Botox Maker's Changes Need to Be More Than Cosmetic

(Bloomberg Opinion) -- Allergan PLC finally responded to months of investor agitation about its under-performance by announcing some tweaks to its management structure and governance. It’s not enough, and investors know it.

The Botox maker late Friday said it plans to split the CEO and chairman roles – a goal of hedge-fund holder Appaloosa Management – but only after an unspecified future “leadership transition.” It seems that current CEO and Chairman Brent Saunders likes being his own boss. It also announced some other governance moves, including strengthening the role of its lead director, all of which amount to only minor changes.

There may have been a strategic element to the timing of its announcement, but it didn’t escape investors’ notice: Allergan shares slipped 1.6 percent Monday and Appaloosa blasted the news. The changes aren’t nearly enough for a company that’s performing as poorly as Allergan, and continues a pattern of behavior where leadership insists on maintaining a strategic course that has served investors poorly.

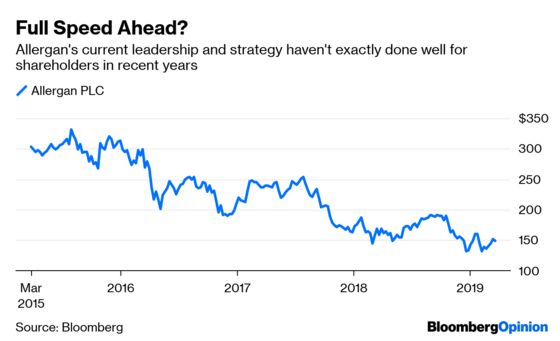

Calls for a shake-up are well-founded. Allergan’s stock has plunged 37 percent in the past two years and 56 percent from its 2015 peak. Its fundamental strategy and makeup look increasingly dicey, with generic competition eroding sales of older medicines even as the company has failed to produce new and growing products at a sufficient rate.

Its “open-science” model – one that favors sourcing drugs externally over developing them itself – is supposed to be a strategic differentiator, but has so far been a disappointment. The experiment was richly funded by the $39.5 billion sale of its generics business to Teva Pharmaceutical Industries Ltd. but has failed to deliver value. A number of Allergan’s drug deals have flopped commercially or in trials, an Appaloosa analysis found some $13.4 billion in M&A-related impairments since 2015.

The latest failure came earlier in March from a late-stage trial of a depression drug acquired via the $560 million acquisition of Naurex in 2015. That medicine has been touted by management as one of the firm’s “star six” late-stage drugs. Now that particular star has winked out, and the data and sales outlook for several others is B-list at best. “Open science” might be a fine strategy, but Allergan isn’t good at executing it.

Allergan nodded at these mishaps Friday by also announcing the creation of a dedicated board committee focused on M&A. It’s unclear if it’ll have any real power, and is well short of an actual shift in strategy.

Investors would be unhappy with this scenario on its own, but on top of draining the firm’s resources and share price, the struggling parts of the drug unit are dragging down the firm’s more successful Botox and aesthetics businesses. Those divisions have a very different risk and growth profile, which is largely a function of the fact that the Allergan of today was assembled via a number of large deals in a relatively short period of time. That’s created a sometimes ill-fitting collection of assets, and it’s fueled loud calls for a breakup.

Instead of acknowledging these issues, Allergan has been something of a hoarder. The company conducted a strategic review last year under pressure from investors. The result? The planned sale of one small business, its anti-infectives division. The unit could fetch around $2 billion at most, Bloomberg Intelligence has estimated; the firm's most recent annual filing pegs its fair value at $885 million. It’s hard to be confident that Allergan will use that money well, and in any event, the sale does little to narrow the company’s focus.

The decision to add only mild additional management oversight effectively doubles down on Allergan’s current approach. Saunders has defended the company’s unwillingness to make major changes, saying that big moves would disrupt the firm’s strategy and turnaround effort. I don’t think investors see the prospect of disruption – either of management or the company as a whole – as such a bad thing. And they’re right.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.