(Bloomberg Opinion) -- In some theologies, purgatory is where the souls of the dead undergo purification of their sins before rising to heaven or descending into hell. As the deadline for Britain’s exit from the European Union approaches, U.K. assets face a similarly binary outcome — making investors justifiably unwilling to take big bets on the endgame.

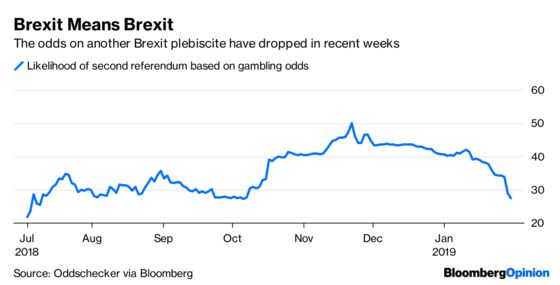

As things stand, it remains a coin-toss whether the nation crashes out with no deal, or whether the latest political gymnastics will produce an accord palatable to both sides. What seems unlikely is a second referendum that could — maybe — see the U.K. stay in the bloc.

UBS is warning investors to steer clear of making Brexit-related bets. “We remain wary of taking directional views on sterling and U.K. assets,” the bank’s economists said in report published Wednesday. “Although much seems like it has changed, the reality is that very little has.” The Swiss firm this week cut its U.K. growth forecast for this year to 1.5 percent, down from 1.8 percent previously.

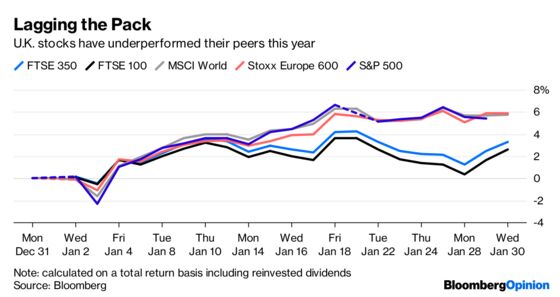

It’s little wonder that British stocks have underperformed their peers elsewhere.

Other benchmark equity indexes have rallied by about twice as much as those in the U.K. this year as domestic investors have shunned the British market. There, individual investors pulled 2.1 billion pounds ($2.7 billion) out of their funds in November, the biggest outflow since the Brexit referendum, according to figures released earlier this month by the Investment Association. Shares of Hargreaves Lansdown Plc, the U.K.’s dominant fund platform, have fallen almost 10 percent this week, with most of the decline coming Tuesday after the company blamed Brexit for most of the 6 percent drop in assets under administration it experienced in the final six months of last year.

Investors are right to be wary of sterling-denominated assets. Almost every path in the decision tree that leads to a deal has potentially insurmountable roadblocks. There’s the infighting in both the Conservative and Labour parties. There’s the very vocal reluctance of the EU to reopen the so-called Withdrawal Agreement. And the issue of the Irish border — barely mentioned by either side in the run-up to the referendum — remains the biggest current obstacle in the talks.

Because none of the potential outcomes of the debate has a probability of more than 50 percent “any Brexit bet is more likely to be wrong than correct,” according to Bloomberg Intelligence economist Dan Hanson. He’s absolutely correct.

A stay of execution may be possible, but what exactly delaying the end-date would achieve hasn’t been made clear even by its most fervent supporters. The bloc is understandably unwilling to give the U.K yet more time to tie itself into more knots.

Policymakers at the Bank of England, meantime, have been unusually reticent in commenting on the chaos. As my colleagues David Goodman and Jill Ward at Bloomberg News note, there’s only been one significant policy speech since the publication of the central bank’s economic forecasts in November — on “Some Effects of Demographic Change on the U.K. Economy” by Michael Saunders.

Given the storm of criticism that greets any Brexit-related warnings from the BOE, a self-imposed purdah is probably a sensible strategy. But it’s hardly reassuring for investors that the impartial, independent grown-ups in the room feel compelled to stay silent during such a crucial juncture in history.

And the evidence of harm to the U.K. economy is mounting. Figures this week showed consumer confidence sank to its lowest level since May 2013 this month, while lenders approved the fewest home loans in eight months in December.

To be sure, the global economic backdrop is also deteriorating generally. The German government just cut its growth forecast for 2019 to 1 percent from 1.8 percent previously, which would mark the slowest expansion since 2013. In a speech on Wednesday, Economy Minister Peter Altmaier cited “great concern in industry that an unregulated Brexit, a hard Brexit, at the end of March could lead to significant economic upheaval between the U.K. and the rest of Europe.”

For Brexiteers, the economic damage that a no-deal exit would inflict on Britain’s neighbors remains a key bargaining tool. But I’m reminded of the scene in the 1974 Mel Brooks film “Blazing Saddles” where the sheriff threatens to shoot himself if the vigilantes threatening to kill him don’t back away. His bluff worked; I don’t think chief EU negotiator Michel Barnier is as gullible as the townsfolk in the movie.

Quitting without a deal remains the default option, and therefore is in many ways the easiest to envisage, even if it’s the most economically painful outcome for everyone concerned. Investors are right to stay on the sidelines as far as U.K. assets are concerned; March 29 will arrive soon enough, and probably faster than a resolution to the crisis Britain has created for itself.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.