How Giants Fall in China

Government favor can help private companies swell to gargantuan size quickly, but those debts will eventually have to be paid.

(Bloomberg Opinion) -- China likes to tout the virtues of its private sector, whose firms are the source of most new jobs and most economic growth in the country. Not all private companies are created equal, however. Those perceived to have the state’s backing can grow disturbingly fast and crash to earth just as quickly.

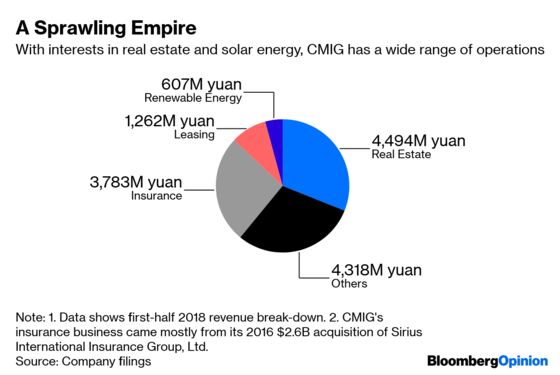

Behemoth China Minsheng Investment Group Corp. is only the latest example. The company was founded in May 2014 to act as a private-sector version of a sovereign wealth fund, one that would supposedly be better at investing than its state-run counterparts. Its founding investors included 59 different private companies, who pooled together some 40 billion yuan ($5.9 billion) in registered capital.

As of last September, the most recent financial data available, the group was carrying 232 billion yuan in debt, 63 percent of it due within a year. As with other fast-growing private conglomerates such as HNA Group Co. and energy trader CEFC China Energy Co., those obligations have started to unravel. CMIG has tested bondholders’ nerves repeatedly this year with late repayments, the latest of which spread offshore and triggered cross-default clauses on dollar bonds that had been worth $800 million.

CMIG’s stunning growth has inevitably created the impression that the firm has political backing. It openly describes itself as the brainchild of Premier Li Keqiang. In a 2016 bond prospectus, the group noted it was “the only private enterprise approved by the State Council to use ‘China’ in its name” and that it regarded “serving [China’s] national strategy as its mission.” The group pledged to spend $5 billion developing an industrial park in Indonesia as part of President Xi Jinping’s signature Belt and Road infrastructure-building program, and talked up investing in Vietnam and Cambodia.

Within two years of its founding, the company had won credit lines with policy banks such as China Development Bank and Export-Import Bank of China, the latter now mired in an asset-disposal dispute with the firm. CMIG enjoyed about $10 billion in loan facilities from the two policy banks and China’s big four commercial banks -- an unusually large amount for such a young private company.

There’s nothing inherently wrong with relatively easy credit. But it can breed overconfidence, leading firms to take on riskier long-term projects. When that tap closes all of a sudden, as it frequently can in China, companies such as CMIG can be stuck with illiquid projects desperate for cash injections.

For instance, shortly after its founding, CMIG spent 25 billion yuan, or roughly two-thirds of its capital raise, on a prime plot of land in Shanghai. This could have been its best investment -- Shanghai’s property price has soared since -- but the deal didn’t work out: CMIG had promised to develop the plot by 2020, which meant it required the kind of cash the now-distressed company no longer has. The property was sold under pressure to state-owned developer Greenland Holdings Group Co. Ltd. to honor a February bond repayment.

CMIG could face similar problems elsewhere in its portfolio. In late 2016, in a $2.6 billion deal, CMIG took control of Yida China Holdings Ltd., which specializes in property developments in lower-tier cities such as Dalian. China’s smaller cities have a notorious over-supply issue, and sure enough, sales at Yida have been stagnant in the last three years, while those of its larger competitors have rebounded.

And then there’s CMIG’s unfortunate venture into solar energy, which followed the meteoric rise of Hanergy Thin Film Power Group Ltd. In 2015, CMIG sought to build the world’s largest solar park. By last June, it had plowed over 10 billion yuan into solar projects, which are notorious for their long investment cycles. (CMIG’s biggest project, in Ningxia province, won’t break even for nearly a decade, even using the company’s own aggressive assumptions.)

Meanwhile, the policy tide is turning. Tired of hefty subsidy bills, Beijing now only welcomes solar parks to supply to its grids if they don’t require government aid.

While CMIG continues to tout the potential of Belt and Road investments, prospects are dwindling there, too, in part because of a backlash among recipient countries. Its construction work at Country Garden Holdings Co.’s $100 billion Forest City project in Malaysia has stalled ever since Prime Minister Mahathir Mohamad balked at foreigners buying property there. Its Indonesian industrial park has gone nowhere.

The Belt and Road label does have one key advantage: CMIG can be kept alive longer if it can show it owns strategic assets. Nearly a year since it first defaulted, energy trader CEFC has yet to be put into a bankruptcy process in China, Debtwire has reported, because Beijing wants the company to offload its minority stake in an Abu Dhabi oil concession -- a strategically important asset -- before its other assets fall into creditors’ hands.

CMIG hasn’t grown big enough to pose a systemic financial risk. Still, China should be wary of allowing such private-sector giants to swell largely on perceptions of political support. Sooner or later, those bills will come due.

To contact the editor responsible for this story: Nisid Hajari at nhajari@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.