Bond Market Sell-Off Lacks Key Ingredient

Quiescent inflation, questionable stock valuations, a currency clash and more lead market commentary.

(Bloomberg Opinion) -- The U.S. Treasury market experienced a rare event on Tuesday, which is to say prices rose and yields fell. To put the action in context, consider that since the recent intraday low of 2.81 percent on Aug. 23, benchmark 10-year note yields have risen on 22 trading days on their march to 3.26 percent. In other words, yields rose 73 percent of the time amid the sell-off, the highest such percentage since May 1984, according to the interest-rate strategists at BMO Capital Markets.

There was no specific catalyst for Tuesday's rally in bonds other than perhaps the International Monetary Fund trimming its 2018 global economic growth forecast to a still healthy 3.7 percent from the 3.9 percent it had forecast in July. Maybe a better explanation might be that the almost seven-week-long slump hasn't been accompanied by a surge in inflation expectations. So while 10-year yields are the highest since 2011, breakeven rates on Treasuries — a measure of what traders expect the rate of inflation to be over the life of the securities — are only back to where they were just a few months ago. As long-time traders know, it's hard to have a lasting bear market in bonds without a big acceleration in both realized inflation and inflation expectations. Regarding the former, the three-month annualized rate for the core personal consumption expenditure index, which excludes food and energy, dropped from a recent peak of 2.2 percent to 1.8 percent in August. That’s important because the Federal Reserve targets a 2 percent inflation rate, and if the core PCE rate falls further below 2 percent it may eliminate a big reason policy makers have to keep raising interest rates.

Of course, markets never go up or down in a straight line and the rise in bond yields could resume, especially if traders become more concerned about all the supply of debt that the U.S. government is dumping on them to finance a soon-to-be $1 trillion budget deficit. But there are a couple of metrics suggesting that perhaps bonds are a relative bargain. First, 10-year notes yield about 1 percent after inflation, which is toward the high end of the range since 2011. Second, more than 50 economists and strategist surveyed last month by Bloomberg didn't expect yields to get this high until mid-2019, indicating that the rise went too far, too fast.

THE CRUEL MATH OF STOCKS

Stock investors are clearly concerned that bond yields have permanently entered a new, higher trading range. This is important because low bond yields have been a primary reason that investors have been willing to accept relatively high price-to-earnings multiples in recent years. That dynamic makes this earnings season all the more critical. Although the consensus is that companies will report third-quarter earnings that are 19.2 percent higher than a year ago, investors will be looking for evidence that revenue growth is strong as well and that companies are confident that they can continue to expand the top line, according to DataTrek Research co-founder Nicholas Colas. "If interest rates are in fact permanently higher, then organic earnings growth — driven by revenues — must rise or valuations will fall," Coals wrote in a research note. "That’s the cruel simplicity of equity valuation math." After increasing 9 percent in the second quarter from a year earlier, revenue growth is seen slowing to 7.3 percent in the third quarter and 6.3 percent in the fourth quarter.

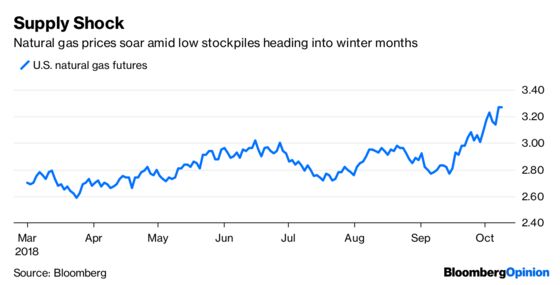

ENERGY BILLS WILL RISE

The market for natural gas — a key source of energy — is starting to stir. Prices have risen to the highest in 10 months amid the lowest stockpiles in 15 years and looming cold weather in the U.S. Midwest. Along with higher oil and gasoline prices, the question for markets is whether rising energy prices bolster inflation or act as a drag on consumer spending. Record gas exports have limited the amount added to underground storage, leaving stockpiles at the lowest since 2003 for this time of year and spurring concern that prices will spike during the winter, when demand peaks, according to Bloomberg News's Rachel Adams-Heard. Futures are trading around $3.267 per million British thermal units, and nine of 10 traders and analysts surveyed by Bloomberg News last week said they were bullish on natural gas heading into the winter. While most expect gas to trade near $4 per million BTUs, three predict futures could jump to $6 or higher — a level not seen since arctic cold blanketed the eastern U.S. during the “polar vortex” of early 2014.

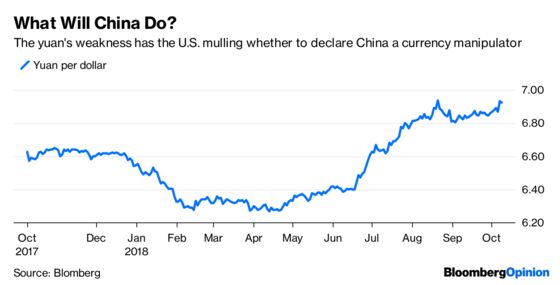

FROM TRADE WAR TO CURRENCY WAR

The trade war between the U.S. and China looks like it might be rapidly developing into a currency war. The tightly controlled yuan has depreciated about 9.5 percent since mid-April and the U.S. Treasury Department is weighing whether to name China a currency manipulator in a report due out next week, a senior Treasury official said Monday. To be sure, declaring China a manipulator wouldn’t trigger any sanctions or other U.S. penalties. Still, it likely would escalate trade tensions, potentially upsetting markets and paving the way for other actions down the road. Bets are mounting that China’s currency will slide to a level not seen since the global financial crisis, as the government tries to shield the economy from a trade war. The notional value of new options betting the yuan will weaken past the psychological milestone of 7 per dollar is at the highest since depreciation pressure really began to pick up in June, according to Bloomberg News's Tian Chen. Last week saw more wagers added than in mid-August, when the currency hit a 19-month low and authorities used verbal warnings and stronger fixings to deter speculators.

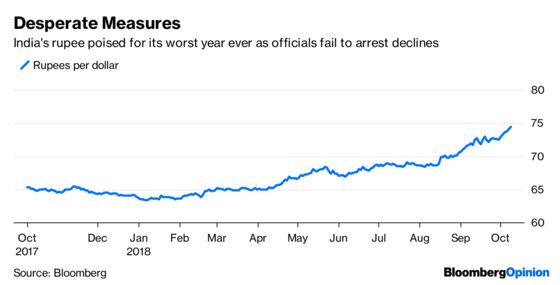

INDIA MULLS URGENT MEASURES

Officials in India, whose efforts at stemming a plunge in the rupee, are starting to look desperate. Prime Minister Narendra Modi’s government is considering tapping Indians living overseas to lure foreign-exchange flows and prop up a sagging rupee, according to Bloomberg News's Anto Antony and Siddhartha Singh. Citing people with knowledge of the matter, they reported Tuesday that officials from the finance ministry and the central bank are discussing a plan to raise money from non-resident Indians. There's no shortage of investors closely watching India — it’s the “I” in the BRIC acronym that also includes Brazil, Russia and China — and its efforts to keep the rupee's 14 percent decline this year from turning into a full-blown currency crisis. The risk of a widening current-account deficit has left the rupee vulnerable to the rout in emerging markets amid surging oil prices, trade tensions and rising U.S. interest rates. Overseas investors have pulled a net $11 billion from Indian stocks and bonds this year.

TEA LEAVES

Investors will get a fresh round of U.S. inflation data to ponder starting Wednesday when the government releases its report on producer prices for September. That's followed on Tuesday by the consumer price report. The August Producer Price Index sparked a mini rally in bonds when it unexpectedly fell 0.1 percent, the first decline in 18 months and below estimates for a 2 percent gain. The Consumer Price Index also came in below estimates, rising 2.2 percent from a year earlier when excluding food and energy, compared with the 2.4 percent median estimate of economists surveyed by Bloomberg News. "Much of the inflation data were on the soft side in August, so the September results will show whether the profile is indeed softening in the second half of the year," Bloomberg Intelligence economists Carl Riccadonna, Yelena Shulyatyeva and Tim Mahedy wrote in a Friday report.

DON'T MISS

'Trumponomics' Takes a Heavy Toll on World: Ferdinando Giugliano

Flight to Quality Could Be a Problem for Stocks: Stephen Gandel

The Best 2018 Bond Strategy Has a Stock Problem: Brian Chappatta

New Era of Free Trade Leaves Mexico More Isolated: Daniel Moss

The End of Coal Could Be Closer Than It Looks: David Fickling

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.