(Bloomberg Opinion) -- Prepare for a crackdown on China’s overheated rental market.

President Xi Jinping’s push to develop housing for lease was supposed to take the edge off soaring home prices. It hasn’t worked out that way. Rents instead have rocketed as the government’s call triggered a stampede of investment into the sector, fueling discontent among a millennial population that had already been priced out of the market for home purchases.

Chengdu led the surge with a 31 percent jump in average rents in the year through July, followed by a 30 percent increase for the southern boom town of Shenzhen, according to data from the China Real Estate Association. Beijing registered a 22 percent gain, while rents in Shanghai climbed more than 16 percent.

Developers such as China Vanke Co. and Longfor Group Holdings Ltd. were quick to heed the message after Xi said in October last year that houses were built to be lived in, not for speculation, and pledged to make renting as important as purchasing. City governments made more land available for rental projects and state-owned banks were encouraged to lend for such developments.

China’s rental sector is undeniably underdeveloped. Only one-fifth of the housing stock in Beijing, Shanghai and Shenzhen is used for leasing, versus 50 percent in Tokyo and more than 60 percent in San Francisco and New York, according to Bloomberg Intelligence and Beijing Homelink Real Estate Brokerage Co., also known as Lianjia.

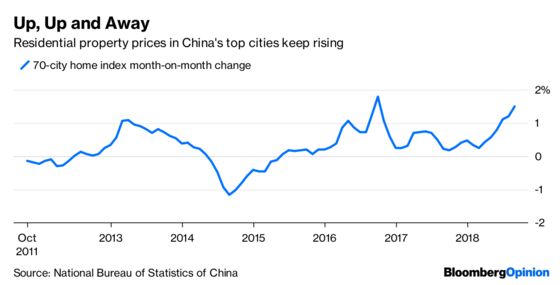

The trouble is that ultra-low yields – the corollary of high sale prices – make it hard for property companies to earn an economic return on their investment, putting upward pressure on rents. Yields in major Chinese cities are just 1 percent to 2 percent, according to Robert Ciemniak, CEO of Hong Kong-based research and analytics firm Real Estate Foresight Ltd.

Developers prefer building homes for sale because they get an instant cash return from pre-sales. That’s why Vanke, for instance, has resorted to freezing rents for tenants who pay 10 years upfront for its Emerald College development on the outskirts of Beijing. Yet it would still take the developer more than 35 years to recover its investment through rentals, even as analysts questioned whether the 1.8 million yuan ($261,000) entry-level payment was too high, the South China Morning Post reported.

Much of the rental inflation has been driven by a new group of real estate brokers that have bid heavily against each other to source apartments from landlords, renovate them and then let them out at higher prices, a model that Ciemniak calls “rent in order to sub-rent.” Apartments that cater largely to urban millennials who can’t afford to buy sometimes go for double what these asset-light companies pay the owner.

Among the big players are Ziroom, owned by Lianjia Chairman Zuo Hui, which raised 4 billion yuan in January from private-equity firms Warburg Pincus and Sequoia Capital, as well as Tencent Holdings Ltd. among others. Singapore’s sovereign wealth fund GIC Pte and the Canada Pension Plan Investment Board have also entered China’s rental market. Besides private-equity money, real estate brokers have been allowed to securitize future rental streams, giving them further fuel for expansion.

Until now, authorities have sought to keep the party going. For example, state-owned China Construction Bank Corp. has gone as far as giving housing rental loans to tenants in cities such as Shenzhen where prices have jumped. There are signs that may change.

Beijing has interviewed the owners of leasing companies such as Ziroom and Danke Gongyu and stopped them from using bank loans to accumulate housing stock. The Commission of Housing and Urban-Rural Development, meanwhile, has called on brokers to refrain from raising rents and overbidding in their drive to expand.

These early signs of official misgivings could presage more forceful measures, such as improving tenants’ rights, more quality inspections, restricting loans for renters and controls on securitization. Ultimately, the government could turn to price caps if the rental boom continues to build.

Some rules are inevitable for the nascent sector after reports of abusive practices such as brokers using tenants’ names to take out loans, debt-fueled expansion leading to bankruptcy, and abnormal formaldehyde levels in renovated apartments.

To be sure, rent increases may be less extreme than the headline figures suggest. The quality of renovated apartments improves on returning to the market. Higher rental prices reflect that, while brokers may also throw in free furniture or cash rebates.

The danger of seeking to restrain prices is that it will weaken the incentive of companies to develop rental housing, impeding supply and undermining the government’s long-term objective of developing a thriving market. This reflects the contradiction of pushing developers to build homes for lease when the investment case doesn’t justify it.

One solution would be a slump in sale prices that pushes up yields and makes the rental market a more attractive proposition. No one in Beijing is likely to be suggesting that.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2018 Bloomberg L.P.