Wall Street Invaders Won’t Clear This Moat

(Bloomberg Opinion) -- Supply-chain finance is the secret sauce behind Citigroup Inc.’s mid-20% return on equity from transaction banking.

That might sound counterintuitive, especially in Asia. The export-led region is facing the brunt of supply dislocations as the U.S.-China trade war intensifies. But the skirmish isn’t a showstopper for financing. As production moves from one country to another, transactions that need to be greased with money or credit will occur somewhere else. They won’t disappear.

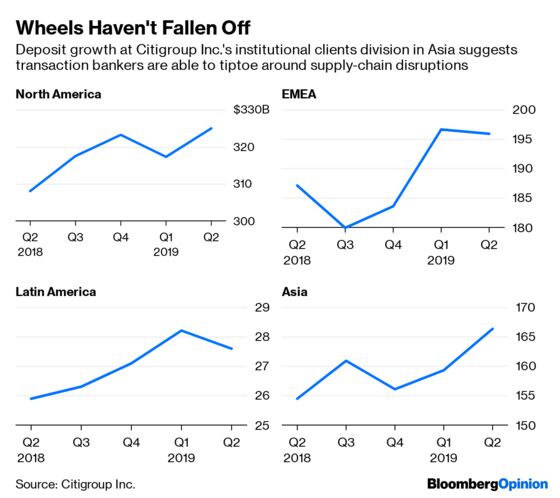

For evidence, take a peek at Citi’s recent quarterly results. The bank has $715 billion in deposits from institutional clients. About $166 billion of it is in Asia, up 8% from a year earlier and growing faster than consumer banking deposits.

What’s more, Citi doesn’t even have to aggressively seek corporate liquidity by promising high interest rates. It just has to work with a few hundred clients – not just Western multinationals like Procter & Gamble Co., but also Asian ones such as Alibaba Group Holding Ltd. and Xiaomi Corp. – by lubricating their vast global supply chains running into tens of thousands of vendors.

Imagine a detergent maker in Indonesia that gets paid by P&G 90 days after billing. The company would be tempted to accept money from Citigroup even for 120 days if doing so helps to keep its domestic bank-financing lines unencumbered. Citi doesn’t take any credit risk on this small supplier because the bank is going to be paid by P&G, which also benefits by getting an extra 30 days to settle its bills. A big chunk of the corporate cash swirling on Citi’s balance sheet is what the multinationals have in their accounts at the bank , vast sums that ensure supply chains function smoothly.

In a two-part series about virtual banking – the hottest new thing in Asian finance this year – my colleague Nisha Gopalan and I concluded that corporate cash management may be a more lucrative bastion than retail for the digital warriors to storm. That’s particularly so for Wall Street banks looking beyond fickle investment-banking revenue. However, even that “more modest leap of faith,” as we described the lure of transaction banking to the likes of Goldman Sachs Group Inc., will have trouble clearing Citi’s moat. It may not be impossible for an online-only bank to operate in more than 160 countries, deal with heavy penalties in case it flouts sanctions or gets dragged into a money-laundering scandal, and over time build its own war chest of deposits. But it’s certainly going to be difficult.

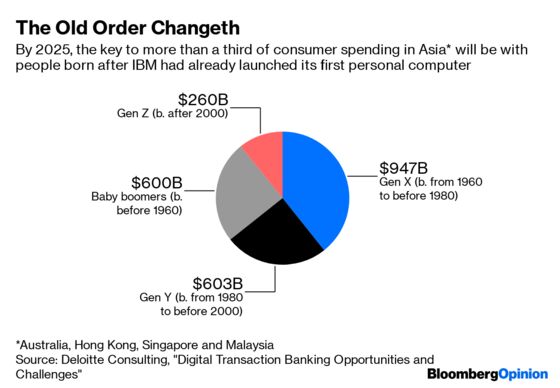

None of this means that traditional transaction bankers can rest easy. In the world they’re familiar with, materials move one way; money in the opposite direction. The greater the risk of interruption to the flows, the higher the premium for ensuring they don’t. This age-old landscape is changing fast. The consumption of a Netflix movie or a Spotify song is purely digital. Deloitte estimates that by 2025, more than a third of all consumption in Australia, Hong Kong, Singapore and Malaysia will be done by people born after 1980. The spending of digital native generations – Y and Z – will be light on materials.

Transaction bankers can’t dig themselves into a hole and pretend they’re engaged in a pure business-to-business activity. If you want to bank Uber Technologies Inc., you have to grapple with the financing of the discount coupons on late Uber Eats deliveries.

Many things in the new digital supply chain will be done more efficiently by non-banks. Deloitte cites the example of Traxpay, chosen this year by Edeka Group, a large German food retailer, to handle the working capital needs of its vendors. Platforms like Traxpay will still need banks. But the real profit lies in owning the client relationships, not in providing money. To retain their edge banks will either have to buy promising fintech firms, or build their own rival products. Both options are capital-intensive; neither is guaranteed to succeed.

We’ve previously characterized transaction banking as humdrum to distinguish it from its flashier cousin of retail digital banking. But not only is supply-chain finance juicy for banks, its meat-and-potatoes wholesomeness is drawing in fintech and Wall Street investment banks. The $715 billion of cheap liquidity sitting on the balance sheet of the big daddy of transaction banking is both a temptation for challengers, and a dare. It’ll be interesting to see where those deposits are five years from now.

--With assistance from Nisha Gopalan

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.