(Bloomberg Opinion) -- An interstellar spectacular is currently keeping China's moviegoers entertained. Behind the scenes, the film also has a minor role in the stock market's next disaster epic.

“The Wandering Earth,” a science-fiction feature released ahead of the Lunar New Year on Feb. 5, has become the second-highest grossing film in Chinese history in just two weeks. Beijing Jingxi Culture & Tourism Co., which made the movie, has said it expects to earn 73 million yuan to 83 million yuan ($10.9 million to $12.3 million) from the first six days of showings alone. That’s equal to more than 5 percent of its total 2018 revenue.

Yet Beijing Culture’s shares got only a one-day pop when markets opened after the holiday, and have since failed to share in the Shenzhen stock exchange’s post-new year rally.

The lukewarm response stands in sharp contrast to Beijing Culture’s previous hits. Its 2017 release “Wolf Warrior 2,” the second episode in a Rambo-like franchise, topped the box office with 5.7 billion yuan in gross sales. The film accounted for more than 20 percent of the company’s revenue that year. Last year, medical drama “Dying to Survive” captured the hearts (and wallets) of the middle class. Both times, Beijing Culture’s shares got a more sustained lift.

While investors may be giving the stock the cold shoulder partly because of a history of unseemly selling by insiders, what they fear most is potential writedowns. About a quarter of Beijing Culture’s total assets are goodwill, which represents the amount paid in excess of a target’s book value in acquisitions.

Goodwill is a ticking time bomb for Chinese companies. In mid-November, ahead of the 2018 full-year earnings season, the China Securities Regulatory Commission warned that all firms must re-evaluate their goodwill at least once a year, as part of an effort to crack down on inflated values.

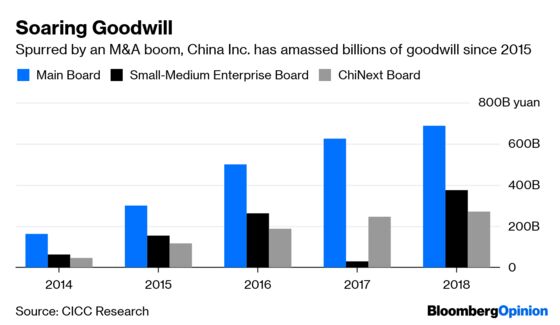

Mainland-listed companies held 1.3 trillion yuan of goodwill on their balance sheets as of the third quarter of 2018. Roughly half is on the books of smaller private enterprises, which last year set off one of the world’s worst stock market routs after pledged-share loans triggered margin calls. Goodwill averages 21 percent of net assets for companies on the ChiNext Index, versus only 4.4 percent for Shanghai’s main board.

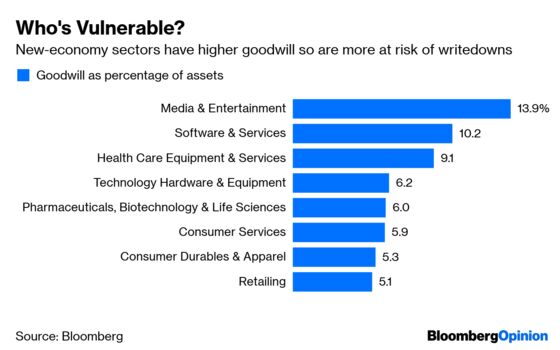

Already, 58 firms have issued profit warnings involving goodwill impairments, only one month into the full-year earnings season for A shares, according to CICC Research. New economy sectors such as media, software, and health care have the highest goodwill-to-asset ratios, data compiled by Bloomberg show. This fact alone will cap how much of a rebound we can expect from the technology-heavy Shenzhen exchange this year.

A-share companies started to accumulate goodwill assets in 2015, as looser monetary conditions made it easy for China Inc. to finance acquisitions with debt. Between 2015 and 2016, domestic credit grew by more than 20 percent.

The takeover spree picked up after China’s securities regulator shut the IPO window again in 2016. If an entrepreneur wants equity financing and can’t list, an obvious way is to sell the company to a peer that already has a ticker on the Shanghai or Shenzhen exchange.

The government knows that firms with too many intangible assets often spell trouble.

Wintime Energy Co. is a good example. One of China’s largest defaulters last year, the coal miner again rattled bond investors when it missed payments earlier this month. Over the years, Wintime has amassed 60 billion yuan of net debt, backed by 100 billion worth of long-term assets, over half of which is in the form of intangibles such as goodwill and coal-mining rights. With solar panel makers perceived as national champions and the cost premium for new projects over coal withering, how much are Wintime’s assets really worth? Had the company been forced to write down assets earlier, it might not have been able to raise so much debt.

Earnings season will go into full swing next month. Impairments and profit warnings won’t make for pleasant viewing. But it’s a show that Beijing is willing to sit through.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.