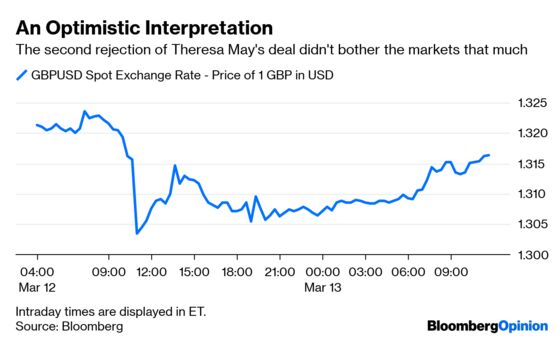

(Bloomberg Opinion) -- U.K. Prime Minister Theresa May has repeatedly promoted her Brexit deal as the best alternative to either crashing out of the EU without an agreement or shelving the whole sorry adventure and staying in. Yet the market reaction to her second failure to win Parliament’s support for her plan tells you that investors think the threat of a no-deal departure is now off the table, and that something positive will emerge from this mess.

The pound climbed higher despite the evidence that May’s government and the House of Commons are entirely dysfunctional. Traders think (no doubt correctly) that British lawmakers will on Wednesday evening reject the idea of a no-deal Brexit. Their hope is that the subsequent vote on Thursday to delay the March 29 deadline will provide a new base from which to build a more economically benign departure from the EU.

If Britain ends up holding a general election or a second referendum, so be it, the thinking goes. The post-May era can begin and a softer Brexit or no departure at all will be the happy outcome. This is the basic rationale for the pound trading at close to $1.32, not far off its recent highs.

There’s some dangerous optimism at work here. The first flaw is to assume that a no-deal Brexit can be killed unilaterally by Westminster. The only way of avoiding the automatic March 29 Brexit deadline is through the support of the 27 other EU member states, and it’s not clear for how long and under what conditions a delay would be granted.

A short extension of a few months certainly looks doable, even if it just brings both sides to another cliff-edge in May or June. More time to prepare for a no-deal Brexit can only be a good thing. A long extension of one to two years, as I’ve written, would be damaging for the EU’s own integrity as it elects a new parliament in May and appoints a new European Commission in the fall. A long delay is also unpopular with the British public, polls say.

Securing a short extension would help the British economy dodge a catastrophe, even though Brexit has already done plenty of damage. It certainly won’t help bridge some intractable divides within Westminster. The idea that a few months is all Britain needs to secure a cross-party consensus for an alternative Brexit arrangement looks like wishful thinking.

We already know there’s no majority for the plan from Jeremy Corbyn, leader of the opposition Labour Party, which includes a permanent customs union with the EU, nor is there support for Norway-style access to the EU’s single market from the major parties. The idea that Parliament is now “in control” is appealing to some investors, but it’s a fiction. May is still there, as are her ministers and an increasingly factional bunch of lawmakers. For Brussels, this isn’t suddenly a viable negotiating partner.

Expectations that a general election or referendum will break the impasse are also viewed cheerfully by traders. But can the British public and its politicians choose pragmatism over populism? The latest Kantar poll on voting intentions in a second referendum shows 29 percent don’t know, 32 percent would leave and 40 percent would remain. There’s still plenty of doubt.

An election would boot out Theresa May but might leave the country with a choice between Corbyn and Boris Johnson (the bookies’ favorites) for prime minister. Labour has struggled in the polls because of its failure to keep remain voters on board and its half-hearted attempts to deal with anti-semitism within the party. But if it’s a choice between Corbyn and an avowed hard Brexiter, all bets are off. Short-seller Steve Eisman has made bearish U.K. trades, not least because of the Corbyn threat. Johnson, meanwhile, openly embraces no-deal Brexit and has been foul-mouthed in dismissing the worries of business. Political extremes haven’t gone away.

Indeed, even if the dreams of the “People’s Vote” supporters come true and the country ends up remaining, this wouldn’t be the end. Revoking Article 50, the mechanism by which Britain leaves, would unleash its own populist demons and entrench the societal schism laid bare by the first referendum. The ultimate choice seems to me to be no deal, or no Brexit. But investors should be weighing up the cost of that second eventuality too.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering Brussels. He previously worked at Reuters and Forbes.

©2019 Bloomberg L.P.