Fishing for Alpha? Take Your Investing Net to China

(Bloomberg Opinion) -- Ever seen Chinese silver carp jumping out of the water? Some can leap three meters into the air.

That’s what a vibrant stock market should look like, and it’s an image that helps to explain why foreign investors are warming to China.

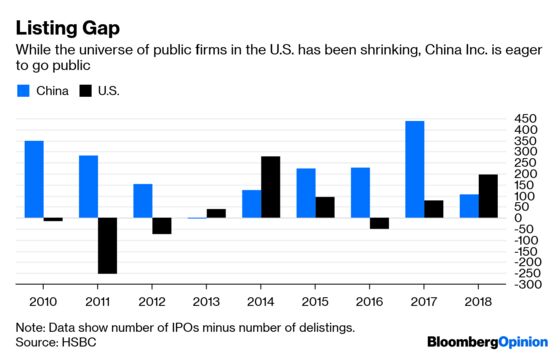

The U.S. market’s record bull run masks the inconvenient truth that the universe of public companies has been shrinking since the late 1990s. A market with few IPOs is like a stagnant pool of dead fish. China, by contrast, is teeming with opportunities to hook the next high-flyer before it soars.

Overseas investors bought more than 120 billion yuan ($18 billion) net of China-traded shares this year through Hong Kong’s Stock Connect program. The U.S.-listed Xtrackers Harvest CSI 300 China A-shares ETF has seen record daily inflows this week.

To some extent, this should be no surprise. In just two months, China’s stock market has done a 180, morphing from one of the world’s worst performers into the best. Speculative traders go where the action is hot.

But even if China’s rally runs out of steam, foreigners will still want to pile in. As the supply of equities shrinks, developed nations from the U.S. to Japan are turning stale. If you’re looking for opportunities, you’ve got to go into emerging markets.

The dearth of U.S. listings can be blamed on regulation, mergers and acquisitions — and even SoftBank Group Corp.’s Masayoshi Son, whose $100 billion Vision Fund is pushing unicorns to delay IPOs.

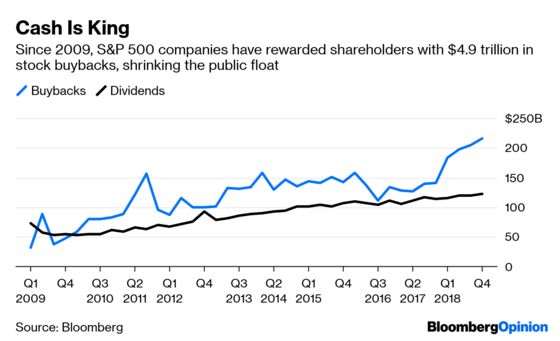

To make matters worse, one trick U.S. firms have been using to propel their share prices higher is buybacks, which shrink the available pile of public stock.

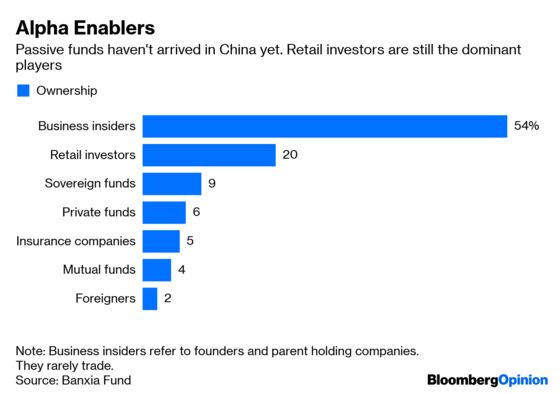

Welcome to China, then, where startups are eager to go public and humans rather than machines are still the dominant investors.

Granted, the IPO market is far from a free-for-all. The nation still operates an approval-based system that requires companies to go through a lengthy and stringent application process. Last year, just 56 percent of IPOs got the nod, far below the average of 82 percent in the past decade. Sometimes, applications are rejected simply because regulators are overburdened and exhausted.

But Beijing knows the pitfalls and is willing to change. In the second half of this year, the securities regulator will open a new technology board in Shanghai that will adopt a faster, registration-based system for listings. Foreigners may be allowed to buy these shares via Hong Kong Exchanges & Clearing Ltd.

Take a look at the kind of stocks overseas investors favor. They aren’t going for the boring index heavyweights like banks and insurers, but specialized and crucial industrial parts manufacturers. They love Han’s Laser Technology Industry Group Co., which makes laser-based welding and engraving machinery; Zhejiang Sanhua Intelligent Controls Co., China’s biggest supplier of heating, ventilation and air-conditioning components; and AI-based surveillance camera maker Hangzhou Hikvision Digital Technology Co. Investors are thirsty for young firms that offer new ideas and technology.

Thanks to the dominance of retail investors, the mainland’s A shares remain a haven for stock-pickers. As of 2017, individual investors held 21 percent of the total market value and accounted for 82 percent of total trading, but earned only 9 percent of profits, according to the Shanghai Stock Exchange. In other words, savvy institutional investors can still generate alpha.

Not to mention that the mainland Chinese market is among the world’s most liquid. Turnover in Shanghai and Shenzhen puts Hong Kong to shame.

To be sure, the A-share market has plenty of dangers. Four years ago, shadow margin trading precipitated a meteoric rise and equally spectacular crash. But these risks were known, and well-reported.

As always, investors need to pay attention and do their own due diligence. For those who fancy their fishing skills, plenty of prize catches await.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.