Celgene Is the Remedy for Bristol-Myers's Cancer Setback

(Bloomberg Opinion) -- Bristol-Myers Squibb & Co. investors seem confused.

The company’s immune-boosting cancer medicine Opdivo has been battling Merck & Co.’s Keytruda for market share in the lucrative lung-cancer market, and mostly losing. That streak continued Wednesday night as Bristol-Myers reported mixed results from a key drug trial, prompting a more than 4% drop in the company’s shares after the bell. The drugmaker managed to counter that Thursday morning with second-quarter results that topped Wall Street estimates; this news caused investors to pile back in, erasing the stock’s losses and fueling a gain of more than 5% in early trading.

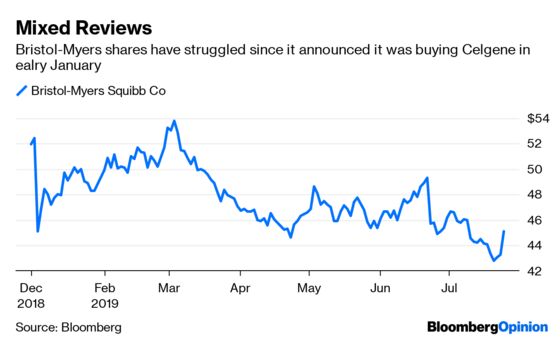

To clear up the confusion: it’s the long-term trajectory of Opdivo that matters – and as that clouds, it’s more important than ever for shareholders to know that Bristol-Myers is working on the next big thing. Its decision to buy biotech giant Celgene Corp. for a $74 billion was meant to be a partial solution, but the blockbuster deal has been viewed skeptically by investors since it was announced in January, weighing on the shares. The real upside from these two turbulent days may come if Opdivo’s struggles finally convince these skeptics to get on board with the deal, warts and all.

We won’t know how bad Wednesday’s results are until Bristol-Myers presents more data from its complicated trial. What is clear is that while a combination of Opdivo and another immune-focused drug Yervoy improved survival for newly treated lung cancer patients relative to chemotherapy, a combination of Opdivo and chemo failed. A chemo-Keytruda combo has been a massive success for Merck in the lucrative lung-cancer market.

The drug world will endlessly debate whether Opdivo’s poor results are due to bad luck, lousy trial design, or Keytruda’s possible superiority. That question is impossible to answer without a comparative clinical trial that no one is likely ever to run. Regardless of their source, continued setbacks mean that Opdivo could lose share in markets that it currently competes in and struggle to break into new ones. That’s grim news for a stand-alone version of Bristol-Myers Squibb.

Opdivo is expected to provide much of the company’s growth going forward, especially because profits for blood thinner Eliquis – its other big seller – are split with Pfizer. Bristol-Myers has plenty of ongoing late-stage trials, but comparatively few that don’t involve its tarnished cancer blockbuster.

Celgene, on the other hand, has five very different new medicines that are nearing the market and a wide variety of earlier-stage projects. On top of that, its marketed products will provide massive diversifying cash flow. Investors know this, but the deal has plenty of detractors. A key holder and activist noisily attempted to derail it earlier this year.

They had their reasons. Celgene’s blood cancer drug Revlimid accounts for the majority of its sales; an early generic entry could shave off billions in cash flow. More recently, the two companies also announced plans to sell off one of Celgene’s other bestsellers to appease regulators, a surprise that increases exposure to Revlimid. Its recent R&D track record has been somewhat mixed.

Those are significant risks. But the latest Opdivo setback suggests that they pale in comparison to the dangers of Bristol-Myers going it alone.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.