China Is Perfectly Prepared to Fight the Last Virus

The economy has a much more sophisticated array of tools to boost growth than during SARS. Unfortunately, its problems are bigger

(Bloomberg Opinion) -- China has a bigger and more sophisticated toolbox to combat any economic slowdown from the coronavirus than in 2003, when it battled the SARS pandemic. The challenge now is a worsening backdrop both domestically and abroad, and how both hamper the effectiveness of Beijing's response.

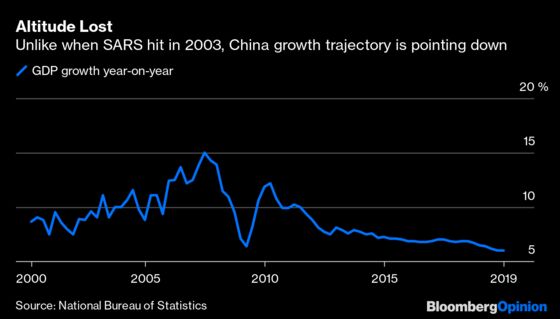

It's hard to be precise about the damage given the situation is still unfolding. Bloomberg Economics is likely to downgrade its projection for China’s first-quarter growth from its current forecast of 5.9%. When Severe Acute Respiratory Syndrome raged in the second quarter of 2003, China's expansion cooled to 9.1% from 11.1% in the prior three months.

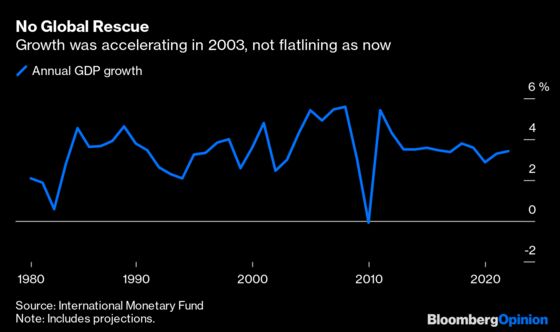

Trouble is brewing beyond China's shores, too. With trade wars, heightened tension between Iran and the West and declining demographics, there were plenty of challenges before this outbreak. The International Monetary Fund is penciling in growth of 3.3% this year, after crawling along at 2.9% in 2019. Yet that pace has stalled from the 3.4% estimate just a few months ago. In 2003, the world economy expanded more than 4% and approached 6% in 2007.

China has changed dramatically in the past 17 years. For starters, its economy is roughly eight times the size. But on a more granular level, key elements of monetary- and currency-policy frameworks have evolved. Most notably, the country has a more flexible exchange rate, to put it mildly. While the central bank still manages the contours of the yuan's moves, the currency was pegged at 8.3 to the dollar for a decade until July 2005. Moreover, the People’s Bank of China now uses an array of rates to manage borrowing costs. In 2004, it was considered almost revolutionary when China raised interest rates, a measure that hadn’t been deployed as a tool of economic management in nine years.

These changes allow policy shifts to come more frequently. Faced with the trade war and a cooling domestic economy, the PBOC began 2020 with a statement of intent: The central bank cut the required reserve ratio for lenders by half a percentage point, the latest in a series of reductions. This signals that officials were aiming to shore up liquidity in the private sector well before the Wuhan outbreak. Damage from the coronavirus might conceivably tip the central bank's hand.

Yet China’s perilous corporate-debt burden could remain a constraint. Over the course of last year, worries that a benchmark interest-rate cut wouldn't reach the private sector kept the PBOC from acting, despite expectations it would do so. Whether easier monetary policy in China would trickle through the rest of the global economy remains an open question. Many multinational firms have already started to relocate their supply chains as a result of the trade war.

When SARS broke out, China was still basking in the glow of its entry to the World Trade Organization in late 2001. Six years later, growth reached a peak of 15%. Executives and officials the world over marveled at the mainland economy and Beijing’s decision-making prowess. Globalization was still very much in vogue and China became shorthand for a flattening world. Few dared offending Beijing, let alone consider imposing tariffs. (The idea of a trade war horrified President George W. Bush’s administration.) American economic diplomacy amounted to the Treasury Department’s gentle prodding that maybe China could, pretty please, end the yuan's hard peg to the greenback.

Many of the people who went out of their way to praise China also urged it to rebalance its economy, to focus less on exports and investment and more on consumption. That shift has largely happened. But now China is more susceptible to changes in household sentiment — precisely the slice of the economy that a fresh outbreak will hit hardest. Since late last week, travel has been curtailed and Lunar New Year holiday activities were curbed in many parts of China.

The good news is that Beijing can deploy more weapons to address this slowdown than in 2003. But given the scale of the changes since then, that may not matter much. Nor will this arsenal be particularly effective if the global economy, which China feeds and relies upon, remains a shadow of its former self.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2020 Bloomberg L.P.