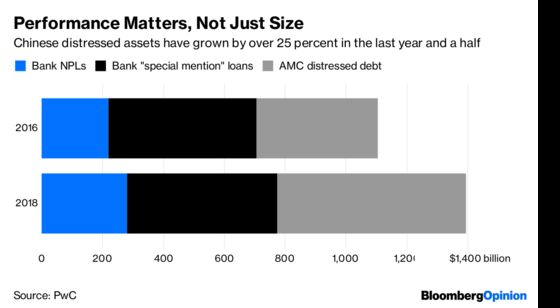

Chasing This $1.4 Trillion Prize May Cause Distress

(Bloomberg Opinion) -- As compelling as the $1.4 trillion pile of distressed assets in China looks, there are few reasons to think foreign investors will walk away with substantial winnings.

Prices are falling again after a blockbuster 2017, when a wave of domestic institutional money pushed distressed debt values to almost 80 cents on the dollar from 30. This partly reflects new supply and partly a crackdown on the shadow-banking system that previously allowed investors to finance purchases of nonperforming loans, according to Dinny McMahon of Macro Polo, an in-house think tank of the Paulson Institute.

About 3,000 local investment funds, well versed in the ground rules of Chinese nonperforming assets, have backed off for now. Returns on distressed assets have fallen as their quality deteriorates. Low-hanging fruit like real-estate debt, which is easily recoverable, is either too expensive or in cities where the property market has started to cave. More bad loans are expected to come to market as China attempts to clean house and cut off overburdened borrowers.

Having been crowded out thus far, foreign investors are being invited in with open arms. Earlier this year, the State Administration of Foreign Exchange further loosened requirements for a one-year old pilot program that helps cross-border transfers of Chinese NPLs to foreign investors via an exchange. Over the past year, around 12 portfolios (comprising three or more loans) have been sold to the likes of Oaktree Capital Group LLC, Lone Star Funds and Goldman Sachs Group Inc., McMahon notes, citing PricewaterhouseCoopers.

They shouldn’t get too excited. It’s likely to be slim pickings this time, compared with the heyday of the late 1990s bank cleanup, when China set up four asset management companies to deal with bad loans stemming from the Asian financial crisis.

In theory, the entry of foreign institutional capital should be positive, contributing to the cleanup of China’s bad-debt overhang while offering opportunities for distressed-debt specialists to profit from their expertise. Yet finding good portfolios with high recovery rates is increasingly difficult, even as the increase in supply and weakening of demand cause prices to soften. While underwriting loans in China isn’t rocket science, it does take deep understanding of the market in terms of valuations, recovery and risk, PwC noted in a report on Chinese NPLs.

Recovery and bad loan resolution is usually the job of debt servicers, whose limited presence is an obstacle to realizing returns. If investors aren’t able to enforce collection through servicers, the only route is the court system. The harder the process, the more expensive it gets.

Investors in Chinese distressed debt still expect internal rates of return of close to 15 percent, a lofty target. To put that in perspective, consider how well the local experts are doing: China Cinda Asset Management Co. posted an annualized monthly average return of 8.1 percent on some of its distressed debt assets in June this year.

Those returns don't look compelling, given the costs and risks. Bad assets aren’t good business in China yet.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2018 Bloomberg L.P.