Alphabet's Google Ad Cliff Is Manageable, for Now

Alphabet, the parent of Google, is facing one of the most difficult internet ad-spending markets in its history

(Bloomberg Opinion) -- Alphabet Inc., the parent of digital-search giant Google, is facing one of the most difficult internet ad-spending markets in its history. The company’s recent actions signal it is taking the prospect of a downturn seriously.

Late Tuesday, Alphabet reported March-quarter sales results that beat Wall Street estimates. The company posted first-quarter revenue ex-traffic acquisition costs of $33.7 billion, up 14% from a year earlier, versus the $32.6 billion Bloomberg consensus. In its earnings release, CFO Ruth Porat said the company’s performance was strong during the first two months of the quarter, before experiencing a “significant slowdown in ad revenues” in the month of March. She added on the investor call that the company hasn’t seen a further deterioration thus far in April, but cautioned the second quarter will be a “difficult one” for the company. Alphabet shares climbed 7% in post-market trading, after a 3% decline during the regular session, with investors seemingly taking solace that the environment hasn’t gotten materially worse in recent weeks.

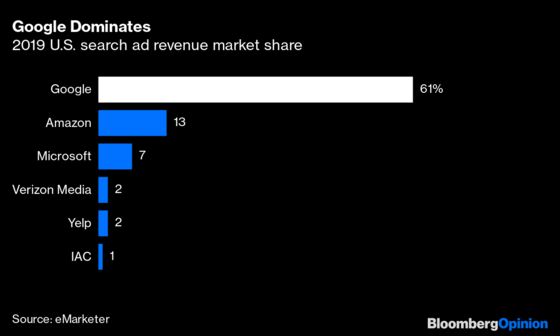

The backward-looking results aren’t as important, compared to what lies ahead — and the future still looks murky. Alphabet simply won’t be immune to the impending global recession triggered by the Covid-19 pandemic. For all of its disparate subsidiaries, the company’s core business is still paid search advertising. To illustrate, RBC Capital Markets estimates the Google search engine accounts for more than 80% of Alphabet’s earnings.

On the earnings call, management repeatedly said Google’s ad business is dependent on an improvement in the macro-economic environment. That’s a problem, as many industries that are key advertising customers are seeing their revenues plummet — including travel, physical retail stores, restaurants, outdoor entertainment, autos and apparel. As a result, these sectors are likely to slash their marketing budgets for the next few quarters. According to a recent survey by the Interactive Advertising Bureau, 70% of advertisers have already cut their digital ad spend budgets by one-third on average for the March to June time period, with paid search plans down 25%.

While Alphabet says it will invest in its long-term opportunities, it is also clearly aware it can’t continue business as usual. Earlier this month, CEO Sundar Pichai sent an email to his staff, saying the company will “significantly slow down” the pace of hiring and adjust its pace of investments. And last week, CNBC reported the company plans to cut marketing budgets by as much as 50% for the second half of the year, citing internal documents. The company confirmed it will reduce spending on promotions during the earnings call.

But still, Alphabet is prudent to hunker down with the internet ad cliff likely upon us. It will weather the pandemic and come out on the other side, but many of its customers will not.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tae Kim is a Bloomberg Opinion columnist covering technology. He previously covered technology for Barron's, following an earlier career as an equity analyst.

©2020 Bloomberg L.P.