Victor Li Shares Hong Kong’s Image Problem

Asia’s sprawling family-controlled groups have continued to thrive. That’s not to say they’re free of challenges.

(Bloomberg Opinion) -- The slow death of the conglomerate has been a theme in the developed world, exemplified this year by the decline of General Electric Co. to a shadow of its former self. By contrast, Asia’s sprawling family-controlled groups have continued to thrive. That’s not to say they’re free of challenges.

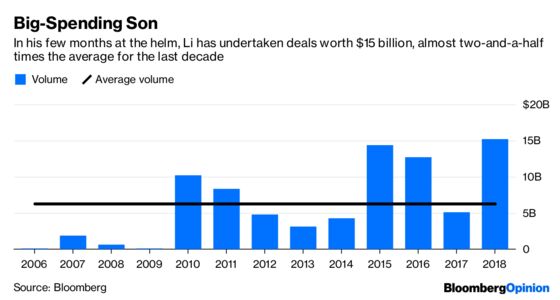

Victor Li, 54, sits atop a global empire spanning telecom, ports, real estate, retail and energy that was built by his father, the legendary Hong Kong billionaire Li Ka-shing. Seven months after taking over from CK Group’s 90-year-old founder, the younger Li must confront a more protectionist landscape that poses a threat to its strategy of diversifying away from its home city and China.

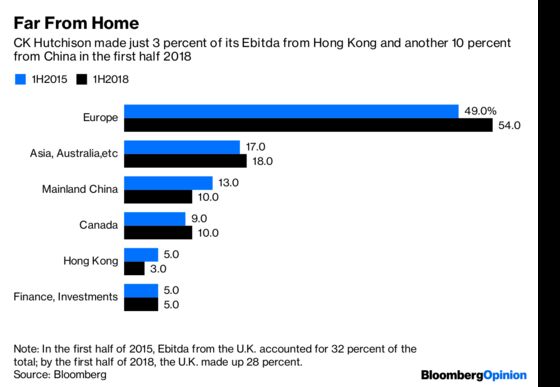

The core of the Stanford University-educated engineer’s problem is this: Being a Hong Kong company no longer shields CK from a backlash against Chinese expansion.

The rejection of what would have been CK’s biggest acquisition came amid growing concerns about Chinese investment in critical industries. In August, Australia’s government banned China’s Huawei Technologies Co. and ZTE Corp. from supplying next-generation wireless equipment to the nation’s telecom operators. The vetoing of the APA deal reinforced impressions that regulators are no longer discriminating between Hong Kong companies and those from mainland China.

It wasn’t the CK Group’s first brush with rejection. In 2016, Canberra blocked bids by State Grid Corp. of China and a CK unit for state-owned electricity company Ausgrid. However, a year later Australian regulators convinced investors all was well when it approved the group’s $5.5 billion purchase of energy network operator Duet Group.

That conclusion was premature. It’s become clear that the CK Group and Li have an image problem, one that mirrors that of Hong Kong itself. The former British colony is supposed to enjoy a high degree of autonomy under the One Country, Two Systems arrangement that saw China resume sovereignty of the territory in 1997. Incidents such as the denial of a visa to a Financial Times journalist and the detention of Hong Kong booksellers in the mainland have fed perceptions that this autonomy is being eroded by increased Chinese interference. The U.S.-China Economic and Security Review Commission last month recommended Congress reassess Hong Kong’s special trading status for some U.S. imports.

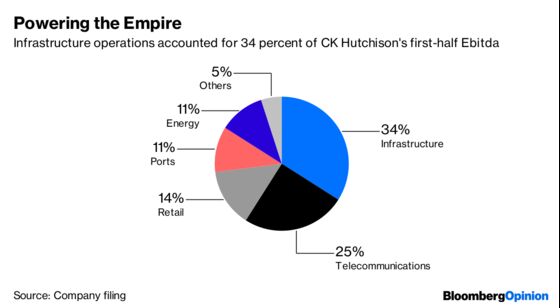

These days, CK Group’s business is largely the fruit of expansion into utilities, retail, telecom and infrastructure assets in Europe (especially the U.K.) and Australia, along with its stake in a Canadian oil firm. That means it can’t afford to be seen as too closely allied with China, where the group also has big investments. Based in a territory of only 7.4 million people, CK has little choice but to expand overseas. But transparency has never been a strong suit, and CK Group routinely acquires overseas assets using a mix of different units.

The issue isn’t insurmountable. Consider Taiwan’s Foxconn Technology Group, which managed to buy Japan’s Sharp Corp. despite employing thousands of workers in China and having to contend with resistance from Tokyo. Foxconn has also become a welcome investor in the U.S. state of Wisconsin.

Investors are growing impatient, though. Shares of group flagship CK Hutchison Holdings Ltd. slumped 19 percent this year through Dec. 18, more than the 14 percent drop in Hong Kong’s benchmark Hang Seng Index. The company trades at a 27 percent discount to net asset value, up from 2 percent three years ago, according to HSBC Holdings Plc. A payout ratio that’s remained unchanged at 31 percent even as leverage declined has helped to dim the stock’s appeal.

Headwinds include Brexit (which threatens the group’s substantial U.K. investments), low oil prices and rising interest rates. CK Hutchison’s decision to buy full control of its Italian mobile-phone venture in July —Li’s third major deal in his first two months as chairman — is looking questionable after an exorbitant 5G auction and the entry of a fourth competitor.

The group still has a lock on much of Hong Kong’s economic life, from a duopoly in electricity supply to large chunks of the city’s real estate, retail business and ports. But competition from mainland Chinese companies is likely to increase as the clock ticks down to 2047, when One Country, Two Systems is scheduled to expire.

Granted, CK isn’t likely to go the way of GE. The elder Li steered away from the kind of leveraged bets or expensive deals that former GE CEO Jack Welch and his successor Jeffrey Immelt undertook. Moreover, the Li family controls the group — a contrast with GE, which didn’t have a majority shareholder and was under activist attack.

Li Ka-shing, nicknamed “Superman” by local media, navigated British colonial times, the Hong Kong handover and the globalization of a business that started as a factory making plastic flowers more than half a century ago. Approaching the start of his first full year in charge, Victor has the task of maintaining growth and discipline in a vastly different world. It will test his management and communication skills to the full.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2018 Bloomberg L.P.