is over, according to Emons.

DALIO’S NOT WRONG ABOUT BONDS

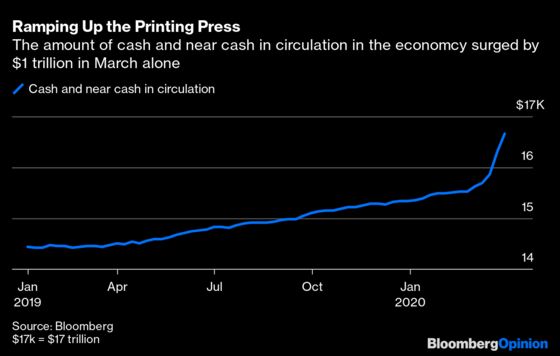

Not a lot has gone right for legendary investor Ray Dalio lately. The flagship hedge fund at his Bridgewater Associates ended the first quarter down about 20%, getting caught on the wrong side of the stock market sell-off that began in late February, Bloomberg News reported earlier this month. In all fairness, most everyone except the perpetual uber bears have had a tough time. So even though U.S. Treasuries rallied this week, just as Dalio said investors would be “crazy” to hold government bonds now, it doesn’t mean he’s wrong. In fact, he’s likely to be proven correct. “If you’re holding a bond that gives you no interest rate, or a negative interest rate, and they’re producing a lot of currency and you’re going to receive that, why would you hold that bond?,” Dalio said Wednesday on the Bloomberg Invest Talks webcast. In March alone, the amount of dollars in circulation as measured by M2 — which is cash, checking deposits, savings deposits, money market funds and other items defined as “near money” — soared by $1.05 trillion to $16.7 trillion. To put that in context, the most M2 ever increased in a whole year was $967 billion in 2019. One consequence of a sudden surge in the money supply is the potential for inflation to suddenly accelerate, eroding the value of bonds’ fixed-interest payments over time and making the securities worth much less. As it is, with rates at record lows, real yields, or those after taking into account inflation, are negative 1.45%.

ABOUT THAT HISTORIC ‘BIG OIL DEAL’

After inserting himself into global oil talks, President Donald Trump hailed the historic agreement among the world’s top producers on Sunday to cut petroleum output by almost 10%. What Trump called the “big Oil Deal” was supposed to reverse a devastating price war that saw oil prices tumble 66.5% in the first quarter, saving what he estimated to be hundreds of thousands of American jobs. There’s just one problem: oil prices have continued to drop. West Texas Intermediate crude fell to as low as $19.20 a barrel on Wednesday, a price not seen since 2001. The issue is that there was a glut of oil even before the sudden stop in the global economy, and a reduction in production isn’t likely to end that situation anytime soon. The International Energy Agency said Wednesday that oil demand is heading for the biggest annual collapse in history, with global consumption tumbling by as much as a third this month amid lockdowns aimed at containing the coronavirus, according to Bloomberg News’s Grant Smith. The world may run out of space to store unwanted crude in a matter of months, which may push prices even lower. “When we look back at 2020, we may well see that it was the worst year in the history of global oil markets,” said IEA Executive Director Fatih Birol. Now, Bloomberg News reports that the Trump administration is considering paying U.S. oil producers to leave crude in the ground to help alleviate the glut.

AND THE WINNER IS…

The British pound is proving to be a surprising haven as the coronavirus pandemic spreads around the world. Sterling is up 3.73% against a basket of nine other developed major currencies over the past month. That’s the best performance among the group, better even then the dollar’s 1.27% gain and the yen’s 1.41% increase. The thinking here is that the pandemic means the deadline for a trade deal this year between the U.K. and European Union as part of the “Brexit” process will be pushed back, removing a major risk hanging over the pound, according to Bloomberg News’s John Ainger. The U.K. could even see more favorable terms from any trade deal, with the crisis shining a light on the EU’s struggles in dealing with an issue that affects different countries within the bloc disproportionately. “The stigma of being associated with the EU — and the euro zone in particular — will only increase as a result of the coronavirus crisis,” Standard Bank’s head of foreign-exchange strategy Steven Barrow wrote in a research note. “We’ve long had our sights on a return to 0.80 over the coming year for euro-sterling (a sterling rise of nearly 10%) but now we are starting to think that this might be a bit too conservative.” The sterling-euro exchange rate was trading at about 0.87049 on Wednesday.

TEA LEAVES

Once again weekly new U.S. jobless claims will take center stage Thursday as market participants attempt to square real-time economic data with the dire projections. The median estimate of economists surveyed by Bloomberg is for 5.46 million new claims, down a bit from the 6.61 million record last week. Still, the range of estimates are all over the place, from 2 million to 8 million, showing economists are still struggling to accurately assess an economy suffering from a sudden stop. There’s more on tap than just jobless claims, with U.S. housing starts for March seen dropping 18.7% to a 1.30 million rate from 1.60 in April, and the Federal Reserve Bank of Philadelphia’s regional manufacturing index tumbling to negative 32 for April from negative 12.7 in March. None of these numbers are likely to engender any confidence in economists or market participants.

DON’T MISS

Money Is In Jeopardy of Losing All Meaning: Jared Dillian

Virus Recession Gives Economists Shot at Redemption: Noah Smith

Gold Shines 50 Years After Nixon. Will Netflix?: John Authers

Reopening the Economy Is More Ethics Than Science: Faye Flam

One Contagion Is More Than Enough for India: Andy Mukherjee

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Robert Burgess is the Executive Editor for Bloomberg Opinion. He is the former global Executive Editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2020 Bloomberg L.P.