The Chinese Car Market's Short Joy Ride Is Over

Temporary factors led to a recovery in June. Consumers now need to pick up the slack, which seems unlikely these days.

(Bloomberg Opinion) -- Is the season in hell for China’s car industry finally ending?

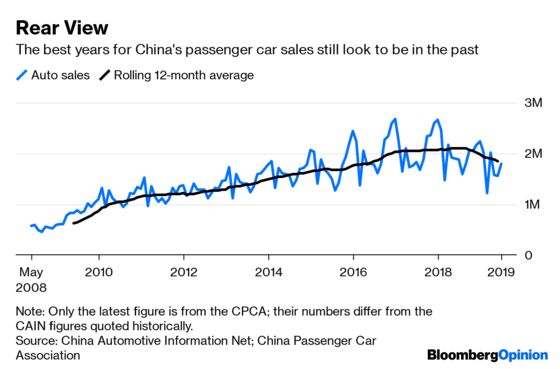

Passenger-car sales in June rose for the first time in a year, up 4.9% from a year earlier, the China Passenger Car Association said Monday. That’s quite a contrast from falling as much as 18% in April. Sales in the habitually quiet month of February were the lowest for any month since 2013.

Don’t get too comfortable, though. On a trailing 12-month basis, performance is still at its weakest since 2016. The recovery has been expected for some time, and may not last.

One explanation for the better numbers is simply that after 12 months of decline, the comparisons from a year earlier are much more flattering. A bigger factor, however, may be the new emissions standards that finally kicked in last week across a host of Chinese regions.

Dealers unwilling to get stuck with cars they couldn’t sell after the changeover have been running down their inventories for months, meaning there just haven’t been enough cars out there to meet the demand. Over the past month, things appear to have come to a head: Vehicles that met the new standards were arriving in showrooms just as discounting on non-compliant cars hit panic levels. Such price cuts helped push 39% of dealers into losses last year.

The pain isn’t over yet. To really get off the mat, China’s car industry needs to see a recovery in consumer demand, but pocketbooks are pressured at the moment. Retail-sales growth has been weakening, dipping to a record low 7.2% in April. With inflation hitting 2.7% in May, its highest level in nearly six years, there’s even less cash to spare. Food inflation is a particular stress, running at 7.7%, with the figure for pork up more than 18%.

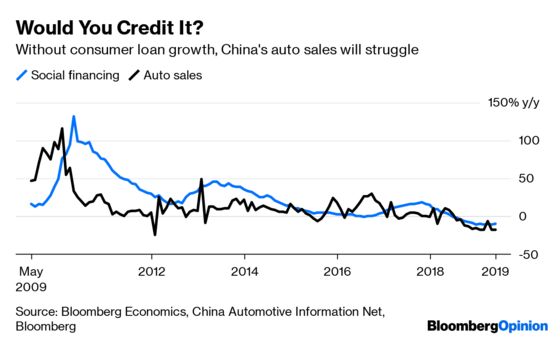

Automotive loans, a traditional tool for propping up the market, aren’t likely to help much. For one thing, the number of cars bought with such financing is still relatively small, amounting to only about a third to 40% of the market. The general weakness in Chinese credit conditions hasn't helped availability either, as my colleague Anjani Trivedi wrote. Social-financing growth, which has historically tracked auto-sales growth pretty closely, remains deep in negative territory.

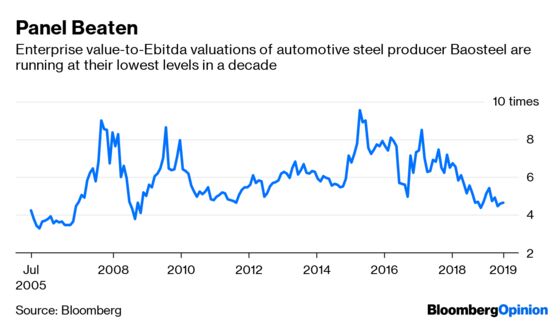

The automotive supply chain doesn’t appear to be seeing any light on the horizon. China’s steelmakers last week called on the government to restore order in the iron-ore market, a thinly veiled call for lower prices, which only goes to show how much weaker their order books are looking. Baoshan Iron & Steel Co., China’s biggest steelmaker and a major producer of the hot-rolled coil used to make automotive panels, is still trading at depressed valuations.

With the trade war deepening and signs the economy weakened in the second quarter, consumers may need some more stimulus if they’re going to emerge from this funk. The long-term picture isn’t all that hopeful: With the working-age population in decline and tough registration rules to stop urban roads from hitting gridlock, the go-go years of Chinese car-sales growth appear to be long gone. While PricewaterhouseCoopers LLP expects new car sales to be about 30% higher in 2030 compared with 2018, that’s a slower pace of growth than the 34% improvement expected for Europe.

The good news for people selling cars in China is that after 12 months, the worst may finally be in the past. The bad news is that the best may be in the past, too.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.