China Car Market Goes Bust, Boost, Boom. Repeat

Beijing’s planned stimulus policies risk prolonging the cycle of highs and lows in an industry where demand is maturing.

(Bloomberg Opinion) -- China is planning to give the world’s largest auto market a shot in the arm. Don’t be so sure it’ll work.

As the nation prepared to post its first annual decline in car sales in at least two decades, a senior official of the National Development and Reform Commission said late Tuesday the government would announce measures to encourage consumers to buy cars and other goods.

The statement finally confirmed months of speculation of imminent stimulus, sending shares of Chinese automaker stocks soaring Wednesday. China’s car market, which accounts for a third of global sales, has been heading down for six months. Passenger car sales dropped 6 percent in 2018, the China Passenger Car Association said later in the day. Retail sales of sedans, SUVs and other vehicles slumped 19 percent in December.

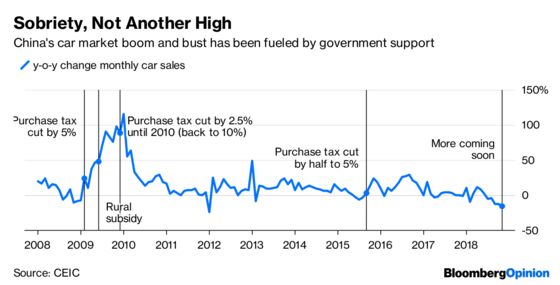

A helping hand was inevitable. After all, this has been the way for the past decade: bust, boost, boom. Repeat.

Growth is stumbling as tightening credit causes buyers, especially in the hinterland, to flinch. Consumers now play a far bigger role in the Chinese economy and cars are one of their biggest discretionary purchases, accounting for almost 6 percent of gross domestic product, a quarter of consumption value, and a fifth of industrial value added.

Stimulus will have to be targeted. Beijing has already rolled out broad income-tax cuts to lift the mood. A boost to the car market has usually come in the form of purchase tax cuts on cars with smaller engines or one-time subsidies to farmers. But Beijing already ruled out a change to the 10 percent purchase tax cut in December. Fair enough. Revenue from the levy is minuscule compared with that from corporate income and value-added taxes, so a repeat wouldn’t go far enough anyway. More will be needed.

The brand-conscious and wealthier urban buyer still wants a BMW or a Benz, but at a better price. Premium brands command the highest loyalty in China, a market that has few. Luxury buying has also been helped by widening discounts on high-end models.

The real pain is in rural areas, where consumers are far more sensitive to a weakening economy and sales have fallen off a cliff. That’s reflected in the swifter drop for SUVs beloved by buyers outside cities compared with sedans. Penetration of auto loans is slowing after rising to account for almost 40 percent of purchases. In the past five years, growth of consumer credit has increasingly become a leading indicator of passenger car sales, according to Goldman Sachs Group Inc.

With Beijing’s hands tied by fiscal pressures, sweeping policies to revive the market are hard to imagine. Channeling more credit to lower-income borrowers may create bigger problems. Subsidies running into the billions of yuan, as in 2009-2010, aren’t affordable. And tax deductions won’t move the needle enough. Helping rural buyers replace older models and perhaps even upgrade to electric vehicles may be one way. Some combination of small subsidies, tax cuts and replacement incentives could be the answer.

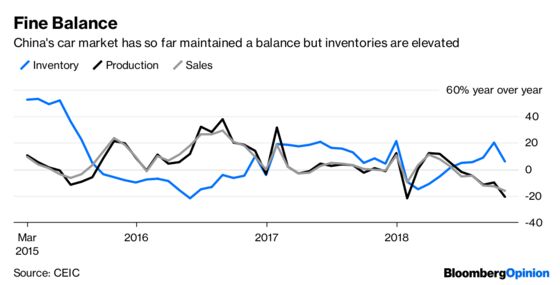

For carmakers, the rebound in valuations from rock-bottom levels is likely to prove temporary. Stimulus policies can’t mask the desperate need to reassess model ranges, production levels and inventory adjustments. At the same time, China’s electric-car policy means most car buyers and manufacturers will eventually have to switch away from internal combustion engines, radically altering the demand picture.

Ultimately, China will have to come to terms with an auto market that is maturing. Each low can’t continue to be followed by a stimulus-induced high. Beijing must push consolidation and let only the fittest survive; those companies will then have to learn to live with more moderate rates of growth. The process will be painful. It’s also necessary.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2019 Bloomberg L.P.