(Bloomberg Opinion) -- Looks like deposed car executive Carlos Ghosn was right after all: Nissan doesn’t care about shareholder value.

Nissan Motor Co. on Tuesday reported dismal earnings and gave an even grimmer outlook. Still worse: The company said it would slash its dividend by 30%. Chief Executive Officer Hiroto Saikawa then proceeded to talk about fanciful ideas of improving governance and the company’s transformation and recovery.

No wonder the stock slumped as much as 8% Wednesday, and is on track for its biggest daily drop in almost three years. That’s after underperforming the Nikkei 225 since 2016. In his video message last month, Ghosn harped on Nissan’s “value destruction.” It’s hard to dispute him: Returns on equity have dropped to just about 6% from their peak of 16% two years ago. How can shareholders maintain any trust in management?

Saikawa and the rest of the board have a history of keeping shareholders, especially minority ones, at arm’s length. Blinded by the prospects of a full merger with Renault SA, its corporate alliance and palace intrigue, the company’s leadership has consistently ignored investors’ changing sentiment. In 2017, an increasing number didn't want Ghosn or Saikawa running the company; and from 2015 to 2017, support for both deteriorated far more than for any other board directors.

The blame for bad business practices and serious governance lapses lies as much on Saikawa as it does on Ghosn. But if the company’s reins stay in Saikawa’s hands, the damage could deepen.

Consider Nissan’s latest outlook. Net income for its fiscal year 2019 is expected to fall 47%, but capital expenditure as a percentage of net revenue is expected to rise 12%, as is the portion spent on research and development. How can the company be talking about spending as the bleeding continues?

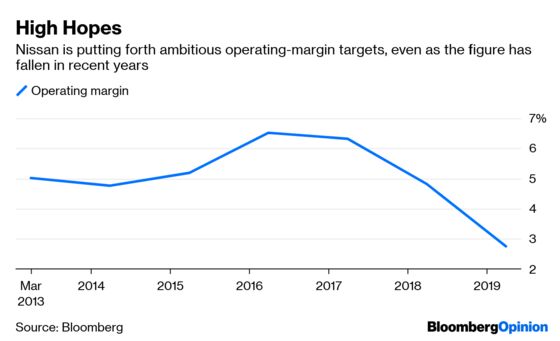

Next, its operating-profit outlook points out that much of the deterioration will come from spending on compliance and improving its products, as sales of its baseline cars continue to slide. Meanwhile, Nissan is now targeting 6% operating margins – more than double its latest 2.8% figure, and close to levels from three years ago. A lot has changed since then, at the company and in the global auto market. If anything, that outlook is misleading.

Of course, slashing the dividend also makes Nissan less valuable for its single largest shareholder, Renault. On Wednesday, the French company said Nissan's results would hit first quarter net income by an estimated 56 million euros ($62.8 million). But the Renault’s insistence on merging is more a political maneuver than a solution to Nissan’s problems.

If Nissan wants to regain shareholders’ trust, it might be time to push for an overhaul at the top.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2019 Bloomberg L.P.