China Risks Overplaying Its Hand on Trade

(Bloomberg Opinion) -- The U.S.-China trade war has been driven by successive rounds of misunderstanding and overconfidence.

Until the collapse of an initial hoped-for agreement in May, the Pollyannas were mainly in Washington. U.S. Trade Representative Robert Lighthizer and his allies in the Trump administration were gunning for a wholesale remaking of the Chinese state’s relationship with the economy which was never likely to happen. Now it’s Beijing’s turn to come to the table with unrealistic expectations.

Any agreement will have to be accompanied by an elimination of the latest round of tariffs imposed by Washington and a possible lowering of duty rates on previous tranches, people familiar with the deliberations told Jenny Leonard of Bloomberg News on Tuesday. In China’s eyes, that would be a reasonable recompense for buying more U.S. farm goods and cracking down on intellectual property theft, she wrote.

Rolling back tariffs has to be part of an interim agreement, according to Li Yong, deputy chair of the expert committee of the China Association of International Trade. The ultimate goal should be for them to be removed altogether, he told the Global Times, a Chinese state-owned tabloid.

China risks overplaying its hand. One only needs to look at the way global trade volumes are slumping to see that removal of tariffs should be the ultimate objective of the talks, but it’s not possible to simply unscramble this egg and go back to where we were in 2016.

Washington was far more aggressive than Beijing in ramping up tariffs in the initial phase of the trade war — driven no doubt by the fact that its imports from China are so much larger than its exports in the other direction, giving the U.S. greater scope for punitive action.

That puts both sides in a difficult position. It’s hard to see how Washington giving up levies on $360 billion of trade in return for minor concessions by Beijing could be painted as anything other than a humiliation for President Donald Trump. As a result, China must either make much larger changes than it’s been prepared to countenance so far, or wait for a shift in the political winds that forces the U.S. back to the negotiating table.

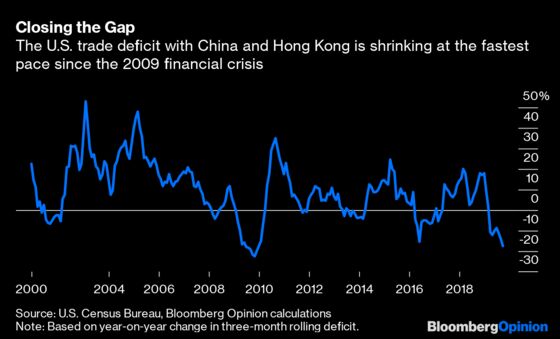

There’s little sign that Trump is feeling any pressure of that sort at the moment. America’s trade deficit with China, which appears to be his key metric for whether the fight is going well or not, is shrinking at a precipitous rate. The rolling three-month deficit in September was almost 18% smaller than a year earlier, the biggest decline since the 2009 financial crisis.

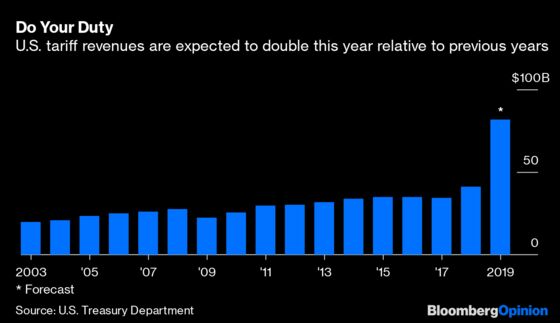

Crucially, unlike the 2009 episode, the shrinking deficit isn’t being driven by a collapse in domestic demand, either. The U.S. unemployment rate is running at its lowest levels since the 1960s. The Dow Jones Industrial Average hit another record high Tuesday, and the S&P 500 peaked the day before. Meanwhile, all that tariff money is likely to bring an extra $40 billion of duties to the Treasury this year — small potatoes in the context of a $1 trillion budget deficit, but a sizable sum in its own right.

It would be a mistake to interpret all the febrile talk about firming up venues for signing a phase-one trade deal as evidence that an agreement is around the corner. Indeed, that close-to-the-finish-line sense is often a clue that trade talks are on the verge of breaking down, just as gloom and despondency can sometimes precede a breakthrough. In their enthusiasm to press home a moment of advantage, China’s negotiators shouldn’t make the mistake of thinking they have the U.S. on the mat.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.