(Bloomberg Opinion) -- During the past 16 months, Celgene Inc. has gone from biotech darling to pariah after a series of research fumbles. On Thursday, Bristol-Myers Squibb Co. — which has had its own share-price stumbles after cancer setbacks — rode to Celgene’s rescue and possibly its own with a $74 billion dollar cash-and-stock deal.

Celgene is cheap for a reason, and this is still a gamble. But Celgene has valuable assets that may yield more under different management; Bristol-Myers, meanwhile, will vault from R&D laggard to one of the industry’s most exciting firms. Its shares declined early, perhaps reflecting investor surprise. But this deal adds major cash flow and excitement for Bristol-Myers at what may end up being a good price.

The price reflects a 54 percent premium that could jump higher, with a $9-per-share contingent value right included that’s tied to certain regulatory milestones. That’s not nothing – but it deserves some context.

A little over a year ago, Celgene was worth $114 billion. Since then, a potential blockbuster gut drug flopped a late-stage trial; a multiple sclerosis drug has faced endless delays; the firm has slashed guidance; and investors have grown concerned that the firm relies too much on blood-cancer blockbuster Revlimid, which accounts for more than 60 percent of its sales.

But Celgene’s slip below a $50 billion market cap and consistent flirtation with five-year lows was a clear sign that disappointment in management had overshadowed the firm’s actual asset quality, and a signal to potential buyers that there was a deal to be had. Bristol-Myers’s offer values Celgene’s equity at about 5 times trailing 12-month revenue. That’s about the median for large drug deals, and in line with what Shire PLC paid for Baxalta Inc.

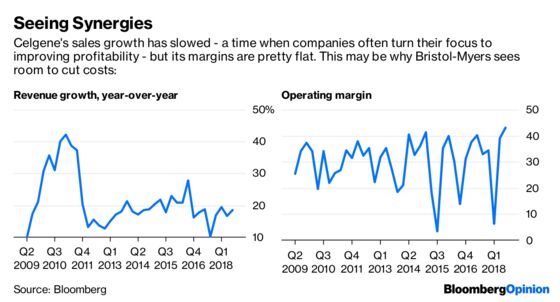

Celgene’s growth is slowing as Revlimid matures. But the medicine, likely the best-selling cancer drug in the world last year, has at least a few more years of momentum left before generic competition hits. That should be supplemented by new drugs soon. While Celgene’s pipeline isn’t the shiny jewel it was a few of years ago, the firm has multiple medicines on the cusp of being approved by the Food and Drug Administration, as well as plenty of promising early-stage investments. Blood-disease drug luspatercept could hit the market this year, to be followed by MS drug Ozanimod and advanced blood-cancer cell therapies That’s more than what most of pharma can say.

It’s certainly more than Bristol-Myers can offer on its own. The firm has an over-reliance problem of its own. Outside of blood thinner Eliquis and immune-boosting cancer blockbuster Opdivo, it has very little to excite investors. That’s a scary place to be. Eliquis has potential patent issues, and Opdivo has been getting thrashed in clinical trials and on the market by Merck & Co.’s rival drug Keytruda.

The Celgene acquisition solves that problem and more. It’s certainly a risk. If Revlimid faces competition sooner than expected and the pipeline disappoints, Bristol-Myers could be back where it started.

Bristol-Myers thinks it can realize $2.5 billion in annual synergies by 2022, and presumably that it can manage Revlimid’s decline. If Celgene’s string of awful pipeline luck moderates even slightly, this could very easily be a major pharma bargain.

--With assistance from Tara Lachapelle.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.