China’s Trade Weapons of Mass Destruction Are Missing

(Bloomberg Opinion) -- In the feverish run-up to conflict, it’s only natural the protagonists should be on the hunt for ways to justify their rash actions.

In the months preceding the 2003 Iraq war, that came in the form of the confected claims that Iraq had stockpiled weapons of mass destruction and trained al-Qaeda operatives in how to use them.

With a fresh set of tariff barriers this week set to ramp up tensions between China and the U.S., it’s now coming in a different form: A narrative that compromise with Beijing on trade is impossible because it treats foreign investors and powers as vassals to be subdued.

Through loans from state banks, acquisitions of foreign companies, and technology-transfer agreements with foreign investors, the Chinese government threatens “the long-term competitiveness of U.S. industry,” according to a March report from Trade Representative Robert Lighthizer. In the blunter words of President Donald Trump, “we can’t continue to allow China to rape our country.”

It’s striking, in the face of all this adrenalin, to consider the more humdrum facts of doing business in China. After all, the preference of companies in recent years has been to embrace, not shun the opportunity to invest there.

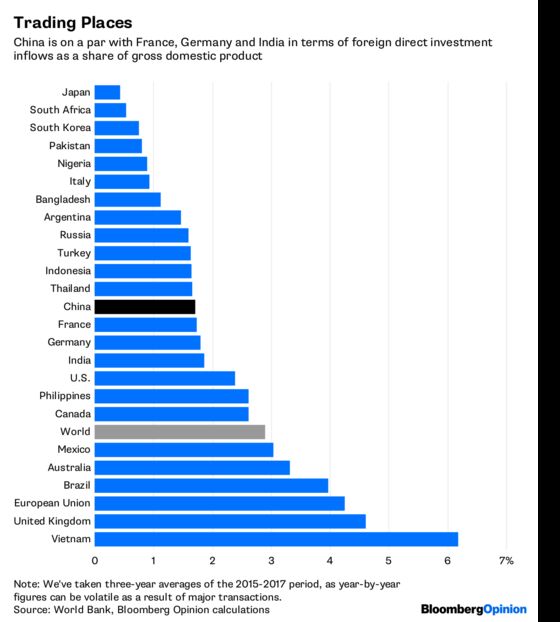

After the U.S., U.K. and Hong Kong, China is the biggest single recipient of overseas capital globally, with a $1.49 trillion stock of foreign direct investments that’s roughly equivalent to the amount put into Africa and the Middle East combined.

That doesn’t appear to be reversing under China’s current authoritarian turn: The $136 billion inflow during 2017 was the largest on record and represented about 9.5 percent of FDI movements during the year, the data show. As a share of gross domestic product, average inflows over the past three years have been fairly typical for a major economy, and over the past five years they’ve been better than the U.S.

Of course, it’s possible the allure of the Chinese market is so great that businesses will shun a bad and worsening investment climate, calculating the offsetting benefits are worth it. There’s probably a degree of truth to that, but also major reasons to question it.

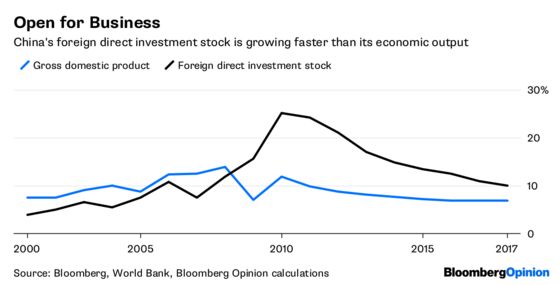

For one, China’s stock of inward investments is still growing at a healthy pace, despite an anticipated slowing in the economy and a more robust growth trend in India, Vietnam, the Philippines, Bangladesh and Ethiopia.

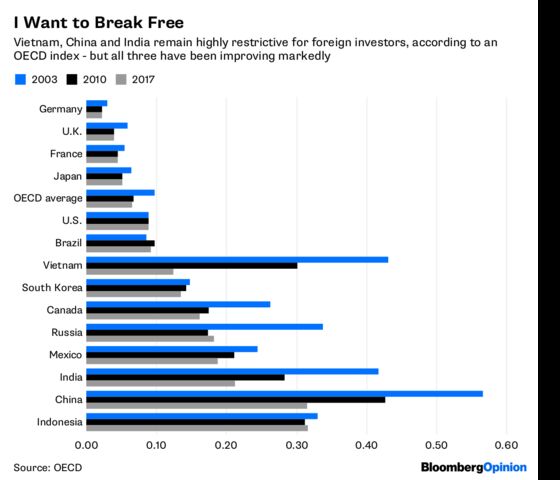

For another, measures of trade restrictiveness – such as the OECD’s gauge and the U.S. Chamber of Commerce’s IP index – have improved notably in recent years, despite remaining elevated relative to developed economies.

A more ground-level picture of operating in China can be gleaned from looking at the business-climate reports put out by the foreign chambers of commerce there.

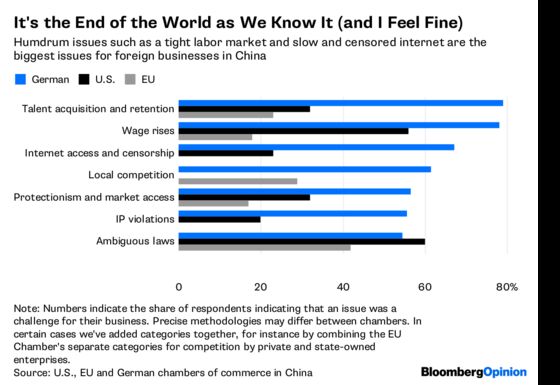

Many of the issues cited by Washington’s trade restrictionists come up – in particular the presence of ambiguous or inconsistently enforced regulations, licensing difficulties and being banned from particular parts of the market. Other issues, though, are almost absent (such as financial support from state banks) or don’t rank very highly, such as threats to intellectual property.

In contrast, many of the biggest worries are the sorts of regular difficulties you’d see in any overseas market. The challenges of finding and retaining staff and the pace of wage increases, plus slow and censored internet access form the top five worries for German businesses, while a slowing domestic and global economy are the No. 1 and No. 3 concerns in the European chamber’s report.

In the U.S. chamber’s report, compliance issues, labor costs and scarcity of talent comprise three of the top five risks, between ambiguous regulations at No. 1 and protectionism at No. 5. In all three reports, the challenges of complying with new regulations and environmental rules – issues one rarely hears about – are quite as prominent as more politically charged topics.

Even the Made in China 2025 plan to upgrade the nation’s high-tech capacity – one of the central planks of Washington’s case for the prosecution – attracted remarkably few concerns.

Only about 16 percent of companies polled by the European chamber said they were seeing increased discrimination as a result of the program. A similar 18 percent in the German chamber’s survey felt it would be negative for their local operations over a 10-year time frame, but 51 percent said it would be positive. In an indication of how little the issue was on the minds of U.S. businesses until Lighthizer started banging the drum about it, the U.S. chamber didn’t even bother to ask its members a question about the policy when it conducted its latest survey last autumn.

As we’ve argued before, there are real issues with how China does business on the world stage, from the shell-game over the industries it protects from foreign investment, to still-rampant intellectual property theft and Made in China 2025’s quota targets for domestic production.

Still, those ought to be irritants to be worked out in the context of the chess game between the two sides. They’re not grounds to sweep the pieces from the board and let slip the dogs of trade war.

To contact the editor responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net

©2018 Bloomberg L.P.