Powell Slams Door on Trump’s Negative Rates ‘Gift’

The evidence on the effectiveness of negative rates is very mixed, This is not something that we’re looking at, Powell said.

(Bloomberg Opinion) -- Federal Reserve Chair Jerome Powell made two things clear during much-anticipated remarks on Wednesday. First, fiscal policy might need to do more to combat the lasting economic damage from the coronavirus pandemic. Second — in what markets were most eager to hear — he’s not about to steer the central bank down the path to negative interest rates.

“The evidence on the effectiveness of negative rates is very mixed,” Powell said Wednesday in a webinar hosted by the Peterson Institute for International Economics. To hammer home the point: “This is not something that we’re looking at.”

“It’s an unsettled area, I would call it,” he said. “I know that there are fans of the policy, but for now it’s not something that we’re considering. We think we have a good toolkit, and that’s the one we’ll be using.”

What was left unsaid, of course, is that one such fan is President Donald Trump, who tweeted on Tuesday that “as long as other countries are receiving the benefits of Negative Rates, the USA should also accept the ‘GIFT’. Big numbers!” Given his background in real estate (and racking up debt), it’s hardly a surprise that he’s enamored by the concept of being paid to borrow. This wasn’t the first time he endorsed the policy, and it certainly won’t be the last. Still, markets have largely become accustomed to tuning out the president’s off-the-cuff musings on monetary policy.

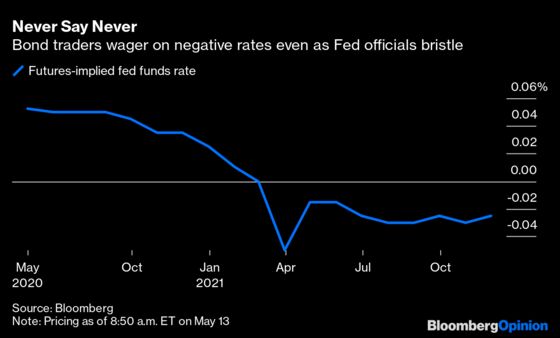

Recently, however, the interests of bond traders and Trump have aligned. For days, fed funds futures have been pricing in a policy rate that’s below zero as soon as next year, even though current officials have widely indicated such a move is not in the cards. Here’s what that looked like before Powell spoke:

The hedges gained traction on May 7, the day after DoubleLine Capital Chief Investment Officer Jeffrey Gundlach said on Twitter that pressure will build to take the fed funds rate negative because the Treasury was borrowing so much with short-term bills (some of those rates have already fallen below zero in secondary trading). Then, Atlanta Fed President Raphael Bostic vowed the central bank would deploy its full arsenal to aid the economy and would err on providing too much support, not too little. “It is really a whatever-it-takes scenario,” he said, echoing the famous phrase from Mario Draghi when he was president of the European Central Bank.

The impulse makes some sense logically. If a trader had to bet on the direction of the fed funds rate in the coming year, it would have to be down. As Powell made clear after last month’s Federal Open Market Committee meeting, the central bank will be in no hurry to tighten monetary policy. He hinted during his remarks Wednesday that it could be a “few years” before the economy has truly recovered. More immediately, U.S. unemployment is at levels not seen since the Great Depression. It all would seem to add up to Fed officials pressured to do “more.”

In a somewhat unusual stance for a Fed leader, Powell is imploring lawmakers to take further action, rather than the central bank. “This is the time to use the great fiscal power of the United States to do what we can do to support the economy and try to get through this with as little damage to the longer-run productive capacity of the economy as possible,” he said after the April FOMC meeting. The federal stimulus law has allocated some $454 billion in equity funding already for the Fed’s various lending facilities.

He reiterated that view on Wednesday. “Additional fiscal support could be costly, but worth it if it helps avoid long-term economic damage and leaves us with a stronger recovery,” Powell said at the end of his prepared remarks. “This trade-off is one for our elected representatives, who wield powers of taxation and spending.” He added later that the goal should be boosting the economy such that it’s growing at a faster pace than the national debt.

Powell didn’t entirely erase the negative fed funds pricing in futures markets — “for now” implies there’s a chance down the road. But he slammed the door as forcefully as he could on the policy while still preserving the central bank’s coveted “optionality.” It’s not that he wants to eradicate negative-rate bets, per se, he just doesn’t want to get boxed in by the markets.

His comments should be put in the context of those from other Fed officials this week, who seemed committed to playing down the appeal of a negative fed funds rate. “I am not a big fan of going into the negative rate territory,” Bostic said on Monday. As if to clarify his point from last week: “Negative rates is one of the weaker tools in the tool kit. I am not anticipating supporting that anytime soon.” Just for good measure, Chicago Fed President Charles Evans added: “At best, we’d have to study it more, but I don’t anticipate that being a tool that we would be using in the U.S.” Minneapolis Fed President Neel Kashkari insisted “there are other tools we would go to first.”

In truth, this is not a new stance. Powell said during congressional testimony in February that negative interest rates can damage bank profitability, which worsens overall credit expansion. He brought up that issue again on Wednesday. Back in November, Fed Governor Lael Brainard made it clear that the central bank would first opt for enhanced forward guidance and some form of yield-curve control at the zero lower bound.

Importantly, as I pointed out last month in a column arguing against negative interest rates, rather than stimulate economic activity, the policy might actually be disinflationary. That’s a scary proposition for Fed officials given that a report Tuesday showed the core U.S. consumer price index fell 0.4% in April from a month earlier, the biggest drop on record.

There’s a long road to a full economic recovery, and missteps will be costly. The Fed has already pledged to support the credit markets to avoid turning “liquidity problems into solvency problems.” It still has to get lending facilities up and running to support municipalities and Main Street, which will have tangible and obvious economic benefits. Powell is no gambler, which is why negative interest rates will remain buried deep in the central bank’s toolkit.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.