China’s Weaponization of Rare Earths Is Bound to Backfire

There was a time when China could cause the world to tremble by threatening its supply of rare earths. It’s long in the past.

(Bloomberg Opinion) -- There was a time when China could cause the world to tremble by threatening its supply of rare earths. It’s long in the past.

That’s reason not to worry too much about news that Beijing is planning to ban exports of technology for refining the suite of minor metals. Such a move, if taken, is likely to backfire even more spectacularly than its previous attempts to weaponize the trade in rare earths itself.

In 2010, a dispute between China and Japan over which country owns a group of islands off the northeast coast of Taiwan caused Beijing to impose export restrictions on all 17 rare earths. That was a problem for Japan, which depends on elements like neodymium, dysprosium and terbium as essential components of equipment such as motors, LEDs, lasers and fuel cells. At the time, China had a near monopoly of the world’s production of the metals. Without alternative sources of supply, Japan’s hi-tech industry would be crippled.

There was a simple lesson from that crisis: Given China’s willingness to use rare earths as a geopolitical weapon, diversifying would be an absolute necessity.

Japan Oil, Gas and Metals National Corp. or Jogmec, a state-owned enterprise set up to guarantee the country’s access to essential materials, funded Australian producer Lynas Rare Earths Ltd. at well below market rates to encourage a non-Chinese supply chain, as we’ve written.

Thanks to that investment, Lynas now produces nearly 20,000 metric tons a year of rare earth oxides from its Mount Weld mine in Australia and processing plant in Malaysia, more than enough to meet all of America’s demand let alone the 500 tons or so needed for defense-critical applications. Last month it signed a contract to build a new facility processing 5,000 tons a year of rare earths in Texas, jointly funded with the U.S. Department of Defense. The Pentagon also last year helped fund a series of other projects to guarantee more processing in the U.S., including from the large Mountain Pass mine in the Mojave Desert where listed MP Materials Corp. operates.

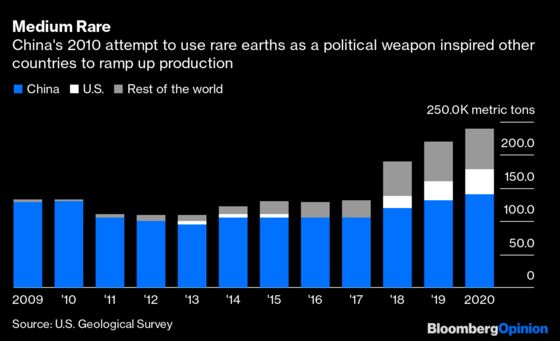

The result of all this has been dramatic. From 98% of global mined production in 2010, China’s market share had fallen to 58% by 2020. Mount Weld and Mountain Pass alone now account for nearly a quarter of global rare earths supply.

Meanwhile, the Pentagon also set up a government stockpile of rare-earth elements analogous to the U.S. Strategic Petroleum Reserve, and announced plans to buy about 5,000 tons last year. Separately, major importers brought and won a case against China at the World Trade Organization over rare earths, as well as tungsten and molybdenum, two other elements where it had an outsize share of supply.

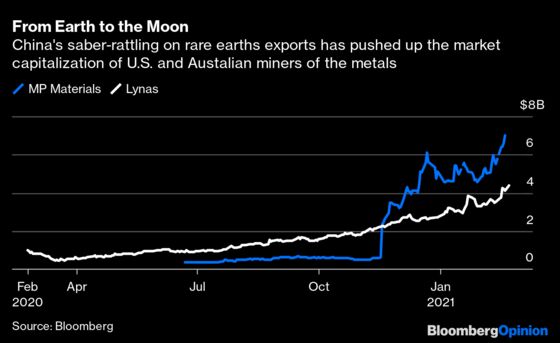

Occasional saber-rattling over the past year has already driven up the valuations of non-Chinese producers, making it even easier for them to fund expansions of mining and processing capacity. Lynas last August raised A$425 million ($335 million) selling new shares to pay for a processing facility in Australia and upgrades at its Malaysian plant. The market capitalization of MP has surged more than tenfold since it went public via a SPAC deal last July.

Nothing about this turn of events should surprise anyone.

When Arab countries used their dominance of oil exports to push up the price of crude in the 1970s, the outcome was not a permanent Gulf stranglehold on energy but a rush to diversify. Rich countries retired their oil-fired power stations and built coal and nuclear generators instead, while new wells were tapped in the North Sea, Siberia, Mexico and Texas.

When Richard Nixon imposed an export embargo on soybeans shortly before the 1973 Arab oil embargo to help rein in galloping domestic inflation in the U.S., there was a similar outcome. Japan, which depended on America for about 92% of its soybean supply, helped establish a Brazilian industry to diversify its import base. It’s now the bigger global producer of such oilseeds.

The world depends on sprawling supply chains of scarce materials for a range of essential products, from electric vehicle batteries to fertilizer and MRI scanners. Most of the time, we pay little attention to the interdependency that’s built into these trade networks, because no player is reckless enough to damage its own position in the market by using it as geopolitical leverage.

As China itself is striving to demonstrate in the far more technically complex market for semiconductors, though, political restrictions on exports will only cause major importers to reconfigure their supply chains to be more resilient. Beijing’s control of rare earths is as much of a paper tiger as it ever was.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2021 Bloomberg L.P.