Why China's Stock Market Is Scarier Than 2015

The number of listed companies with little or no analyst coverage has grown. That’s a big risk for passive investors.

(Bloomberg Opinion) -- Around the world, more investors are starting to bet that dumb money can outfox smart money.

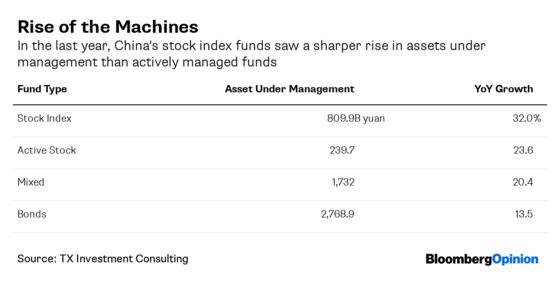

In the U.S., the world’s largest stock market, passive funds now manage just as big a pile of assets as active ones. China is following suit. As of June 30, assets managed by stock index funds rose 32% from a year earlier, outpacing growth in active funds.

As China’s day traders move their savings into ETFs, however, they need to beware of land mines. By one key measure, the stock market looks a lot riskier than it did during the roller coaster ride of 2015.

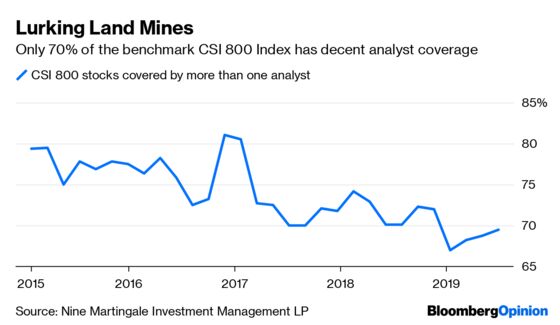

I’m talking about analyst coverage, an important transmission mechanism for information that ensures stocks don’t deviate too much from their fundamental value. Of the benchmark CSI 800 Index – which tracks Shanghai and Shenzhen’s largest listed companies – a whopping 20% has no sell-side analyst coverage; and another 10% is followed by only one analyst, data compiled by Nine Martingale Investment Management LP show. By comparison, roughly 80% of CSI 800 stocks were followed by more than one analyst in January 2015.

The picture is only slightly prettier when we move up the market-cap chain. Of the blue-chip CSI 300 Index, 12% is tracked by one analyst or fewer, up from 8% in 2015. Mind you: China has no shortage of brokers. The Securities Association of China, a trade union, boasts more than 100 members.

This is in stark contrast to the U.S., where stocks in benchmark indexes are closely followed by Wall Street. Only 16 stocks in the Russell 1000 Index are tracked by one analyst or fewer, and the S&P 500 Index has only two such black sheep, data compiled by Bloomberg show.

You don’t have to reach too far back for evidence of the damage this can cause. Before its abrupt trading halt in May 2015, Hong Kong-listed Hanergy Thin Film Power Group Ltd., was the largest member of the popular Guggenheim Solar ETF, with a 12% weighting. Yet the Chinese company had no analyst coverage – and trading volume was as thin as the solar panels it claimed to make. With its chairman Li Hejun holding an almost 75% stake, Hanergy's stock was vulnerable to price manipulation. After the halt, Guggenheim's ETF slumped 7.8% in one day, as U.S. investors rushed to pull their money out.

It’s worth asking why Chinese brokers have scaled back their research. One explanation is dwindling trading volume. In Shanghai, turnover is roughly one-third of its peak in 2015, as officials worked to stamp out margin financing and sentiment drooped.

Browsing through a list of stocks that lost coverage, brokerages such as Shanxi Securities Co., Western Securities Co. and Sealand Securities Co. jump out. Back in 2015, day traders used this sector to play the broader market. Now, with little trading – and tiny commission fees – bigger brokers aren't even bothering to assign ratings to their smaller peers.

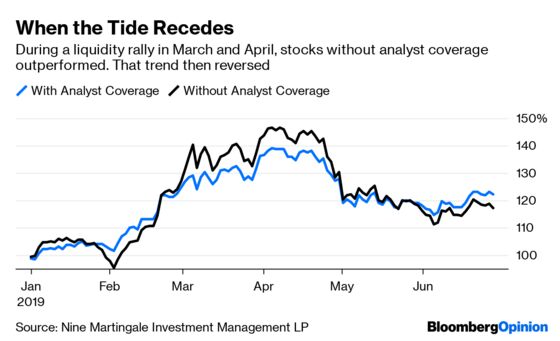

Some smart money has already discovered this pitfall. A portfolio constructed at the beginning of the year including only CSI 800 stocks with analyst coverage would have outperformed one with uncovered stocks by 5 percentage points. In other words, China’s mom-and-pops may still be better off going with active fund managers.

I’ve argued previously that China is the only major market left in the world where traders can make real money. The dearth of analyst coverage is another reason why, and could mean that Chinese stocks aren’t fit for passive investors just yet. Another Hanergy may be lurking.

By public float.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.