(Bloomberg Opinion) -- Britain's malls are some of the least desirable shopping destinations for international investors. But even this supremely unloved part of the London stock market has a price.

Property mogul John Whittaker has teamed up with Brookfield Property Group and Saudi investment fund Olayan Group to explore a potential buyout of U.K. mall operator Intu Properties Plc.

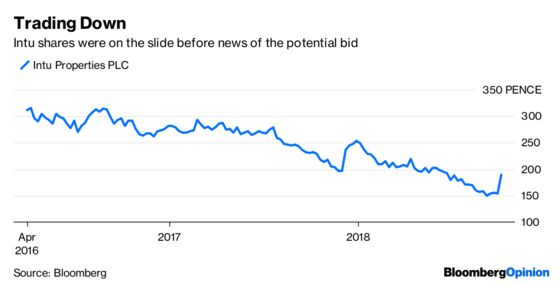

Whittaker’s Peel Group already has a 27 percent stake in Intu, while Olayan owns about 3 percent. Before their putative bid emerged late on Thursday, the value of those holdings had fallen 60 percent since early 2015. No wonder they were fed up. As for Brookfield, it has a reputation for investing against the grain. Intu's valuation is superficially enticing: even after a jump on Friday, the shares trade at a 39 percent discount to book value.

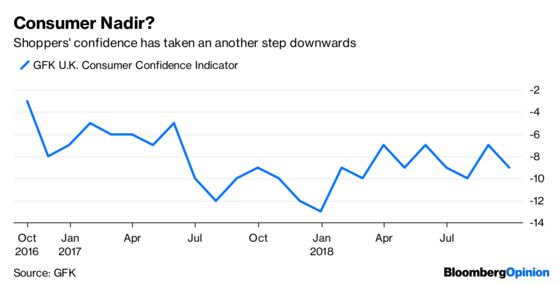

It is dangerous to call the bottom for the U.K. consumer given the number of high-profile retail failures this year. Then there are chains such as Mothercare Plc and Carpetright Plc which have pursued controversial restructurings that have cost their landlords. Hopes of a revival in spending have been dashed by a continuing squeeze on Britons' disposable incomes.

The flip-side is a large amount of store capacity has left the market, benefiting the retailers still standing. Wages are increasing, while fixed-rate mortgages will insulate many consumers from the expected increases in interest rates. A better-than-expected Brexit deal could release demand. And physical stores will still have a place in the online retailing world for returns and those click-and-collect bargains.

Clearly, industry insiders reckon Intu is a good way to wager on a recovery in U.K. retail. Without a firm proposal made, the stock jumped as much as 37 percent on Friday to 204 pence, valuing the company at 2.8 billion pounds ($3.2 billion). Even with the real risk that a binding offer fails to materialize, money managers suddenly see value here.

An approach, if one does happen, would be tricky for the Intu board to handle. Directors recommended a 254 pence-a-share offer from Hammerson Plc in December. That was pitched at 28 percent premium to the prevailing share price and a 27 percent discount to the then net asset value. But Hammerson shareholders balked at consummating the deal and expanding their exposure to the sickly retail industry.

To recommend a considerably lower offer today, and one coming from Intu's dominant shareholder, would require some explaining to everyone else. Any bid would be in cash, forcing many investors to crystalize a loss at a terrible point in the cycle. The view of South Africa's Coronation Fund Managers, which owns 21 percent of the company, will be critical. If Brookfield wants full control, rather than just a majority stake, it will need Coronation's support.

A loss of stock market confidence means it will be hard for Intu to make the case for a standalone future. Pulling in a rival bid from Hammerson looks like wishful thinking – its shareholders are still almost certainly against a deal. But if Intu could persuade Coronation to hold out, it would gain some leverage to play hardball.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2018 Bloomberg L.P.