Jamie Dimon Can’t Hold Back His Competitive Side

The latest memo from Jamie Dimon reads like nothing short of a kumbaya moment from the billionaire who leads biggest U.S. bank.

(Bloomberg Opinion) -- At first glance, the latest memo from JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon reads like nothing short of a kumbaya moment from the billionaire who leads the biggest U.S. bank.

Ahead of JPMorgan’s annual shareholder meeting, Dimon highlighted a $250 million global business and philanthropic commitment that will help “vulnerable and underrepresented communities”; a collaboration with Marriott International Inc. and others that will provide up to $10 million of hotel stays for health-care workers addressing Covid-19 in the U.S.; a lifeline to “hundreds of thousands of homeowners” to delay mortgage payments for three months; and almost $1 billion in new loans for small-business clients. The list goes on.

The numbers that stuck out to me, however: JPMorgan has helped investment-grade companies raise $664 billion and an additional $104 billion in high yield so far this year. It’s not entirely clear what “helped” means, but the bank’s earnings presentation last month said it had “helped clients raise $380B+ through the investment-grade debt market in 1Q20,” implying that whatever the criteria, it has done an additional $284 billion of it in the second quarter with six weeks to go.

April was a record month for the broad high-grade bond market, with some $300 billion of deals pricing, and May has shown little signs of slowing down with about $168 billion in the books. High-yield volume rebounded in April to $37.3 billion, the most in a month this year, and so far an additional $23.8 billion has priced in May. As Federal Reserve Chair Jerome Powell said in his “60 Minutes” interview about the central bank’s corporate credit facilities, “we haven't actually had to lend anyone any money because now the markets are working because the markets know that we’re there.”

Functioning bond markets might be enough for Powell, but for Dimon and his counterparts like Bank of America Corp.’s Brian Moynihan, it’s still market share that matters. In a subtle way, Dimon might have been letting his competitive side show by lauding the bank’s underwriting figures so far in 2020.

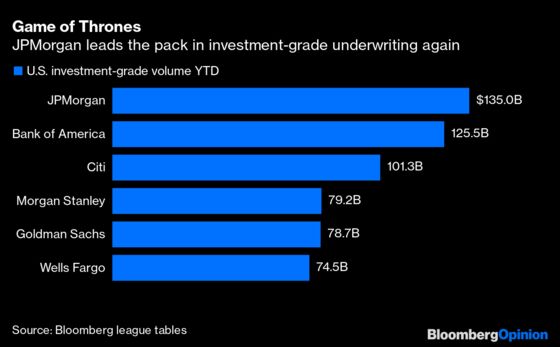

According to Bloomberg’s league tables, JPMorgan finished No. 1 in both investment-grade and high-yield underwriting in 2019. As it stands now, JPMorgan is on track to reclaim its titles in 2020. A back-to-back finish atop the rankings hasn’t happened for the bank since 2013, which capped off a four-year string of first-place finishes after the last recession.

The league tables, which use a stricter criteria on which deals qualify for a given bank, show just how slim the margins can be at the top. For instance, Bank of America snatched first place in investment-grade underwriting in 2018, the only time in the past decade that JPMorgan didn’t hold the top spot. The two banks underwrote $141 billion and $139.9 billion, respectively. That same year, JPMorgan edged out Credit Suisse in high yield, $17 billion to $16.1 billion.

So far in 2020, JPMorgan has increased its investment-grade market share year-over-year by 3.28 percentage points, more than any other bank. Its closest competitor, Bank of America, has increased its share by 2.21 percentage points. In high yield, Bank of America has picked up the most market share and has done the most deals, though it still trails JPMorgan in overall volume, according to the Bloomberg league tables.

All this is to say, fees from debt underwriting will play an important role in the second-quarter earnings results of the biggest U.S. banks. With Treasury yields near record lows, net interest income will inevitably come under pressure. Market volatility is nowhere near the levels seen in March, as measured by the VIX Index, which means trading revenue won’t be the lifesaver it was in the previous quarter. And provisions for credit losses will still eat into profitability. One of the few constants so far in the second quarter has been the flood of new bond deals hitting the market.

JPMorgan and other big banks are clearly trying to tone down their competitive side during this pandemic to avoid appearing greedy during a time of fear. As I’ve said before, bankers are positioning themselves to be the good guys in this crisis, given that they’re well capitalized and have the capacity to be there for clients, unlike in 2008.

Dimon’s memo, in that sense, effectively summarizes the mood. “Let’s leverage this moment to think creatively about how we can mobilize to address so many issues that inhibit the creation of an inclusive economy and fray our social fabric,” he wrote. “By doing the right thing during times of crisis, we can emerge stronger and more cohesive in its wake.”

At the same time, he has an obligation to have JPMorgan emerge stronger from this economic downturn as well. Part of that is keeping a tight grip on its debt-underwriting throne.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.