Don’t Underestimate China’s Low-Inflation Headache

Price gauges are retreating, as they are in many economies. It’s a challenge with global dimensions.

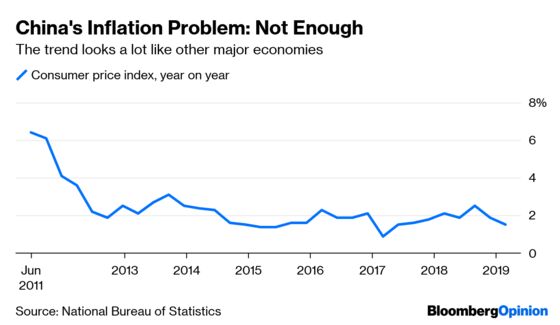

(Bloomberg Opinion) -- China has an inflation problem. It's too low and likely to get lower still.

The slowing pace of consumer price increases isn't sexy like a bad purchasing managers’ number, a collapse in car sales or a stock-market swoon. Lowflation tends to happen slowly. That doesn't make it less of a concern. Once it gets hold of an economy, it can be devilishly tricky to shake. Witness how low interest rates are in major economies, given the length of the expansion and the rock-bottom levels of unemployment.

Figures released over the weekend show how alive the problem is in the Middle Kingdom: CPI rose 1.5 percent in February from a year earlier, down from 1.7 percent a month earlier and considerably below the 2.5 percent clocked in September and October. The increase was 2.9 percent in February 2018. Producer prices barely climbed at all.

In some respects, this trend mirrors what's going on in many economies, big and small, Asian and Western, emerging and developed. Not only is inflation below target, it's heading south.

Unlike most major economies, China doesn't have an independent central bank charged with pursuing a numerical goal for price increases; in many countries it's about 2 percent. As a point of reference, let's just note that China's CPI has spent as much time below 2 percent in the past five years as it has at or above that mark. The average since 2014 has been 1.8 percent.

Inflation normally does weaken when economic activity is softening, and there is plenty of soft news around in China. But it's retreating from a point that was fairly low to begin with.

Not just in China. On Friday, Federal Reserve Chairman Jerome Powell signaled inflation is the bar that has to be met for the Fed to resume increasing rates. The labor market can pump out as many jobs as it wishes. If inflation doesn't do what it's supposed to, the Fed is done nudging rates up. The case for a cut this year doesn't get enough attention.

How does lowflation manifest itself in China's neighborhood? You have to look hard for any sign inflation is on the march in the so-called Tiger economies of Southeast Asia. Malaysia just had a bout with falling prices; in Indonesia, CPI is in danger of disappearing below the lower range of the target. In the Philippines, new central bank governor Benjamin Diokno walks into office with inflation returning to the bank's 2 percent to 4 percent preferred range. That's a gift horse he's unlikely to look in the mouth.

This is a global challenge. Differences are of degree not kind, even when it comes to China. The country has been underestimated, though perhaps not in the way its leaders would prefer. Its economy does resemble others in important respects. Lowflation is one of them.

Tick another box for China's normalization.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.