China’s Price Controls Won’t Crash a Booming Metals Market

So long as activity in the real economy continues at the current pace, such tactics are unlikely to succeed.

(Bloomberg Opinion) -- China’s government is on a campaign to rein in prices for industrial metals. If it wants the plan to work, it needs to address the cause, not the symptoms.

State-owned companies have been ordered to control their risks and limit exposure to overseas commodities markets, people with knowledge of the matter told Bloomberg News this week. Government stockpiles of copper, aluminum and zinc will also soon be released to fabricators and manufacturers, a measure that could be expected to reduce prices.

It’s unlikely to play out that way. Like any investor caught on the wrong side of a trade, the Chinese government would like to think prices are being driven by nefarious speculators disconnected from reality. In truth, they’re moving because of activity in the real economy that won’t stop just because an official is ordering the tide to turn.

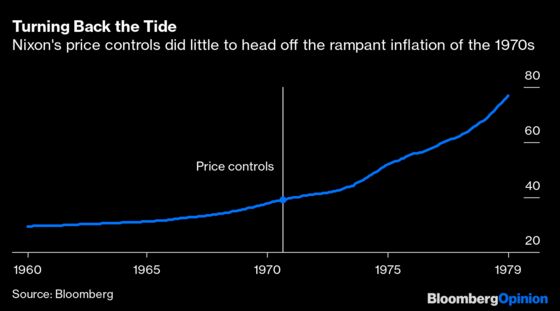

To see why, consider what happened in August 1971 when Richard Nixon imposed controls on wages and prices in an attempt to curb rising inflation in the U.S. See if you can spot that moment on a chart:

Another relic of the 1970s shows how hard it still is for the government to drive down prices. The U.S. Strategic Petroleum Reserve has been around since the oil crises of that decade to ensure that America never runs short of crude — but on the occasions the SPR has actually been deployed, there’s little evidence it’s had much effect.

The most recent of the three emergency drawdowns happened in 2011 as the Arab Spring was rolling through the Middle East. The impact seems to have been, if anything, counterproductive. One month after Barack Obama first mooted tapping the SPR in March of that year, prices for WTI crude were 8.7% higher, at $109.92. After easing down toward $91 over the following months, Energy Secretary Steven Chu’s announcement in June of a 60 million barrel coordinated international release of supplies was followed by another 9% monthly jump. It’s at this point almost a boring observation among economists that the SPR has little effect on crude prices, and may even be pushing them higher.

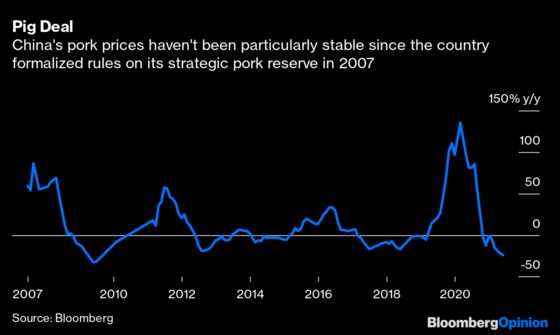

There’s evidence closer to home to show Beijing price controls don’t work. China’s pork reserve — a warehouse network of frozen meat that the government has used since 2009 to mitigate swings in the supply and demand for hogs — has increased rather than decreased price volatility, according to a study led by Yi Yu of Nanjing Agricultural University. That’s probably because such heavy-handed government intervention dulls the signals that producers need to judge where things are headed. China’s pigmeat market, which in little more than 12 months has gone from record inflation to the strongest deflation in a decade, doesn’t look like a model of stability.

To be sure, the scale of China’s planned metal sales might be enough to scare some speculative froth out of the market. Releases from the U.S. SPR have tended to be relatively small, on the order of one or two days’ worth of U.S. oil demand. Figures in the region of 800,000 metric tons of aluminum that have been quoted in relation to China’s plans are far more significant, in the range of a week’s worth of output. The size of Beijing’s strategic metal stockpiles is a closely guarded secret, so anyone buying on the hope of rising prices is facing a seller who may well have an unfathomably large warehouse of metal to keep levels suppressed.

The risk is that — as with pork — it’s the open market manipulation by the government that causes prices to gyrate, rather than the supposed market manipulation by private investors that the reserve sales are meant to stop.

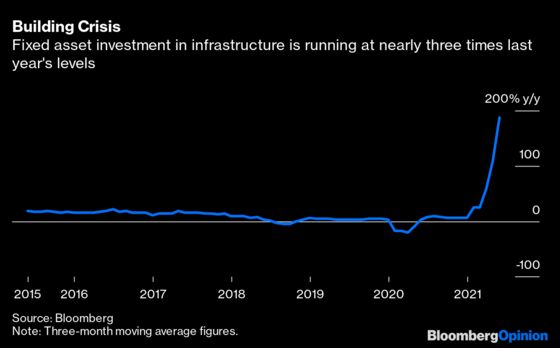

There’s plenty to suggest that metals demand in China is fundamentally strong. Fixed asset investment in infrastructure was running at nearly three times the levels of a year earlier over the three months through May, far in excess of anything the country has ever seen. The treatment charges that copper refiners demand for turning metal concentrates into metal hit a record low of $30.54 a ton in April, suggesting they’re cutting their margins to get product to consumers. Producer prices rose 9% from a year earlier in May, their fastest pace since 2008.

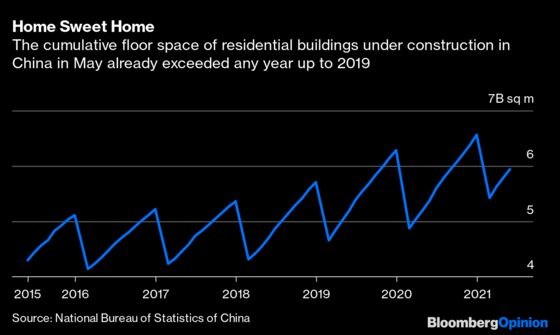

House prices are soaring, with the supply of apartments plummeting despite the fact that the floor space of residential buildings under construction in May this year was already running ahead of the annual total in any year up to 2018. Each of those buildings will need its supply of copper wiring, aluminum window frames and zinc-galvanized steel balconies and staircases — and usage of such fit-out products doesn’t tend to peak until late in the year.

Until tools are down on all those construction sites, government diktat won’t be enough to crash a red-hot metals market.

It’s a similar picture with the other two emergency drawdowns. A month on from the SPR release due to Hurricane Katrina in 2005, WTI was a mere $2.10 per barrel lower, or 3.1%. While the monthly price move after President George HW Bush tapped the SPR at the start of the 1991 Gulf War was a more dramatic 30% slump, that only took it to the levels crude had been trading at before Iraq invaded Kuwait. War and peace, rather than microeconomic tinkering, were the drivers of the price decline.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2021 Bloomberg L.P.