Wild Oil Markets Leave Shanghai a Little Dizzy

The Shanghai contract has done modestly well to date, especially relative to past attempts to create rival oil benchmarks

(Bloomberg Opinion) -- A pandemic, a supply glut and plunging U.S. crude futures: With the world upended, there’s never been a better time to challenge established oil benchmarks. So shouldn’t China’s two-year-old yuan-denominated contract be doing just that?

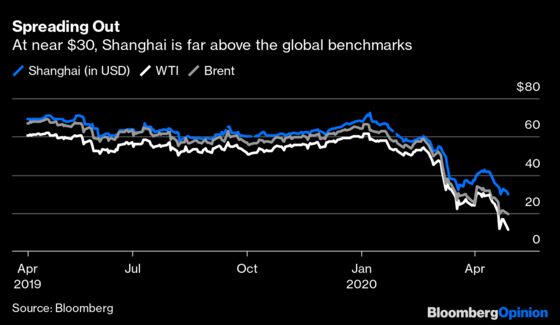

The upheaval in oil is hard to overstate. Last week’s extreme dive into negative prices, driven by the quirks of physical delivery, dealt a significant blow to the credibility of West Texas Intermediate futures. That contract has long been a benchmark for the U.S. oil industry, albeit a flawed one. Heavy selling from the biggest oil exchange-traded fund exacerbated the slide, which could see a repeat in May, when June futures expire. WTI is trading near a meager $16 a barrel, with Europe’s Brent, a better indicator of seaborne oil demand, at under $23. Both are at a fraction of January levels well above $60.

By contrast, Shanghai crude futures are trading at a lofty near-222 yuan a barrel, or just over $31. The contract was set up in 2018 to reflect the shift in the market’s center of gravity to Asian demand and the Middle Eastern grades that China consumes. That’s a near-record spread to the global benchmarks.

The pricing gap is an odd distortion. Part of the premium is due to soaring freight costs to China, which have spiked to as much as 60% of Brent. With few available ships in producing regions, plus the number being used for floating storage, the price of shipping to China is going up. Charterers want to avoid long journeys. But there’s more: traders say storage capacity constraints have made it hard to deliver oil, even with bids. Local retail investors, meanwhile, have piled in. None of this is helping a contract that aims to unseat the current dollar-denominated duopoly.

The Shanghai contract has done modestly well to date, especially relative to past attempts to create rival benchmarks, say, in Russia. It has been liquid, too, thanks to retail interest and local, if not international, trading heavyweights. Investors have started to hedge and there has been none of the Beijing meddling that damaged market credibility in the past.

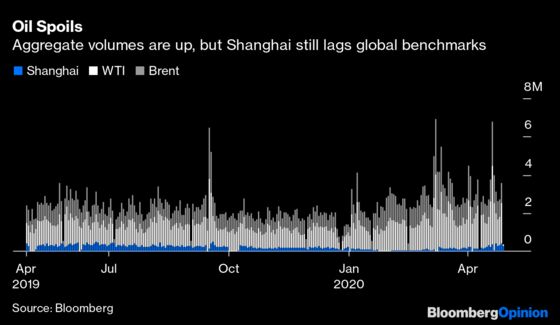

Yet Shanghai has on average amounted to only about 10% of global oil futures volumes over the past 12 months, and a smaller slice as a proportion of open interest. U.S. sanctions against countries such as Russia and Iran haven’t yet helped fuel significant moves into yuan either. While the pandemic has seen interest from Chinese investors soar, the upheaval doesn’t appear to have shifted international trade.

In part, that’s because some problems with the contract were still being solved when the crisis hit, like concentration of activity at the front end of the curve. Then there’s the fact that the contract is denominated in China’s currency, which isn’t fully convertible. That’s key for Beijing’s policy ambitions but a headache for traders.

Regardless, the price gap isn’t encouraging. A benchmark, after all, should reflect global markets. On a positive note, the Shanghai International Energy Exchange has been moving to add warehouse capacity, approving an additional 800,000 cubic meters of storage Friday. The INE is now also considering allowing deliveries to tanks and ships held by refiners or traders, Reuters reports. That will begin to ease the speculative squeeze and should narrow the premium.

One mainland trader described INE’s efforts on storage as swan-like — paddling fast underwater, despite the calm exterior. With more futures contracts becoming available to foreign investors, Beijing will hope so.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Clara Ferreira Marques is a Bloomberg Opinion columnist covering commodities and environmental, social and governance issues. Previously, she was an associate editor for Reuters Breakingviews, and editor and correspondent for Reuters in Singapore, India, the U.K., Italy and Russia.

©2020 Bloomberg L.P.