(Bloomberg Opinion) -- Chinese regulators have stepped back from imposing hard-and-fast rules on how much banks must lend to the cash-starved private sector. Their exhortation isn’t going away, though, and that means investors in shares of lenders should prepare for more pain.

Authorities will refrain from imposing specific targets for each bank and are urging firms to conduct appropriate due diligence, according to front-page stories carried in four of the nation’s state-run financial newspapers on Monday. That’s a softening of the position outlined by Guo Shuqing, the chief banking regulator, which caused banking stocks to plunge on Friday.

The so-called one-two-five rules mandated that at least one-third of corporate loans extended by large banks should go to private enterprises, rising to two-thirds for those from small and medium-size lenders. In three years, at least 50 percent of all new corporate advances should be directed to non-state borrowers.

That may not seem such a jump, considering about 40 percent of new credit went to the private sector between 2016 and the third quarter or this year, according to calculations by Citigroup Inc.

Make no mistake. though: It will hurt.

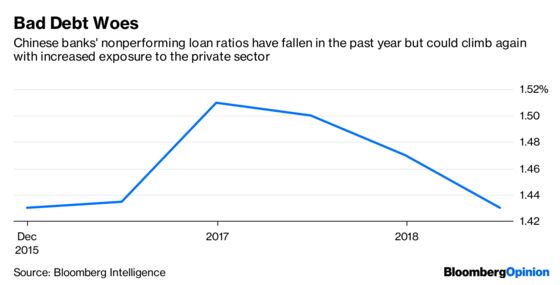

China’s private sector may account for 50 percent of tax revenue and 80 percent of jobs nationwide, but it’s in dire need of funds after bearing the brunt of Beijing’s deleveraging campaign since last year. Such state-directed lending opens banks to the renewed prospect of nonperforming loans while they are still digesting the last round of soured credit.

Lending to private firms is riskier. For one thing, they don’t have the backstop of a likely government bailout when things go wrong. Meanwhile, the absence of an in-depth and comprehensive credit-scoring system makes it difficult to assess the relative strengths of prospective borrowers. Moreover, the edict to support private companies falls disproportionately on banks less able to shoulder it: smaller lenders that typically have weaker capital buffers than state-run giants such as China Construction Bank Corp.

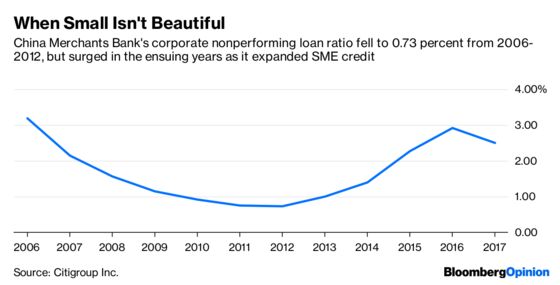

China Merchants Bank Co., the country’s eighth largest, saw its NPL ratio triple between 2013 and 2017 after aggressively expanding loans to small and medium-size enterprises, according to Citigroup.

So expect banks to work around even these weakened guidelines. Some will increase loans to individuals, allocating less to companies as a whole. Others may seek to reclassify some firms previously considered state-owned as private — a defensible maneuver in a country where ownership ties are often murky.

Real-estate developers will be a beneficiary. Unlike export manufacturers caught up in the U.S.-China trade war, they have hard assets to back borrowings. But the overall effect is likely to be negative.

Banks generally are better judges of who makes a good credit risk than government bureaucrats, as China’s bad-loan blowouts of previous decades illustrate. That was the rationale for turning the country’s lenders into profit-maximizing listed companies in the first place. It’s a lesson China’s state planners still have to learn.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2018 Bloomberg L.P.